In June 2025, the World Bank published the latest in its bi-annual series of reports on the Indonesian economy.

Summary

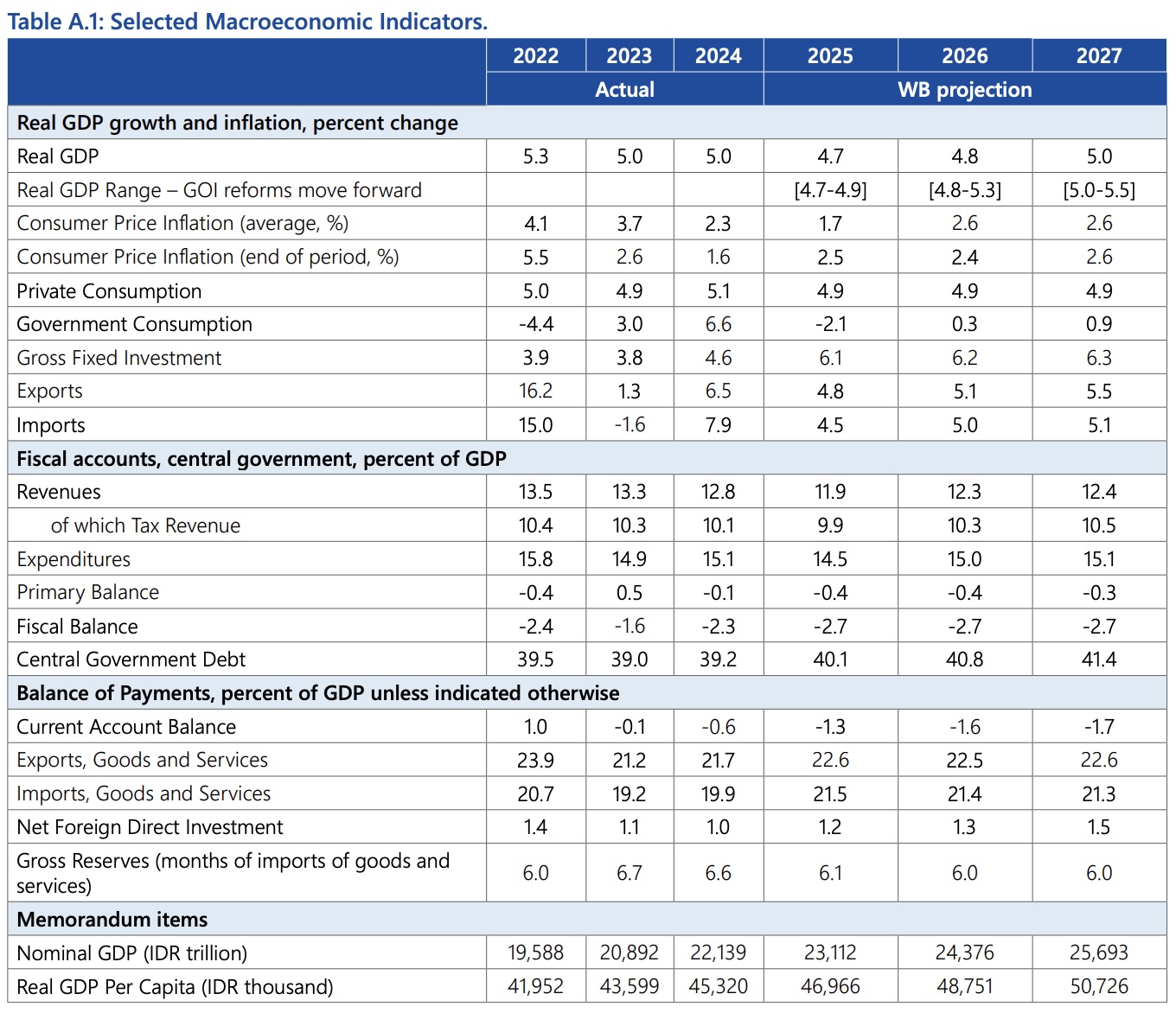

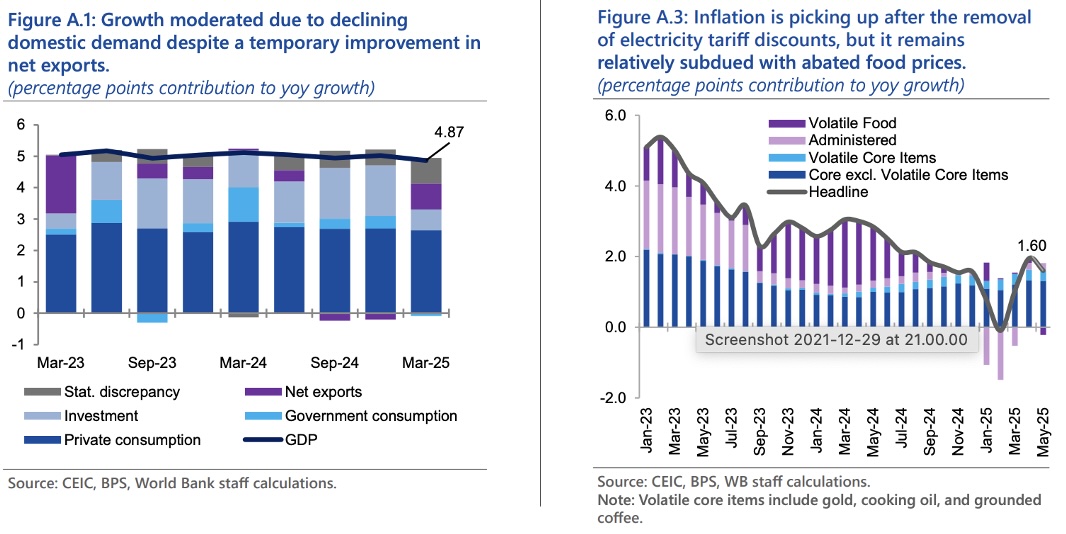

The economy remains resilient amid worsening global conditions. Real GDP grew by 4.9% YoY in Q1 2025, slightly slower than the trend in the post-pandemic period. Budget efficiency measures caused public spending to contract, whilst caution over the global outlook constrained private investment in manufacturing and construction. Lower commodity prices impacted the terms of trade. Agriculture and services performed better.

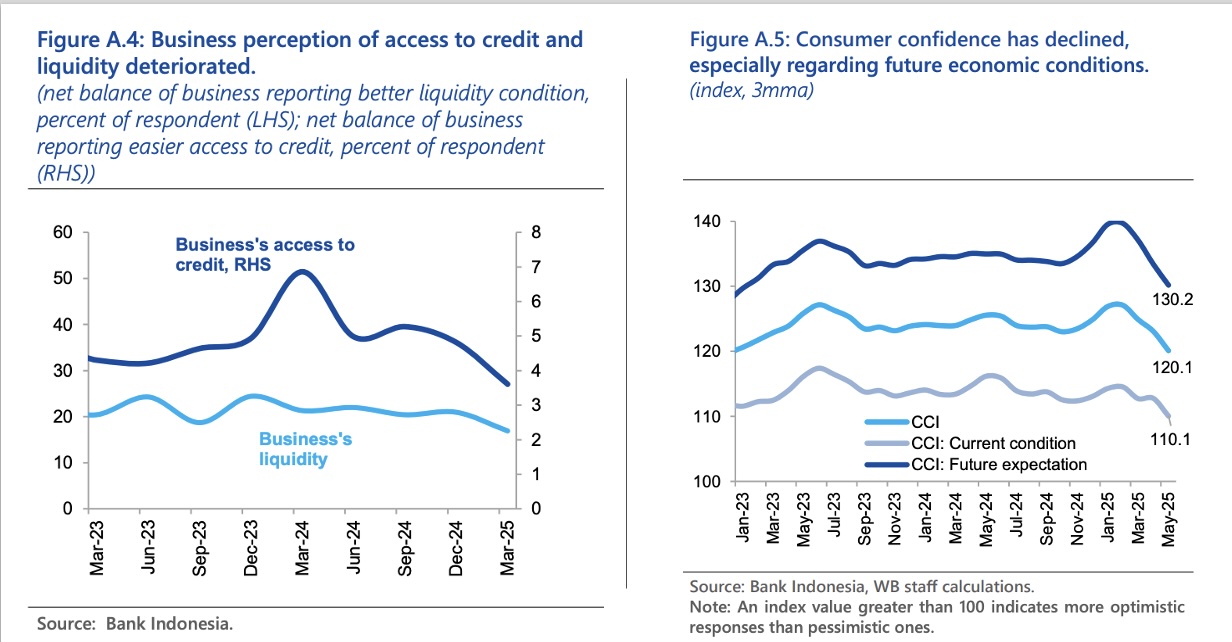

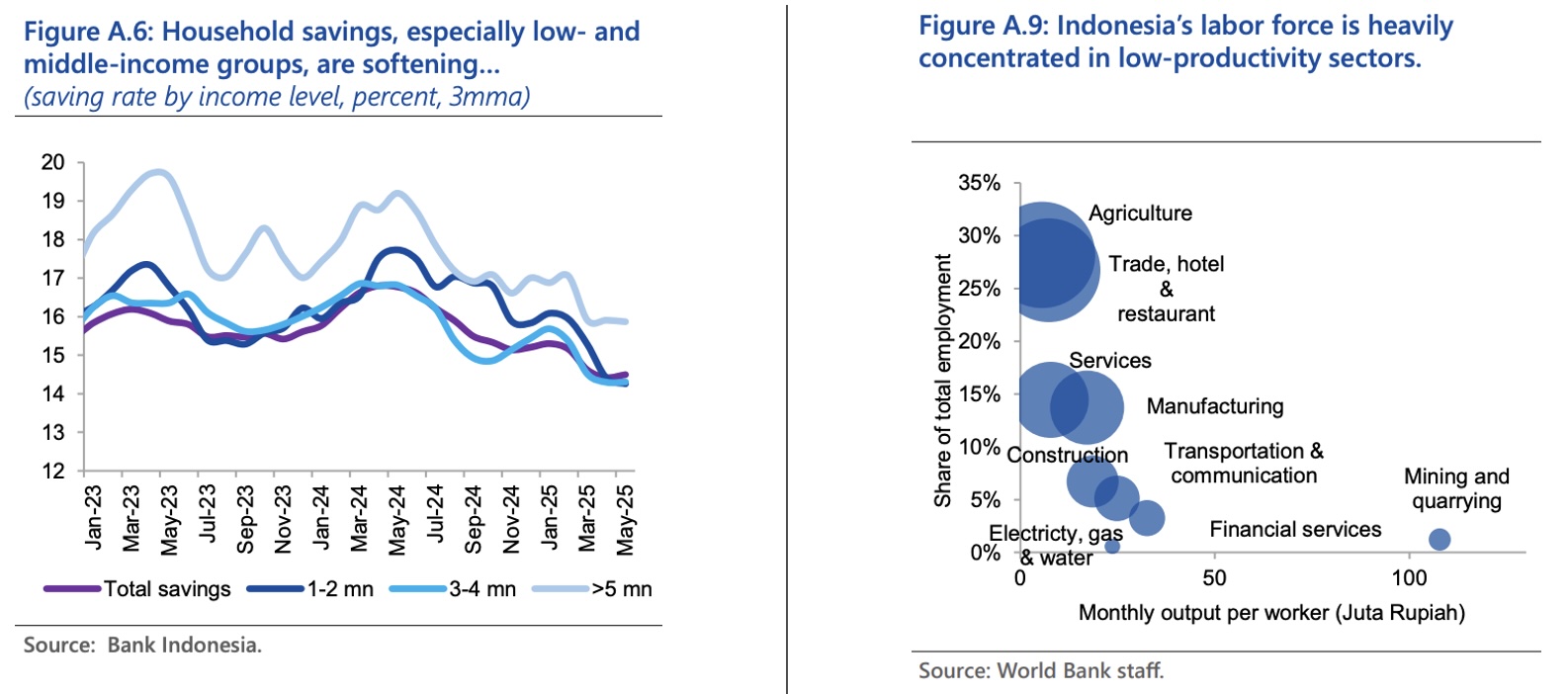

Businesses have been reducing inventory and hiring in order to conserve liquidity. Middle-class households in particular have been cautious on spending since the pandemic, as savings have been decreasing and a lack of quality jobs has been limiting income growth. (52% of new jobs created in 2024 were in low value-added sectors.)

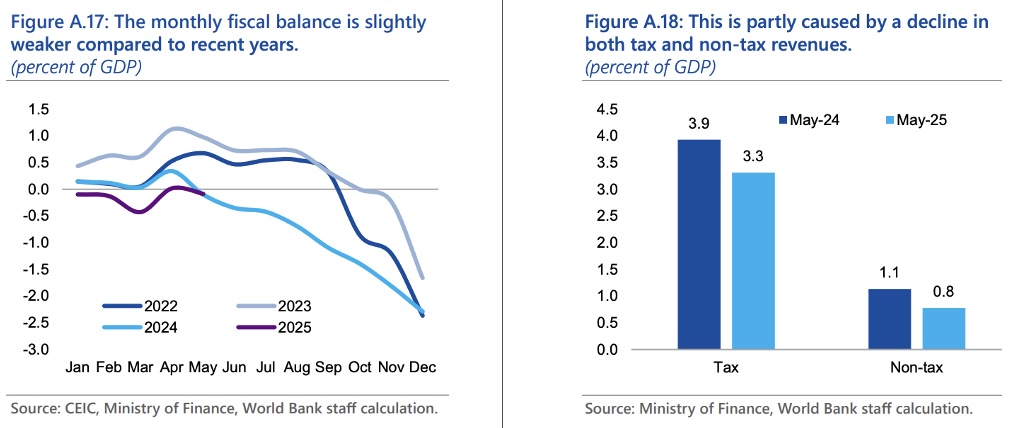

A fiscal efficiency drive, equivalent to 1.3% GDP, has been implemented by the government to create space for priority programs and consumption stimulus, amid revenue shortfalls. Temporary factors associated with the new ‘Core Tax’ digital system have caused tax revenues to decline. Larger-than-expected tax rebates, lower SOE dividends, and lower commodity prices have also had an impact.

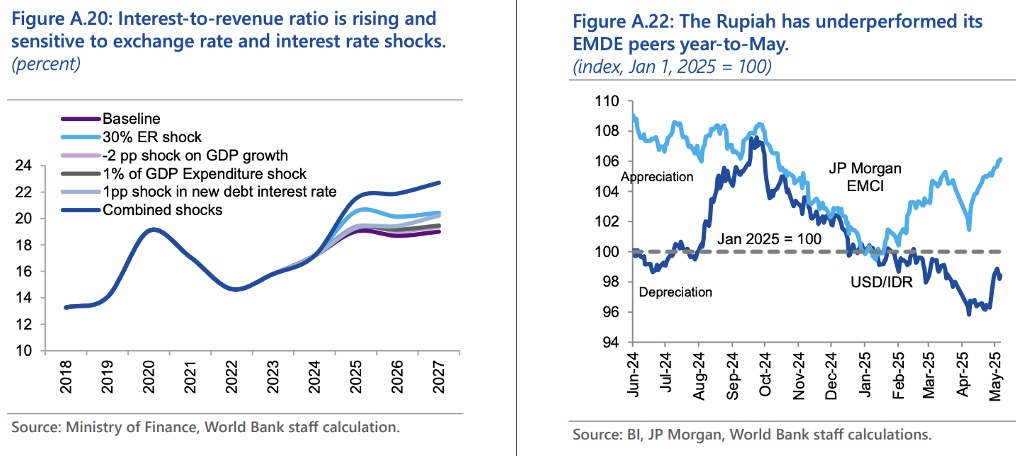

After a period in which global financial volatility affected confidence, the equity market and FDI, the central bank (BI) has intervened to stabilise the Rupiah. Despite a drop in FX reserves to a still-adequate 6.2 months of imports, monetary policy has now started to ease, BI lowering the policy rate by 50bps YTD.

Looking forward, the World Bank is confident that the economy will continue to grow at a medium-term rate of around 4.8%. Private consumption growth should benefit from low inflation and social assistance programmes, whilst investment is expected to pick up with the government’s housing program and projects from Danantara, the new sovereign wealth fund.

The fiscal deficit is expected to hold at around 2.7% GDP, with spending set to increase gradually from 2027 with priority programmes and rising interest payments. To cover the increase, the government plans to tax digital transactions, raise mineral and coal royalties, and improve tax administration. Meanwhile, external financing needs will gradually rise with a widening current account deficit and increasing public debt amortisation.

In an environment of greater global uncertainty, the government has been developing a programme of deregulation – reforms to licensing, investment restrictions, trade and logistics, as well as digital services. The World Bank believes these have the potential to expand the economy’s capacity, unlock FDI, boost investment returns and productivity, and so raise real GDP growth to 5.3% to 5.5% in 2026-27.

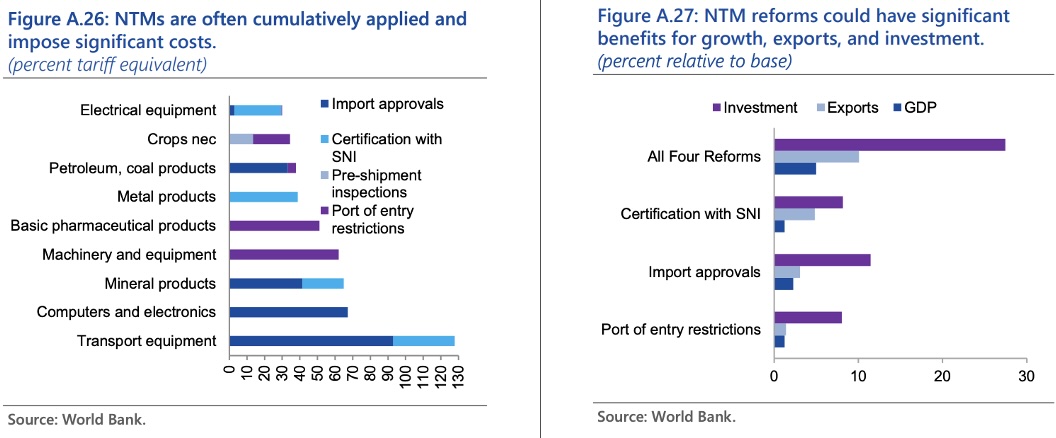

The Bank has highlighted four policy priorities: (i) deregulating trade and investment by removing non-tariff measures (NTMs), streamlining import approvals, relaxing local content requirements and improving the national logistics ecosystem (ii) improving policy communication and providing timely macro-fiscal data to reduce market uncertainty (iii) protecting capital spending, on the grounds that a $1 cut in public investment can lower GDP by $1.3 in the long-term (iv) executing the Danantara strategy efficiently and transparently, in accordance with best international practice.

In particular, the Bank believes that reforms to non-tariff trade barriers have the potential to boost exports by 10% and investment by 27% over the medium term.

The following table and charts, extracted from the World Bank’s report, should help to highlight some themes.

For the full report, please use the following link to the World Bank’s website: World Bank Report

The report includes a section on President Prabowo’s plans for investment in three million new housing units annually, and those steps which the Bank thinks will be necessary if the effort is to be successful.