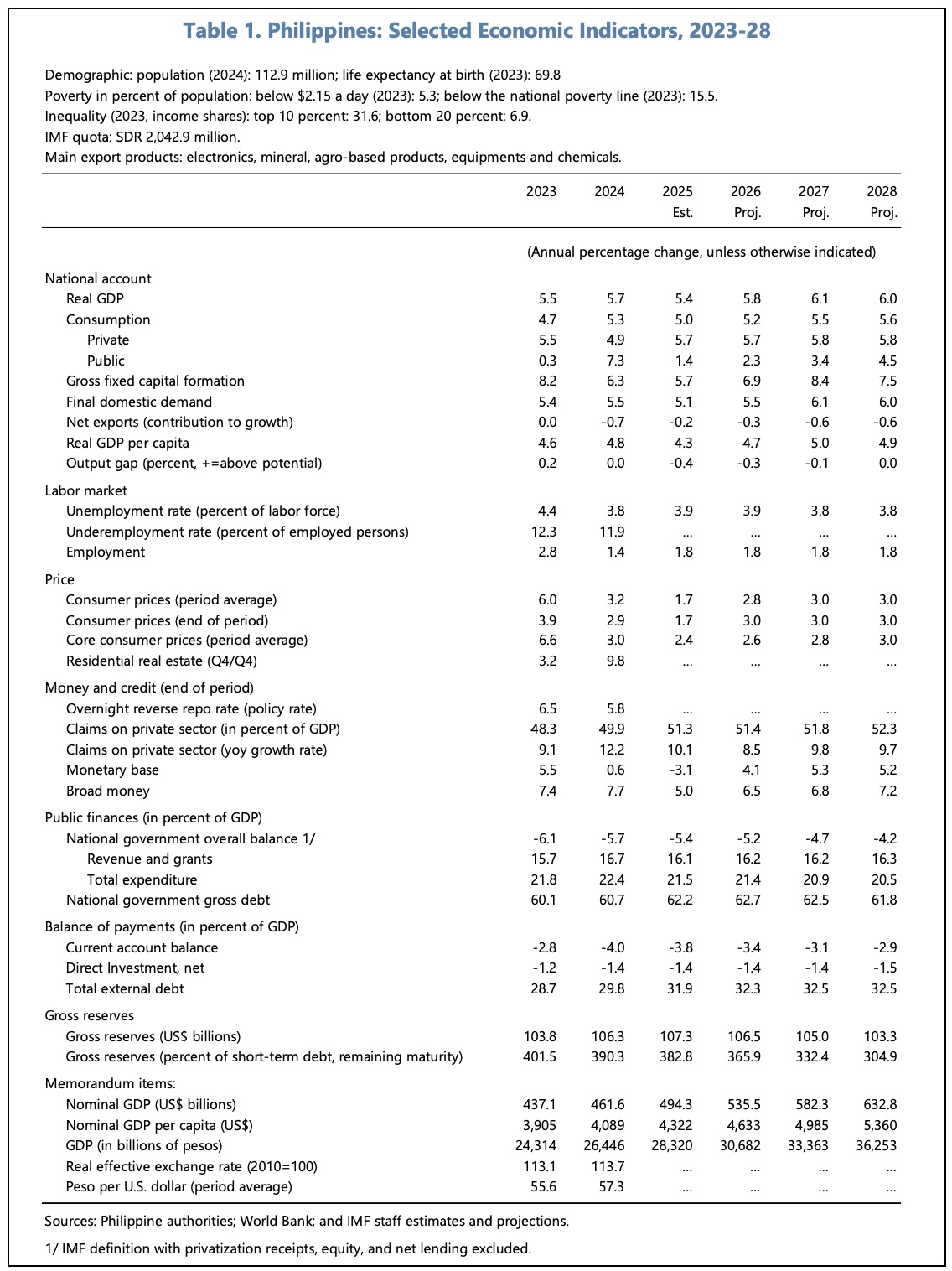

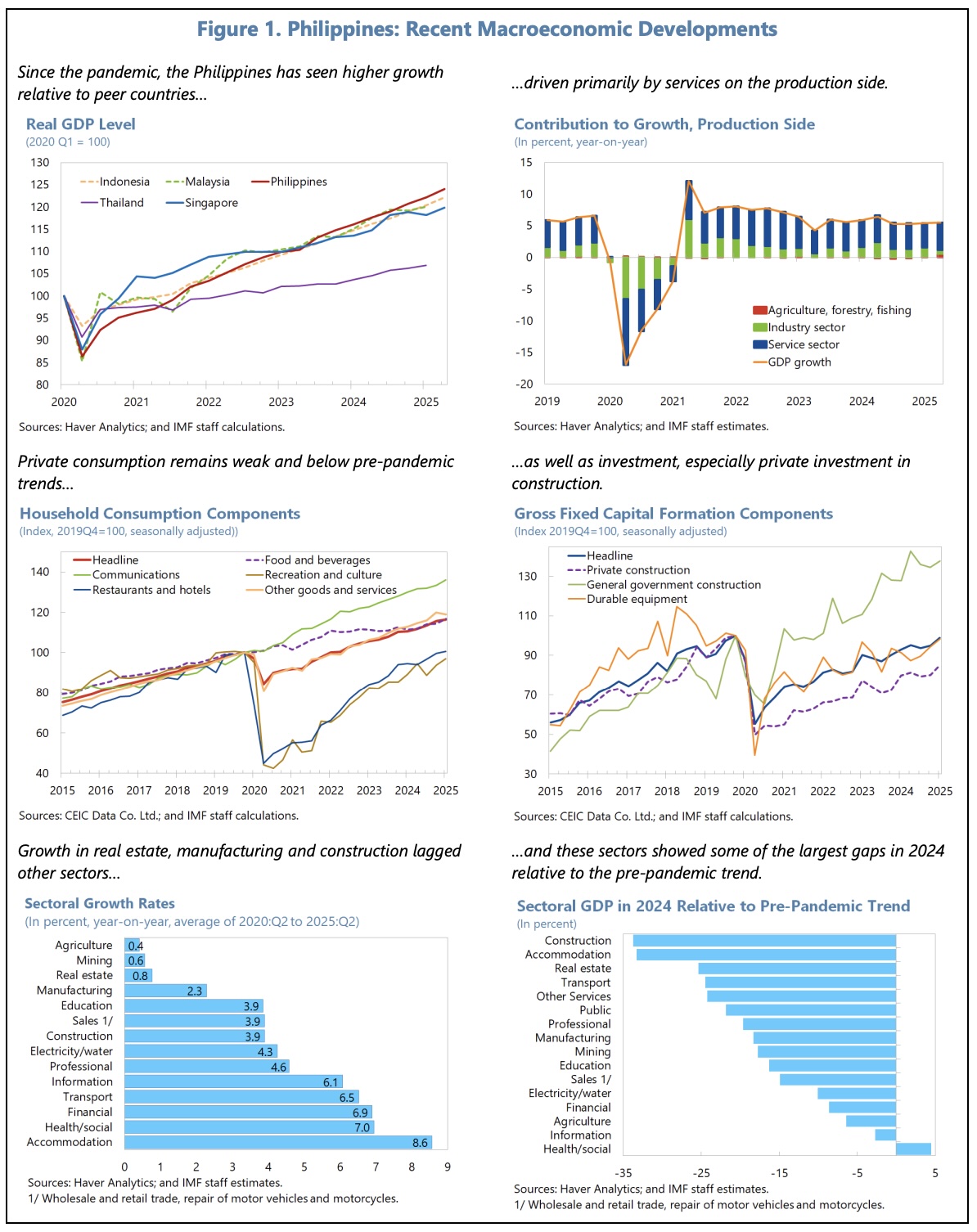

In its most recent forecasts for the Philippines economy, the IMF have lowered their real GDP growth expectations for 2025 from 6.1% YoY (in December 2024) to 5.4%, and for 2026 from 6.3% YoY to 5.8%. Their estimate for final domestic demand growth in 2025 has fallen from 6.4% YoY (in December 2024) to 5.1%, following a weaker than expected print for growth in Q3 2025. The medium-term potential real GDP growth estimate remains broadly unchanged, at around 6%.

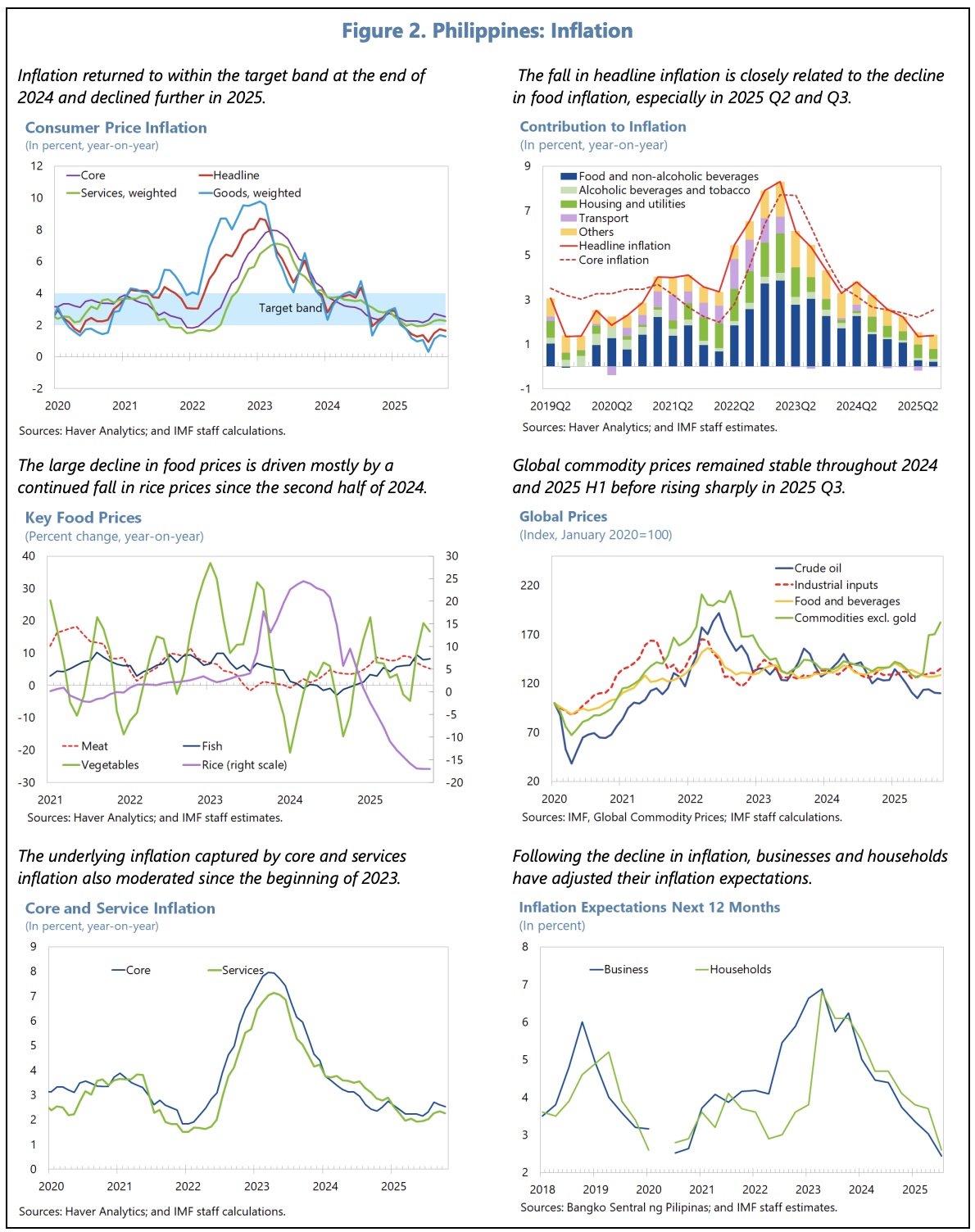

At the same time, the IMF have lowered their average CPI forecast for 2025 from 2.8% to 1.7%. The forecast for 2026 has been lowered by a lesser 0.2%, from 3% (in December 2024) to 2.8%.

Monetary and Exchange Rate Policies

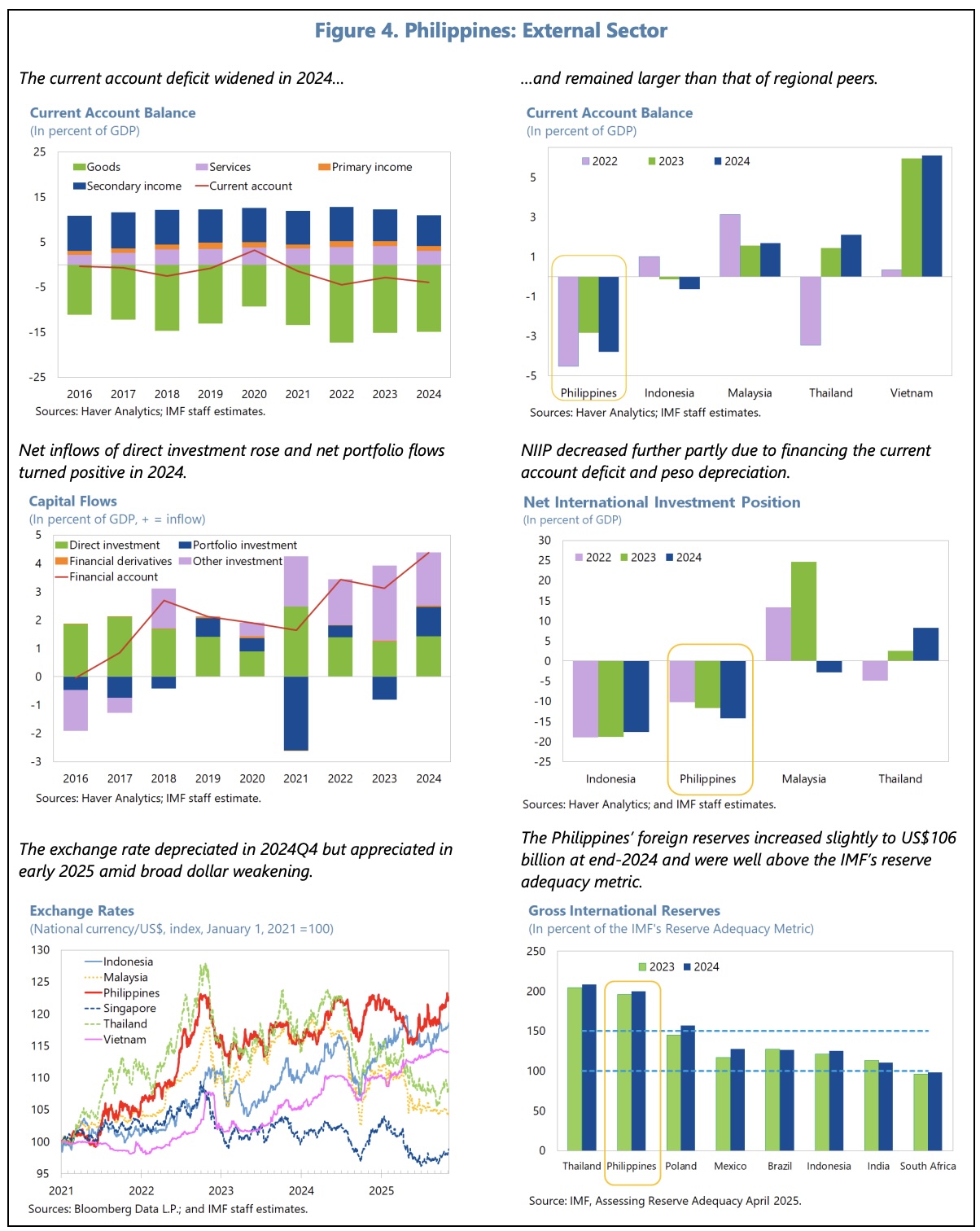

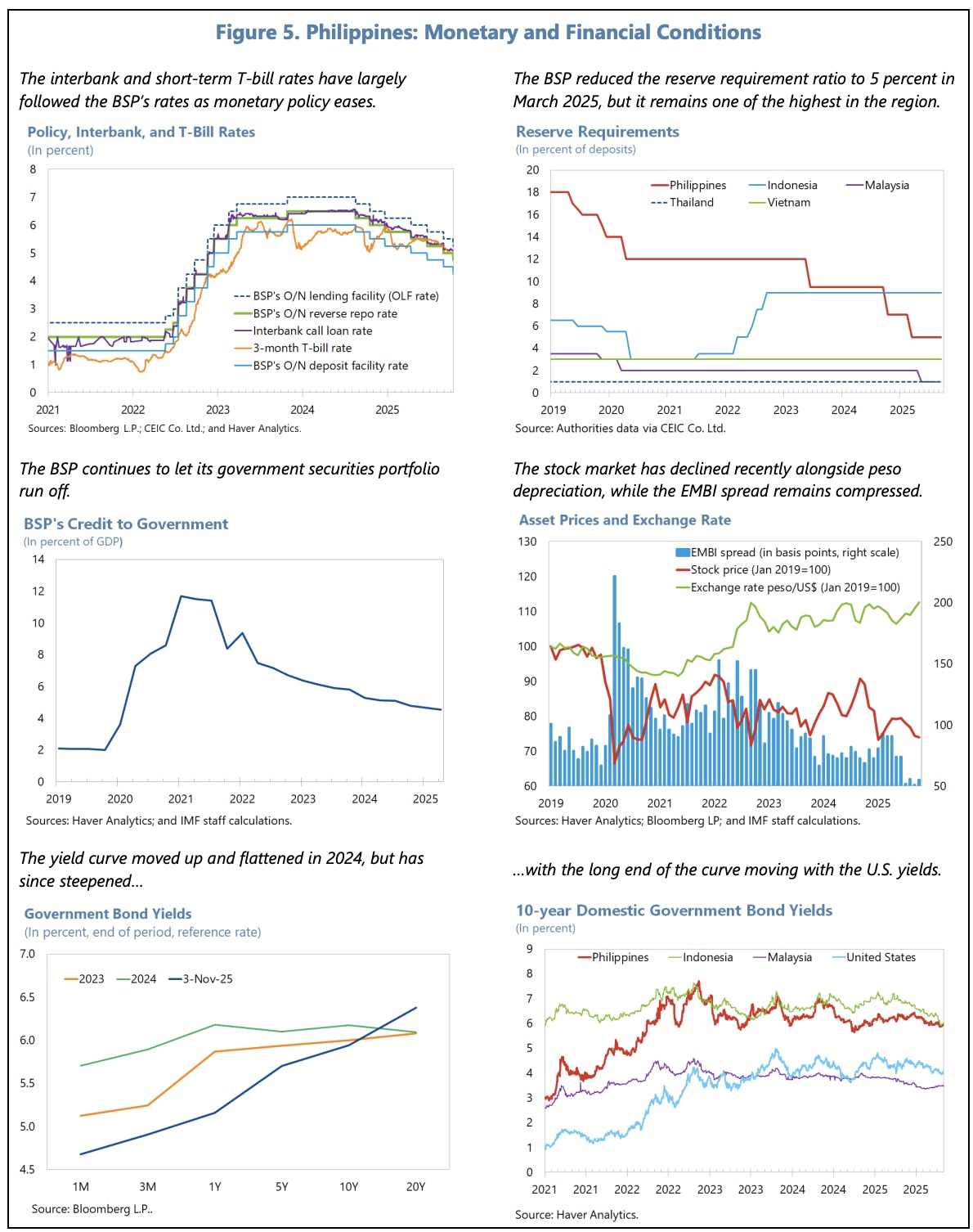

Principally because of the deterioration in the global political and trade background, but also because of knock-on effects from corruption allegations related to flood control projects and the increasing possibility of extreme climate events, the IMF believe the risk to their growth forecast is on the downside. With inflation expectations well-anchored, they therefore support a more accommodative monetary policy stance which remains data-driven, with the exchange rate paying its role as a shock-absorber (ie. with interventions being used only to address disorderly market conditions).

Fiscal Policies

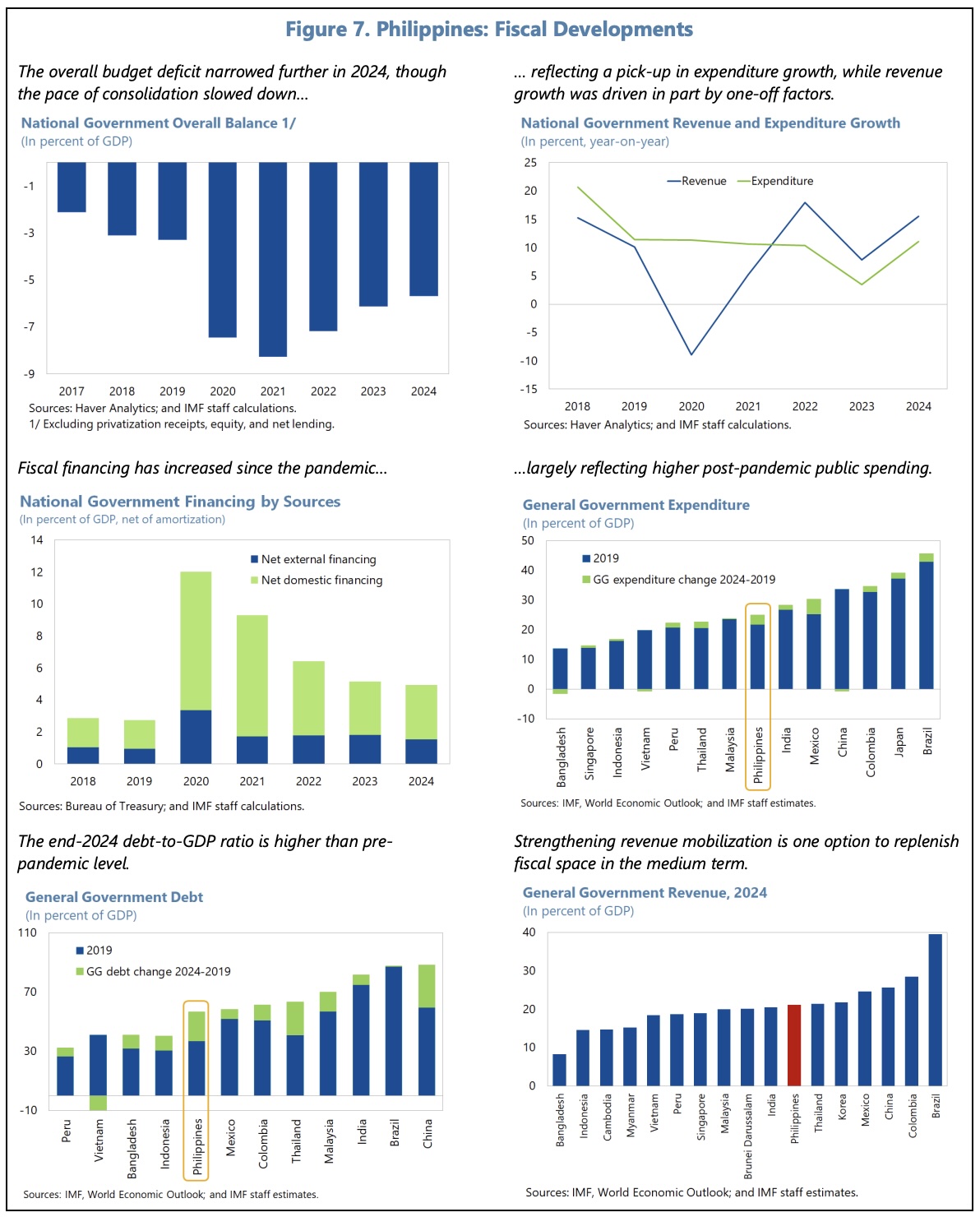

Longer term, the IMF agree with authorities’ plans for gradual fiscal consolidation. (Currently, the plans envisage a decline in the fiscal deficit to 3.1% GDP in 2030 – ie. by around 0.5% pa from 2027.) However, the IMF have also remarked that the introduction of concrete tax and expenditure measures would improve transparency and confidence.

In particular, the IMF favour measures to raise tax revenues over measures to reduce spending, as they typically have lower multiplier effects. Alongside tax administration reforms, they have mentioned measures to improve VAT efficiency, measures with positive health benefits (eg. duties on sugared drinks and certain pre-packaged foods), steps to lower VAT exemptions on the ownership of dwellings, and continuous monitoring of the cost of tax incentives with a view to streamlining them. The IMF have indicated they do not favour the general tax amnesty (GTA) being considered, as ‘anticipated GTAs lower regular voluntary compliance.’ Instead, their preference is for voluntary disclosure programmes.

On the expenditure side, the IMF have highlighted the scope for measures to improve public financial management, spending efficiency, accountability and governance.

Financial Sector Policies

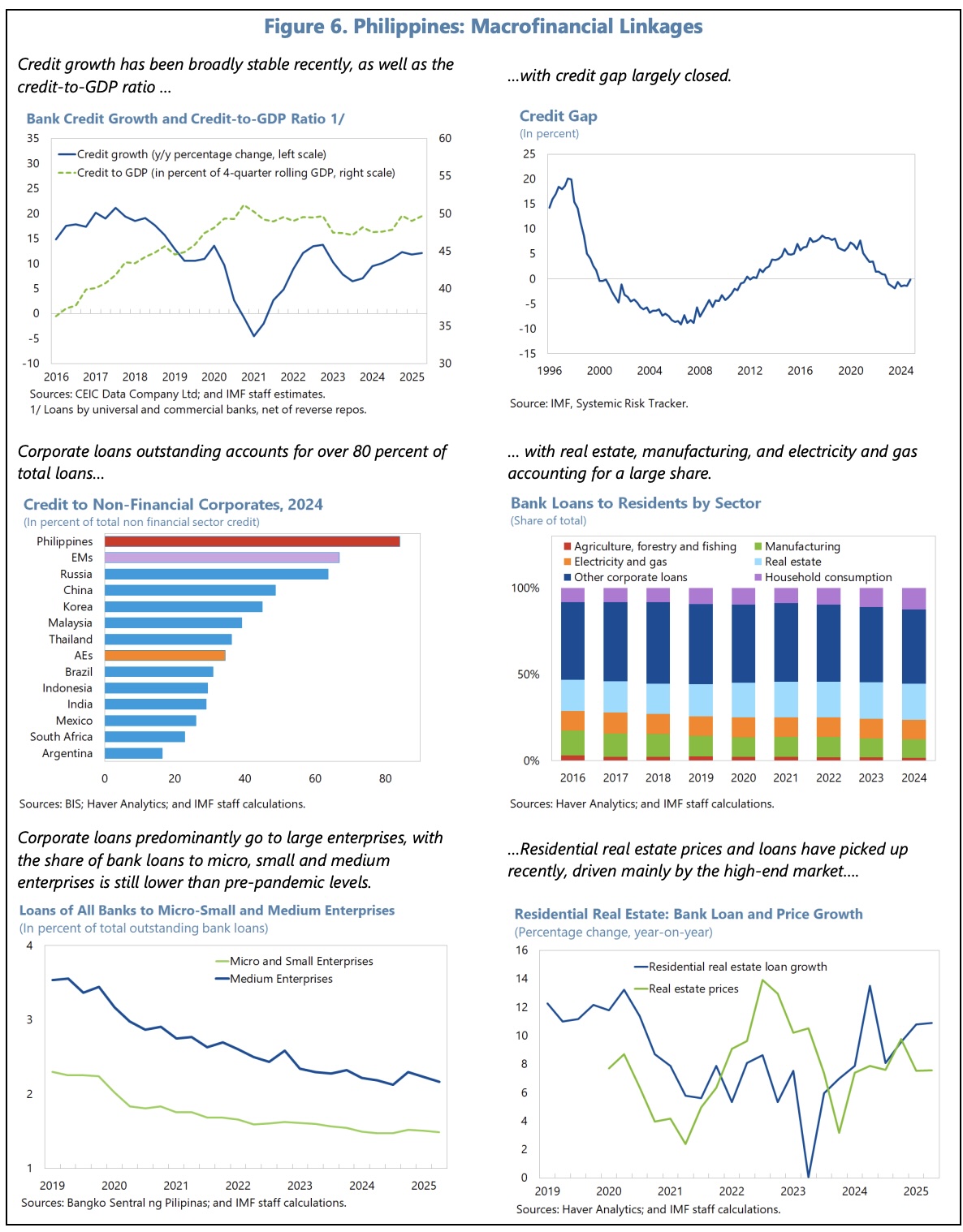

In the IMF’s opinion, systemic financial sector risks are ‘moderate’, as the banking system is well-capitalised, liquid and profitable, it operates to generally conservative lending standards, and has a stable deposit base. Overall credit growth is healthy and the credit gap remains closed. That said, the IMF have suggested that vulnerabilities in real estate in some regions / segments merit close monitoring, as does the growth in credit through NBFIs and digital finance, and the interconnects between banks and some corporates through complex conglomerate structures.

Structural Reforms

The IMF have suggested that priority areas should include:

- the effective implementation of recently ratified reforms to improve the business environment/digitisation

- measures to raise the efficiency of public expenditure and reduce corruption vulnerabilities

- measures to increase resilience to climate change and harness the Philippines’ potential in renewable energy

- investments in education and adaptive social protection

- greater trade integration, to raise productivity and engender a shift to a more diversified growth model

Interested readers may study the full details of the IMF’s Article IV report using the following link to the IMF’s website: Read More