In December 2024, the IMF published their latest report on the Philippines economy under the Article IV consultation process.

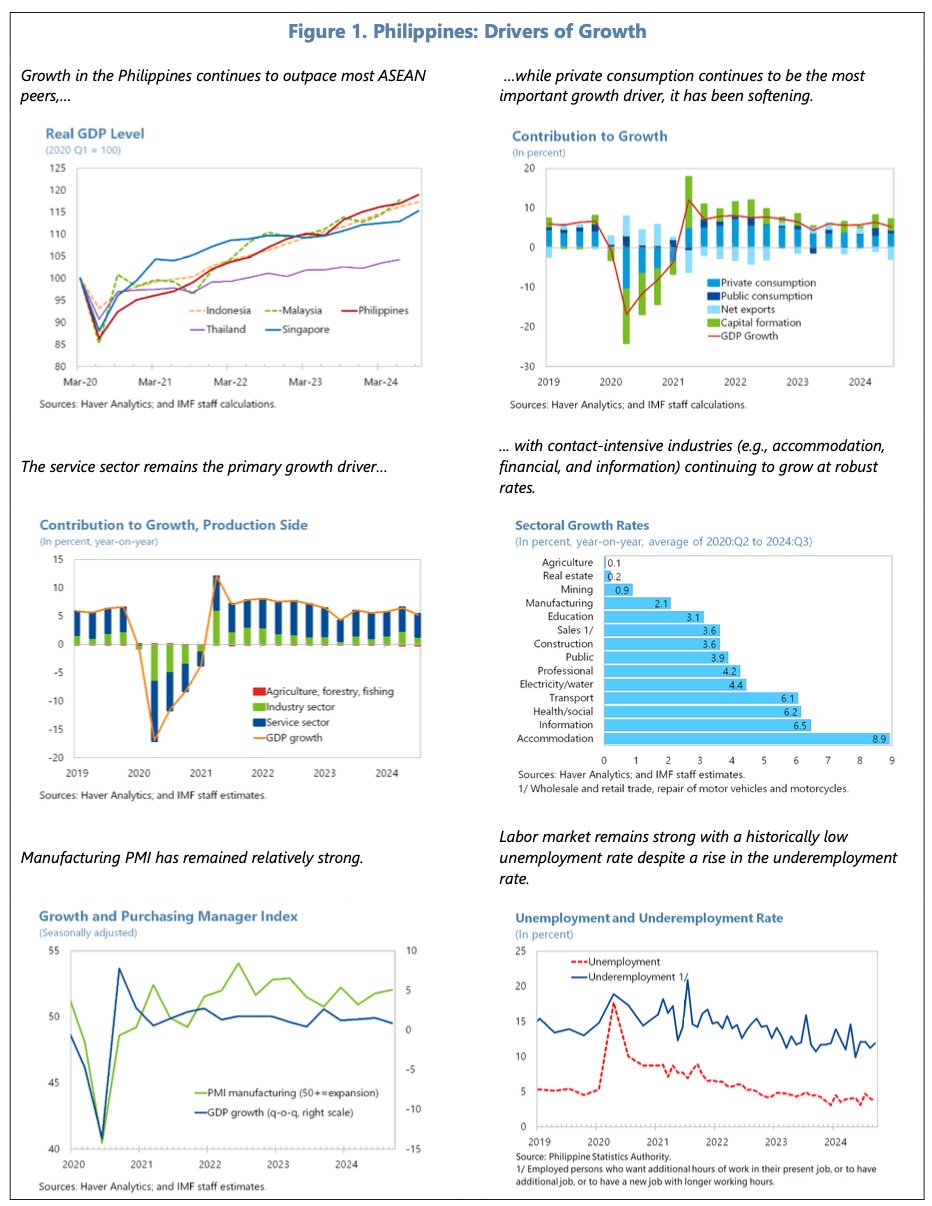

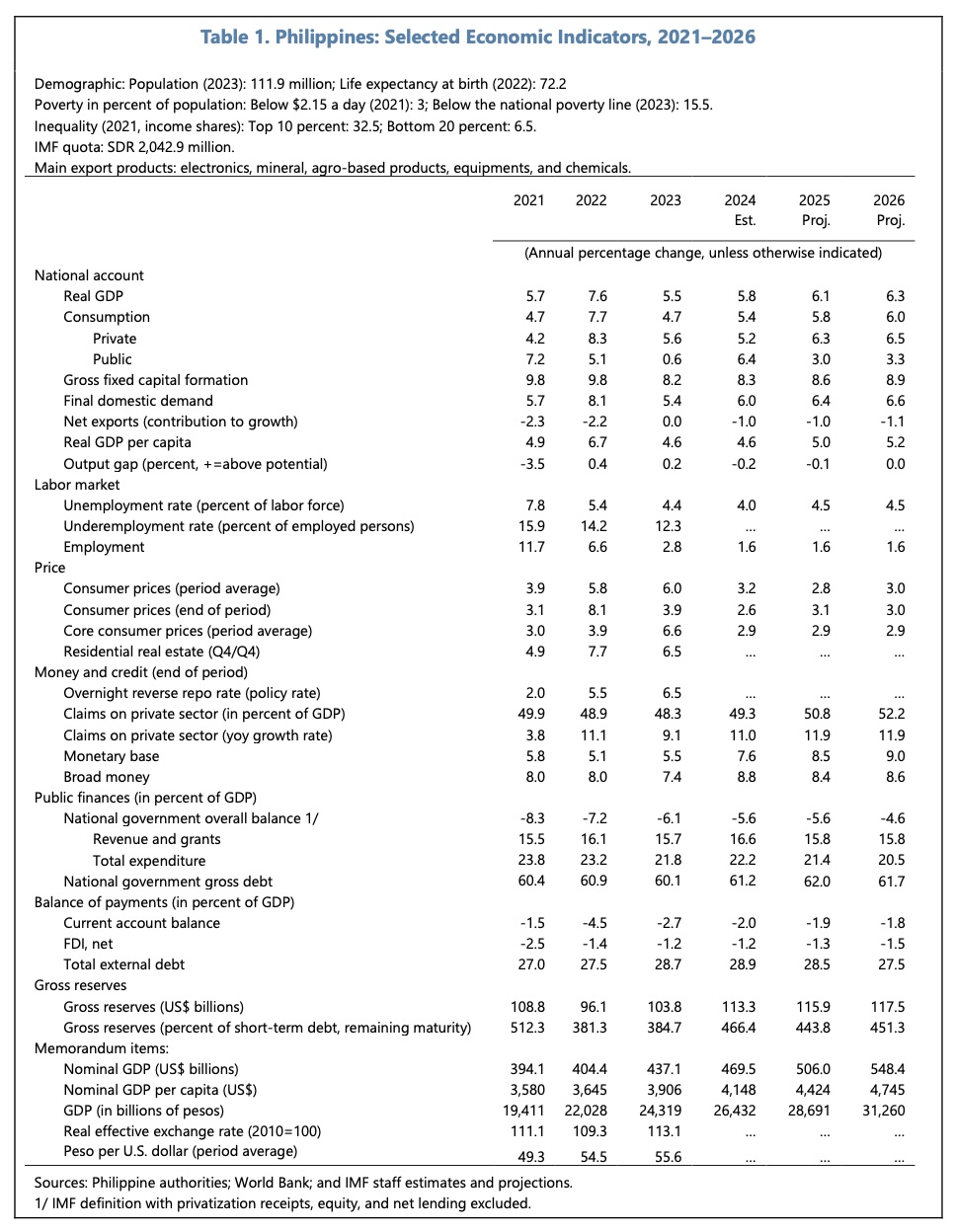

As expected, growth in real GDP moderated after the strong rebound in 2022, to 5.5% YoY in 2023. In 2024, it is expected to grow by 5.8% YoY, supported by public consumption and construction, which is being offset in part by El Nino effects and more subdued private consumption.

Per capita gross national income has increased strongly to $4,230 in 2023, and the Philippines is well-positioned on the path towards middle income status.

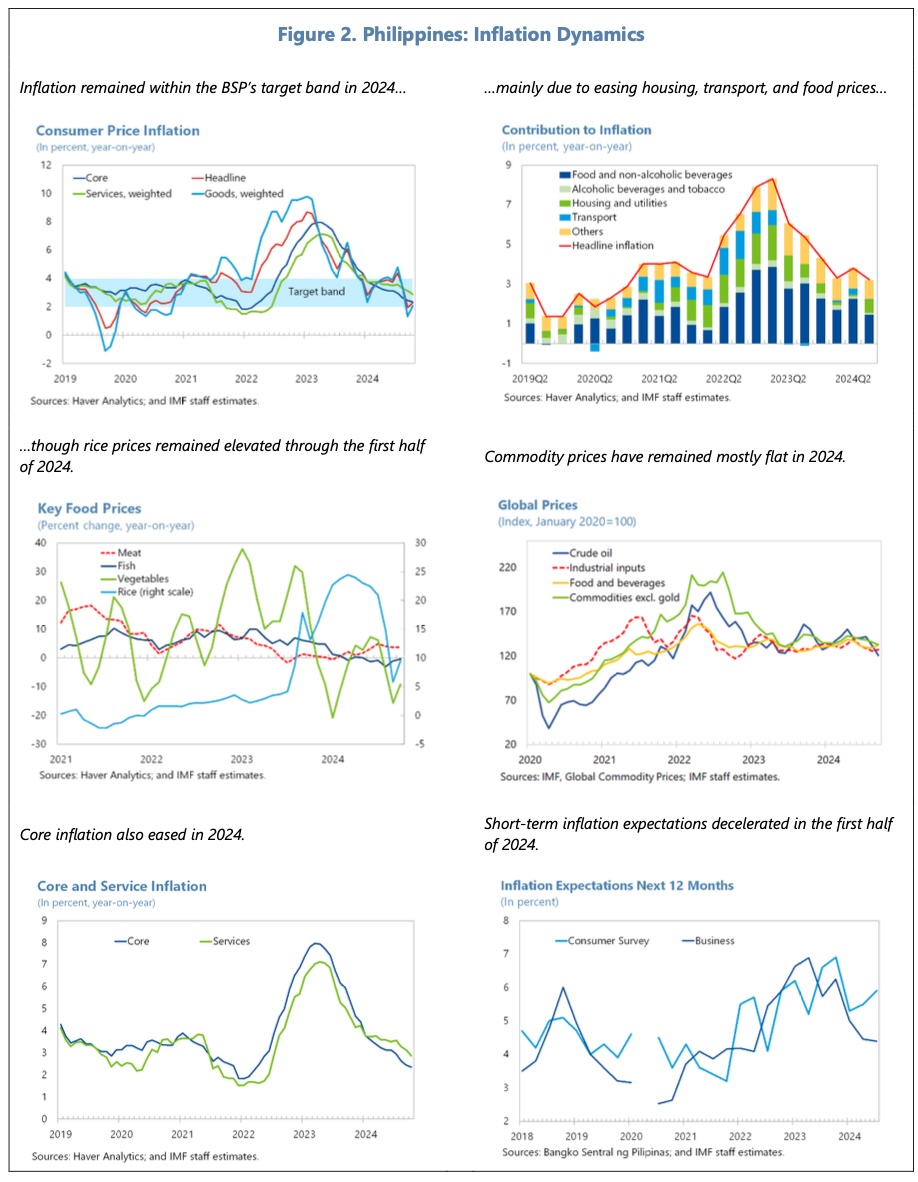

Inflation has been on a declining trend, falling to 2.3% YoY (headline rate) and 2.4% (core rate) in October 2024. YTD, headline inflation has averaged 3.3% YoY. Core inflation is forecast to settle at around 3% YoY in 2024-2026.

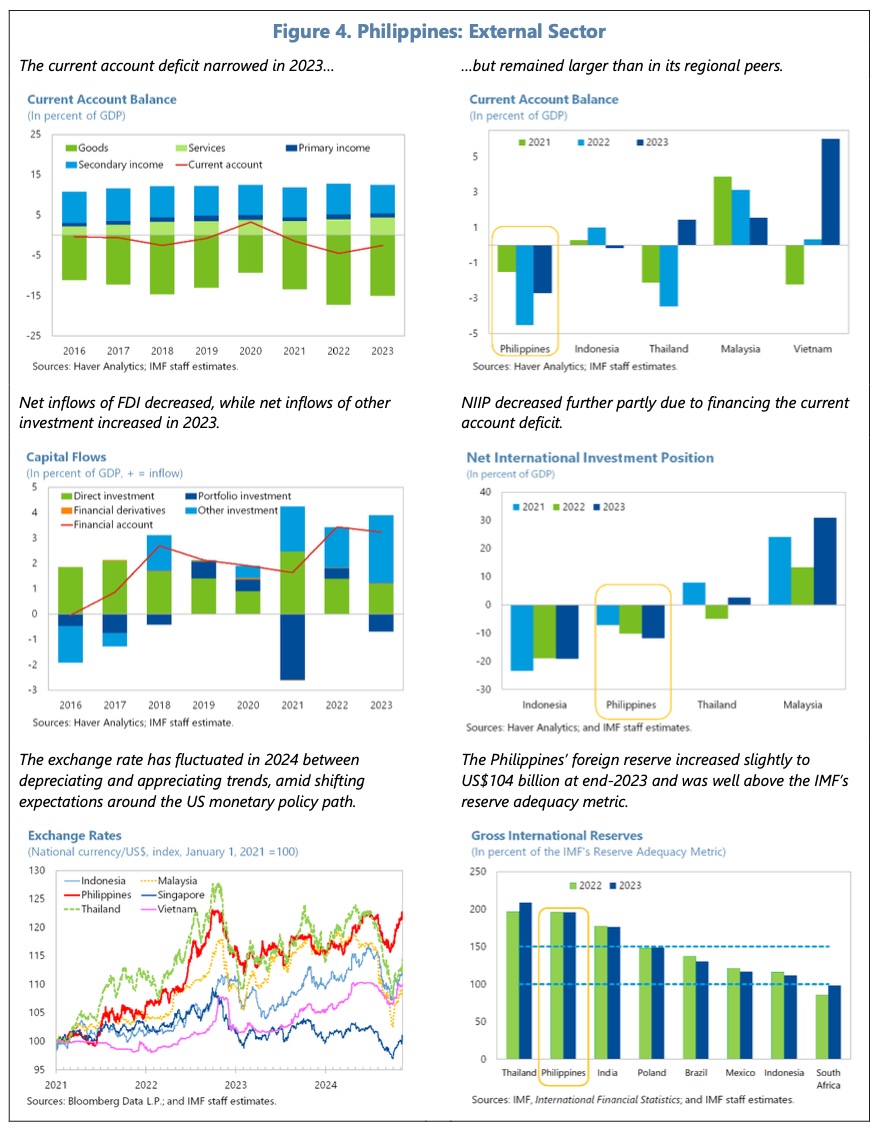

The current account deficit has fallen from 4.5% GDP in 2022 to 2.7% GDP in 2023, and is expected to decline further, to 2.0% GDP in 2024. Lower commodity prices and a gradual pick-up in tourism and business process outsourcing are supporting the trend. Gross international reserves have recovered, from a low of $93bn to $112bn in October 2024. This is seen as a comfortable level, equivalent to nearly 8 months of imports.

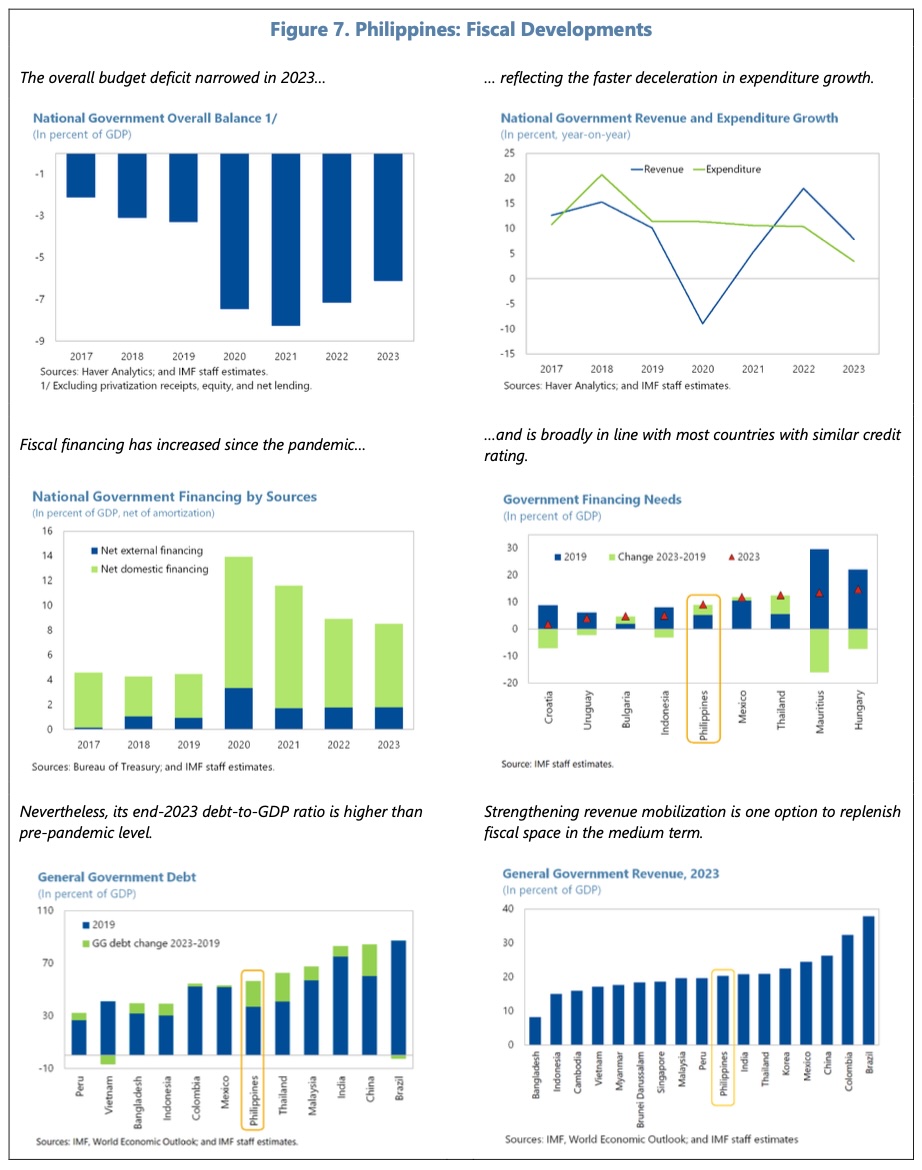

The fiscal deficit declined from 7.2% GDP in 2022 to 6.1% GDP in 2023, as a result of lower current spending. The stock of national government debt has declined from 60.9% GDP in 2022 to 60.1% GDP in 2023.

Looking forward, the IMF expect growth to be supported by disinflation and gradually declining borrowing costs. They forecast real GDP growth to recover towards their estimate of the sustainable rate of 6% to 6.3% in 2025-2026.

The risks, however, are skewed to the downside – with commodity price volatility, new supply shocks, geopolitical/trade tensions, and the possibility of stalled reform momentum being areas of potential concern, alongside natural disasters/extreme climate events.

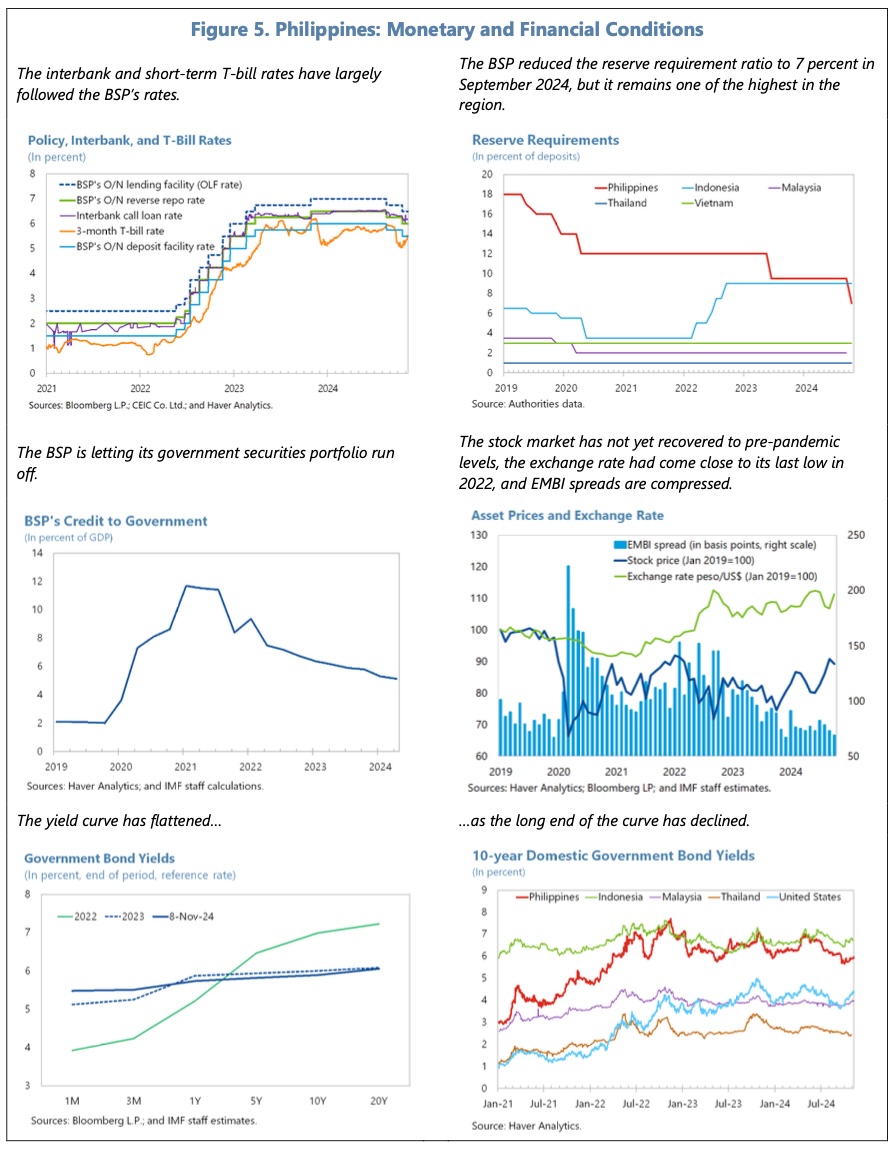

In their assessment, the IMF’s directors have reiterated their support for the authorities’ monetary and fiscal response to the events of 2022. They believe the central bank (BSP) has room to ease the policy rate gradually towards a neutral stance, as inflationary pressures ease and the output gap turns negative. Nonetheless, as inflation risks are tilted to the upside, they caution that the BSP will need to maintain a data-dependent approach, and carefully to manage expectations.

In recent years, inflation has been more influenced by supply-side factors than by changes in demand, reflecting the Philippines’ reliance on imports of fuel and food, and limited price controls. Given the shallow FX market and the non-linear impact of FX fluctuations on inflation expectations, the IMF think it may be appropriate for the central bank to use a FX intervention approach in monetary policy, but only on a temporary basis in certain restricted circumstances.

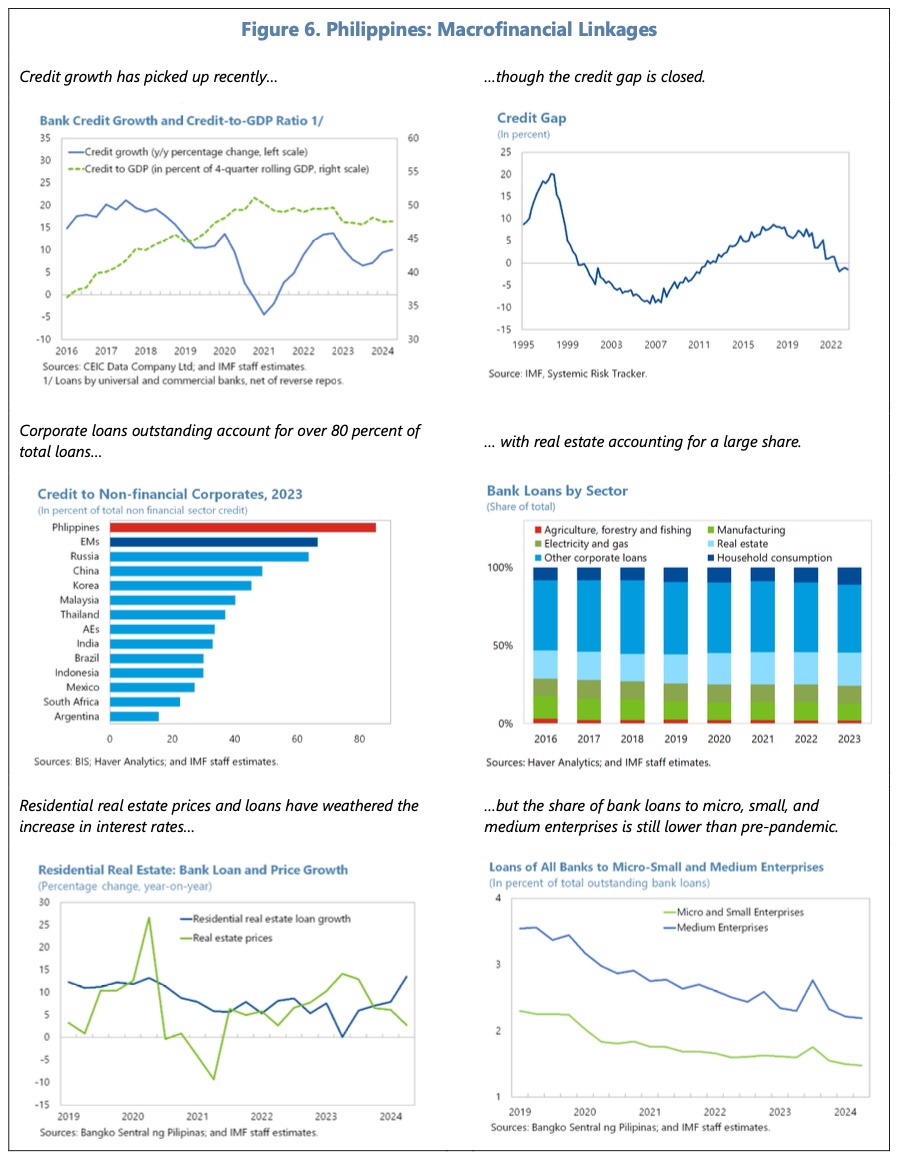

The directors are comfortable with the liquidity and capital adequacy in the banking system. System-wise NPLs stand at 3.5% of loans, but there are some concerns about persistently high vacancies in commercial real estate, where rents have been falling. They directors also note that non-performing housing loans are quite high (6.8%) and that the strong growth in consumer loans (about 25%) warrants watching: real estate loans represent 20% of banking loans, whilst consumer credit stood at 10.6% of loans at end-June. External borrowing by corporates has been relatively stable at under 10% GDP, though the IMF note that hedging markets are underdeveloped.

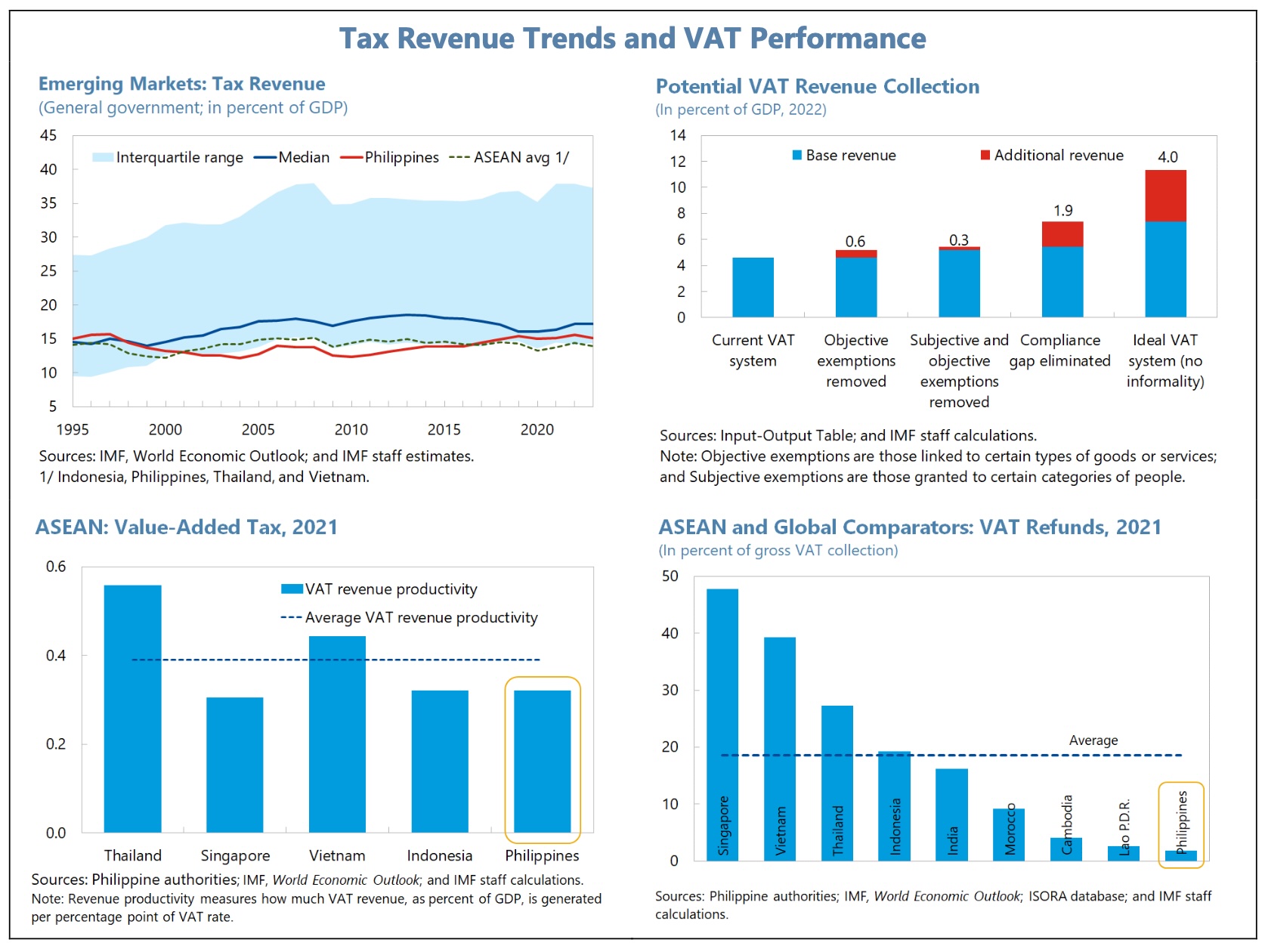

On the fiscal front, they agree that a more gradual pace of consolidation is now appropriate. The target for the 2028 deficit has been raised from 3% GDP to 3.7% GDP, reflecting the same pace of consolidation (0.5% pa.) but from a higher base in 2025. (This reflects greater concerns over the near-term growth prospects.) The IMF favour a concrete and sustainable plan which replenishes fiscal space by raising tax revenues (14.1% GDP in 2023) and implementing expenditure reforms. On tax, they have specifically mentioned the implementation of shelved measures on excise, enhanced VAT efficiency, improved tax administration, and the effective control of incentives (eg. through the expensing of capital spending rather than expanding tax holidays).

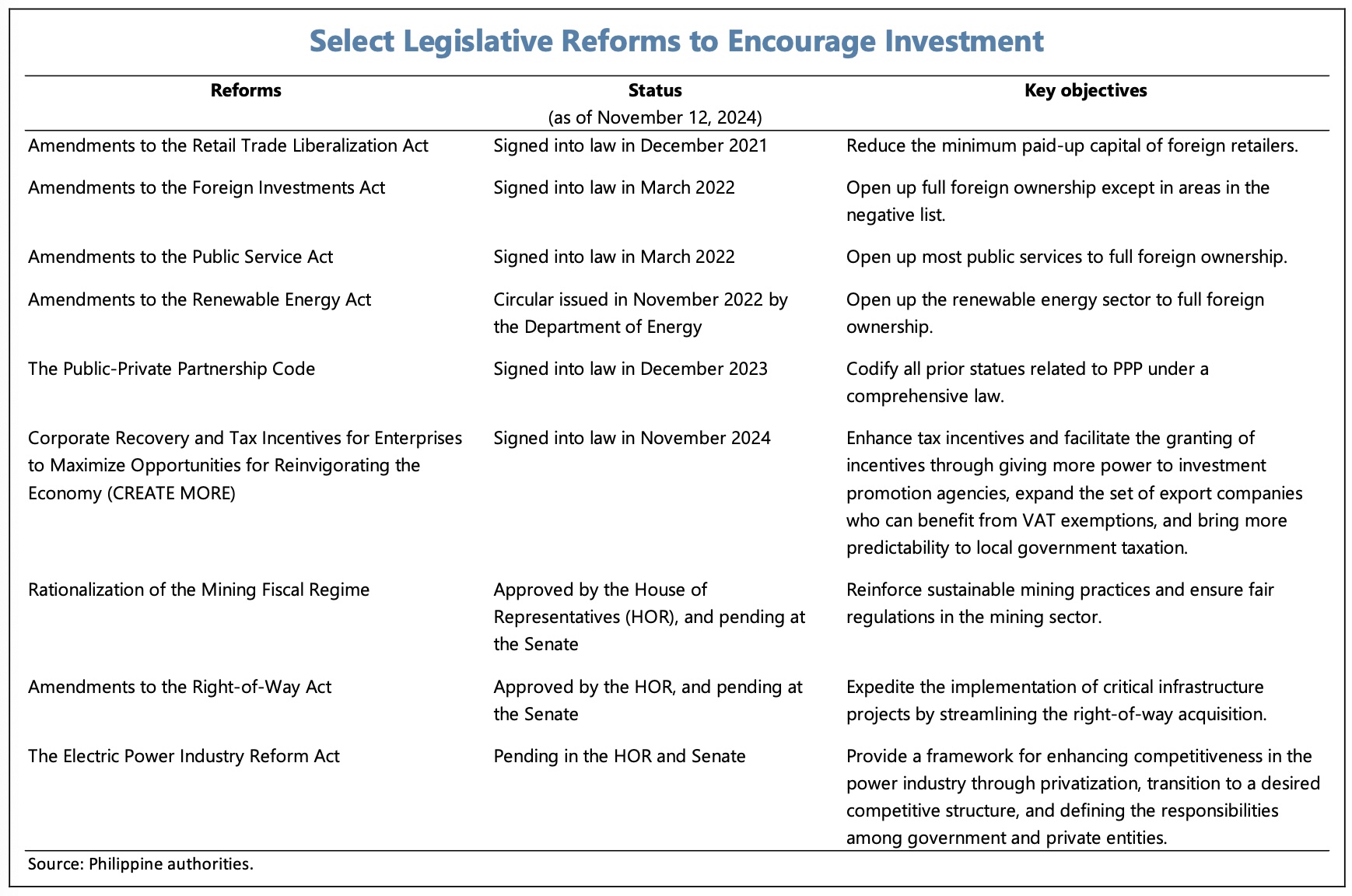

Recent legislative reforms are expected to support the roll-out of Public Private Partnerships (PPP), as well as an increase in Foreign Direct Investment (FDI).

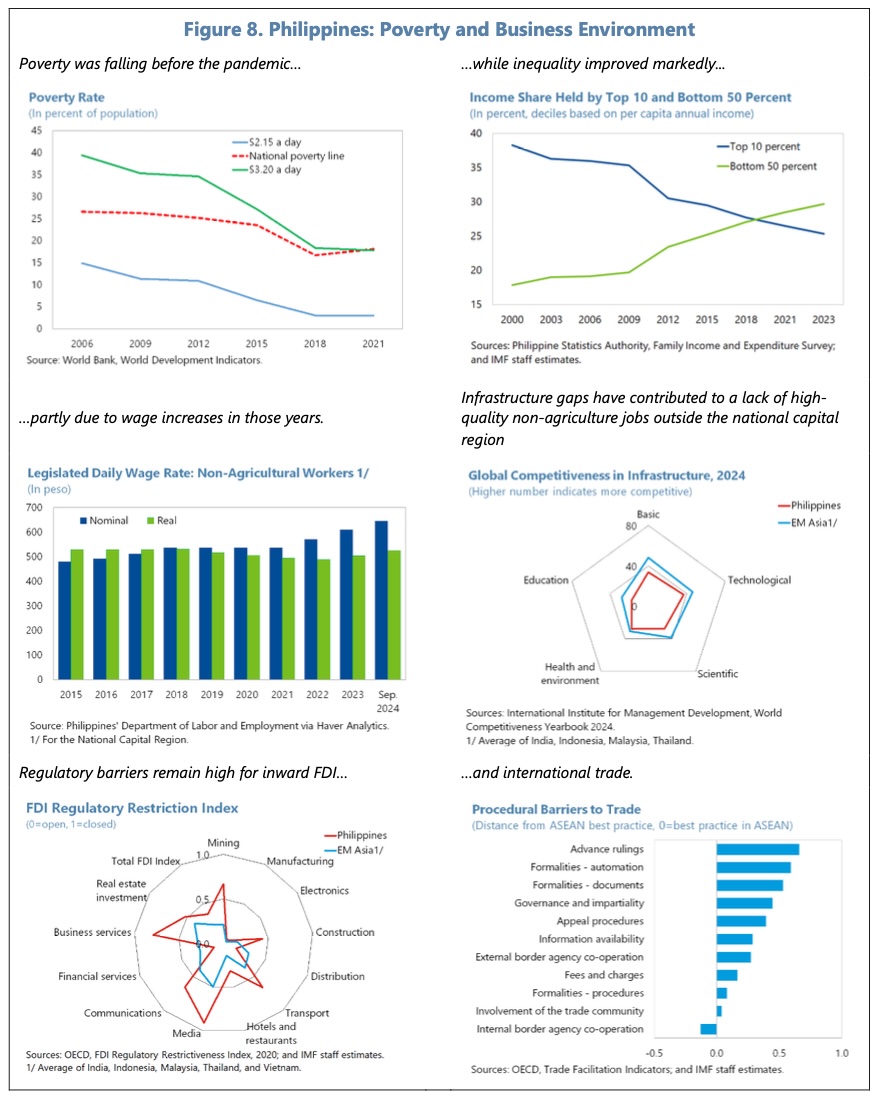

Supported by its demographic profile and abundant natural resources, the IMF are confident about the Philippines’ long-term development potential. Structural reforms are needed, however, if it is to be fully realised. The IMF have highlighted policies to boost job creation, productivity and FDI, whilst reducing poverty and inequality, and also increasing resilience to climate change.

![]()

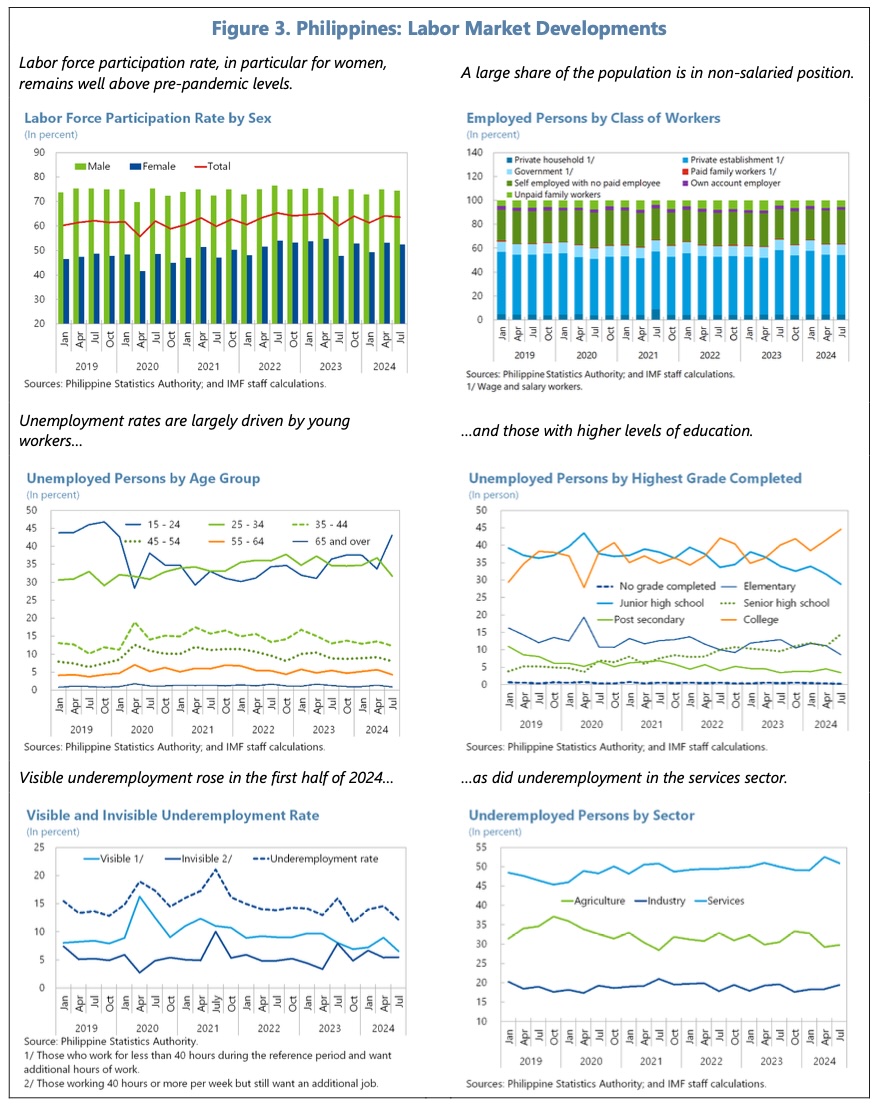

Particular areas of focus include upgrading infrastructure (electrical grids, renewable energy, roads, ports, digital infrastructure), investing in healthcare and education, addressing land fragmentation and low agricultural productivity, and enhancing governance, particularly at the local government level. Digitisation is seen as a powerful tool that can help with education, increased financial inclusion and public spending efficiency. Educational standards among primary school-age children are currently low (90% learning poverty rate), and there is scope to raise the female labour force participation rate (53.4% in September 2023).

Progress is being made in strengthening financial supervision and regulation, and the initial judgement of the Financial Action Task Force, issued in October, is that the Philippines has ‘substantially completed its plan to exit from the grey list of jurisdictions with AML/CFT deficiencies.’ However, the IMF believe that work in both of these areas must continue.

The following charts and tables, taken from the IMF’s article IV report, summarise their perspectives on the Philippines economy.

For the full report, please use this link to the IMF’s website: IMF Report