Overview

In the latest of its Article IV consultation reports on the Indian economy, the IMF have welcomed its continued robust performance, and the inroads it has made towards its Sustainable Devlopment Goals (SDGs). Structural reforms – inflation targeting, the introduction of Goods and Services Tax (GST), improved financial regulation for Non-Bank Finance Companies (NBFC), and investments in digital public infrastructure – have served to unlock innovation and financial inclusion.

A firm platform has been established upon which further reforms may be advanced to foster private sector investment and create quality jobs for the growing population. Given openness to international trade and investment, India’s role in Global Value Chains (GVCs) should be well-positioned to increase.

Recent Developments

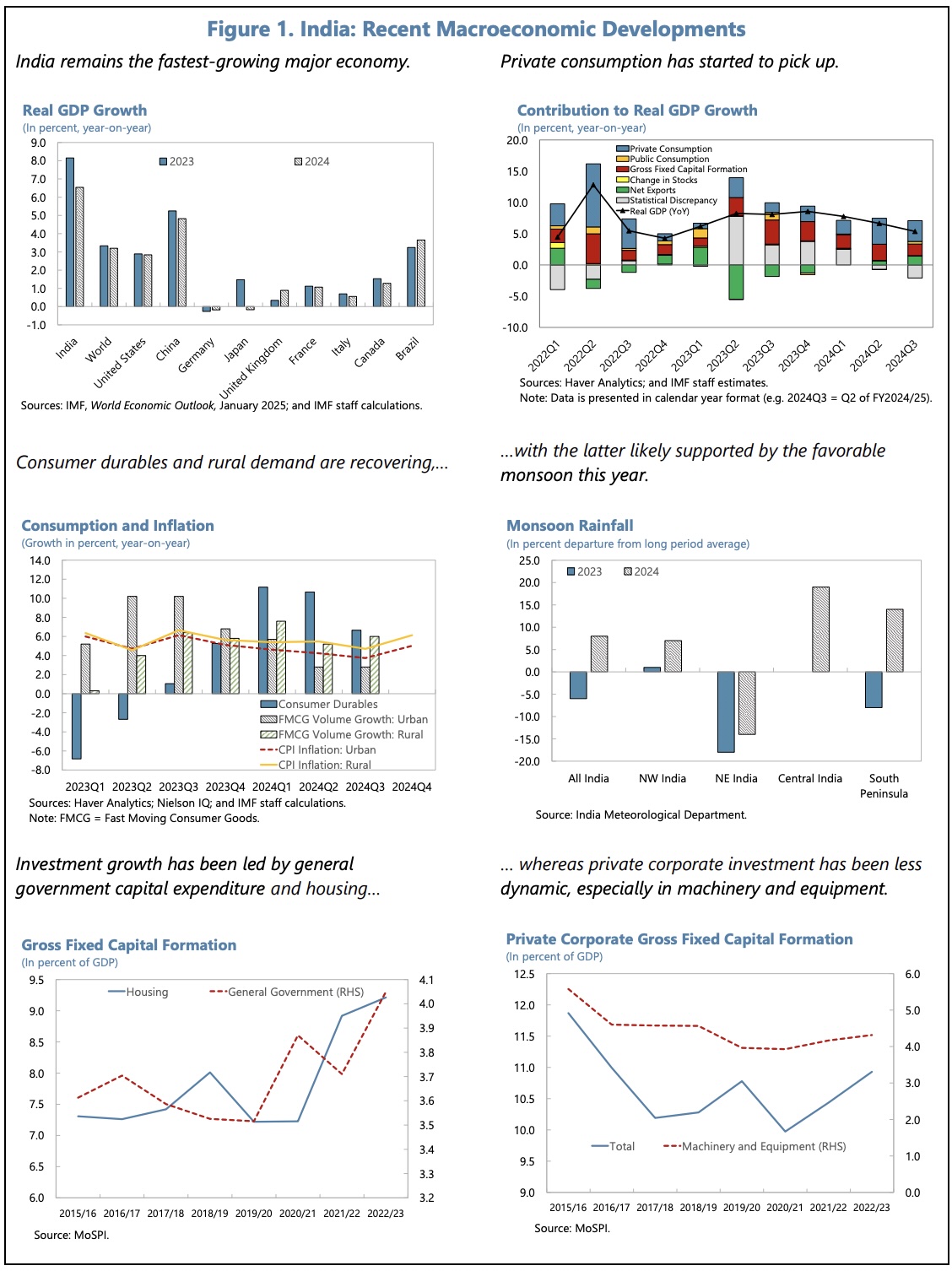

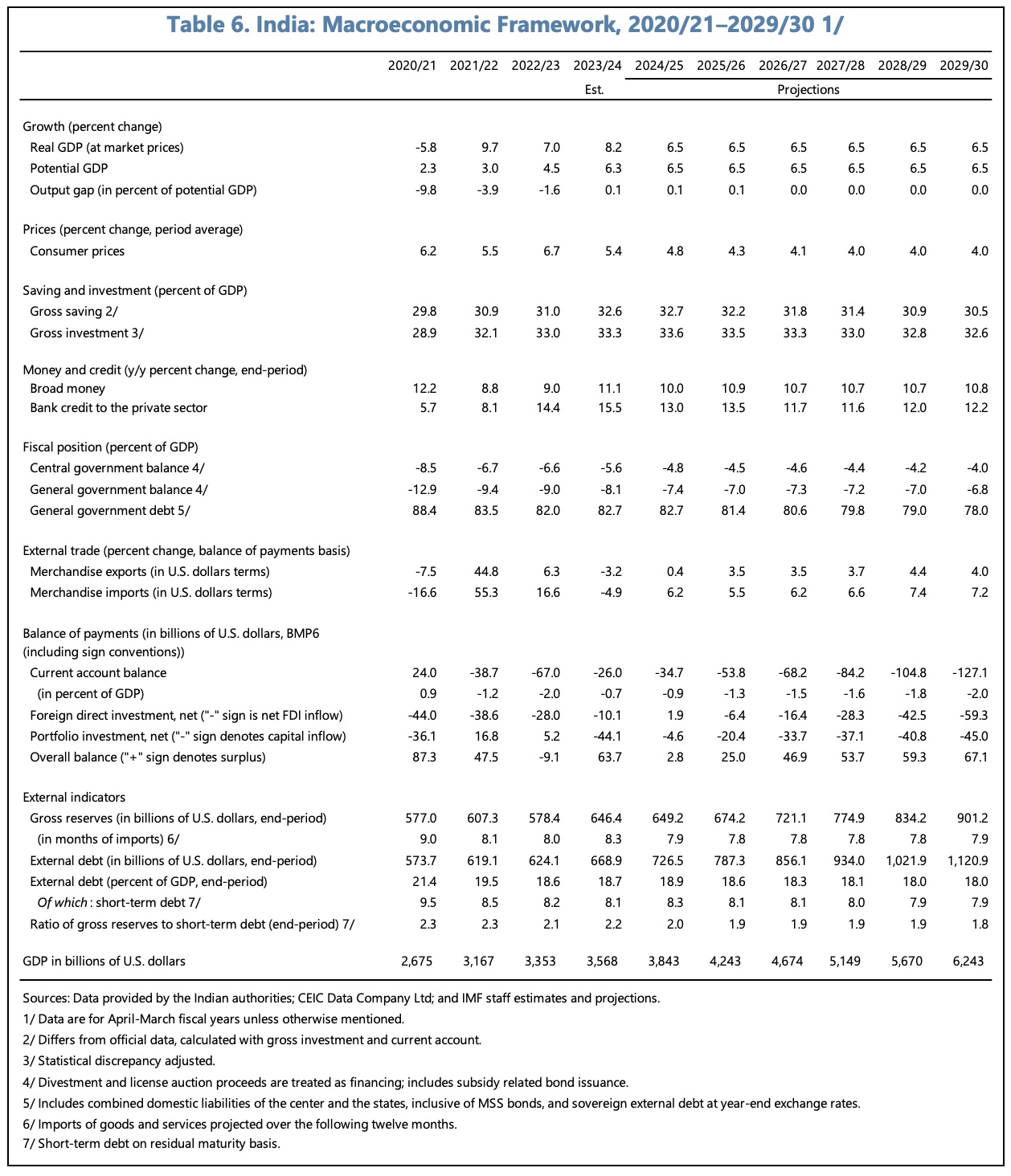

Growth has moderated somewhat to 6% YoY in H1 2024/25, with slower public capex ahead of the national elections. Private sector investment, notably investment in machinery and equipment has not matched expectations, although private consumption has increased with the more favourable monsoon.

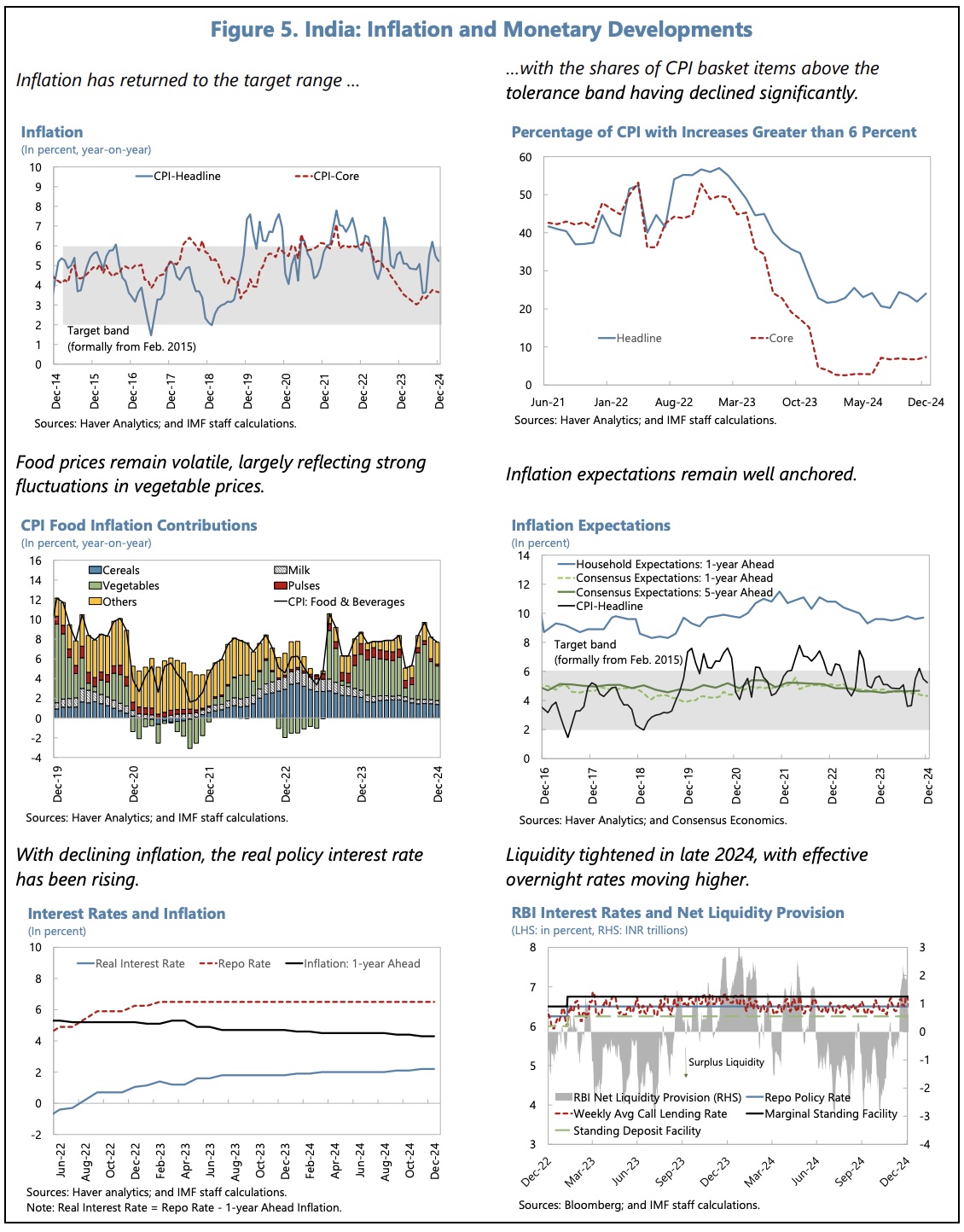

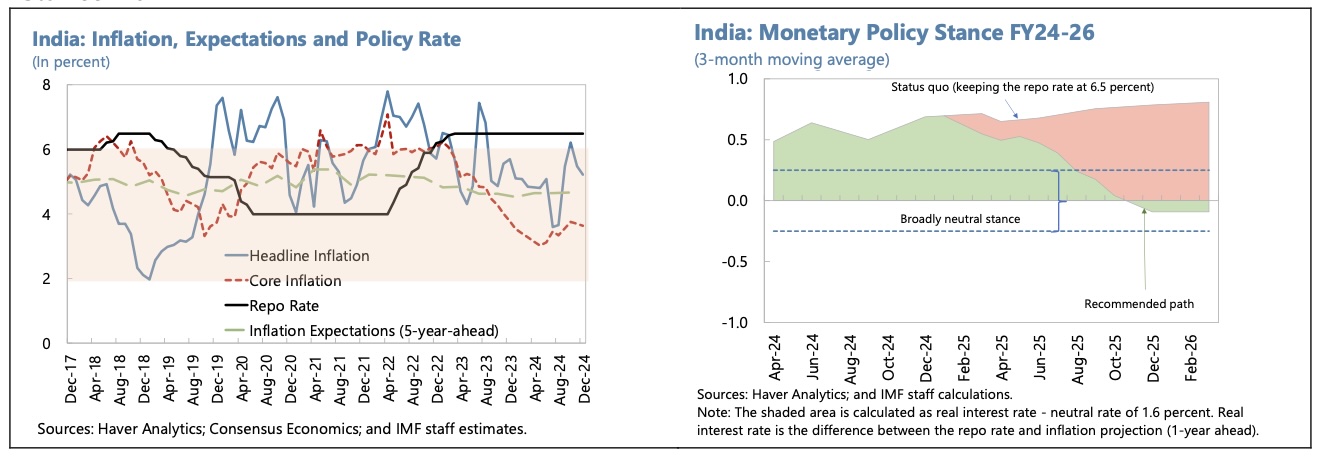

Although food prices have been volatile, headline inflation has moderated, and it is projected to settle at 4.8% in 2024/25 and 4.3% in 2025/26. As the output gap narrows and inflation eases further, there should be scope for a gradual easing in interest rates, although its pace will remain data dependent. With better inflation targeting, there is also scope for some greater exchange rate flexibility.

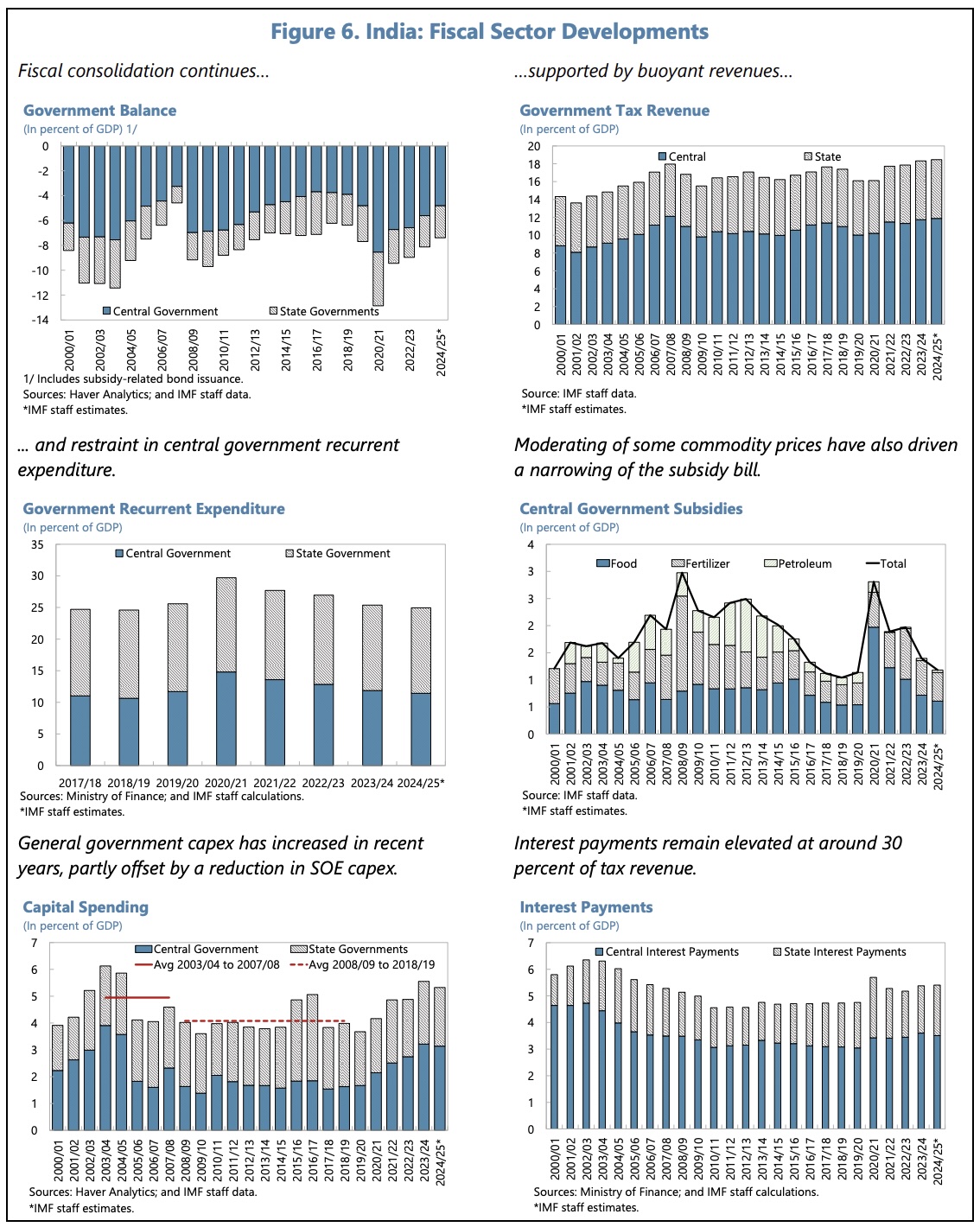

The fiscal balance has also been moving in the right direction, the general government balance declining from 9% GDP in 2022/23 to 8.1% GDP in 2023/24. Within this, revenue and capital spending have increased, whilst central government current expenditure has been restrained and subsidies have declined with lower commodity prices. In 2024/25, the general government deficit is expected to fall further to around 7.4% GDP, supported by high central bank dividends and buoyant personal income tax revenue. Grants-in-aid from the central government to the states have declined. A slow start to their capital spending in the current year suggests the states’ deficit may sustain at around 3% GDP.

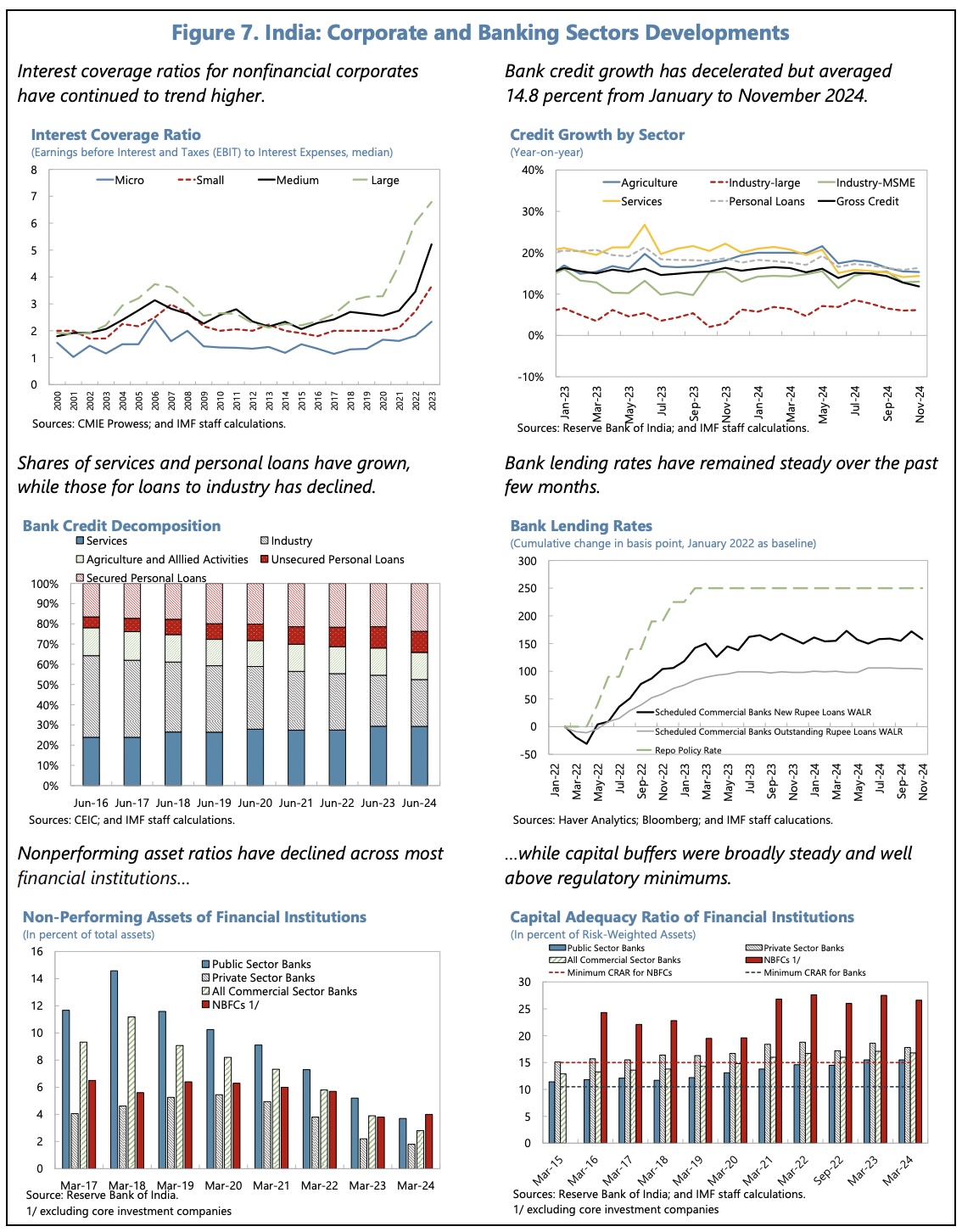

Systemic risks in the financial sector appear to be broadly contained, although there are some pockets of vulnerability that need addressing. Credit growth has decelerated somewhat, but it is expected to remain steady at 11% to 12% in the coming two years. Despite higher lending rates, corporates have been resilient and aggregate interest coverage has improved.

The 2025/26 budget included a substantial simplification and reduction in import tariffs, including on items such as electronics, life-saving medicines, textiles, cars and motorcycles. Restrictions on the export of certain agricultural products, which were introduced in 2022-23, have been relaxed. On the other hand, the import management system for IT hardware, and tariffs on imports of certain types of steel from China and Vietnam have been extended beyond their original expiry date.

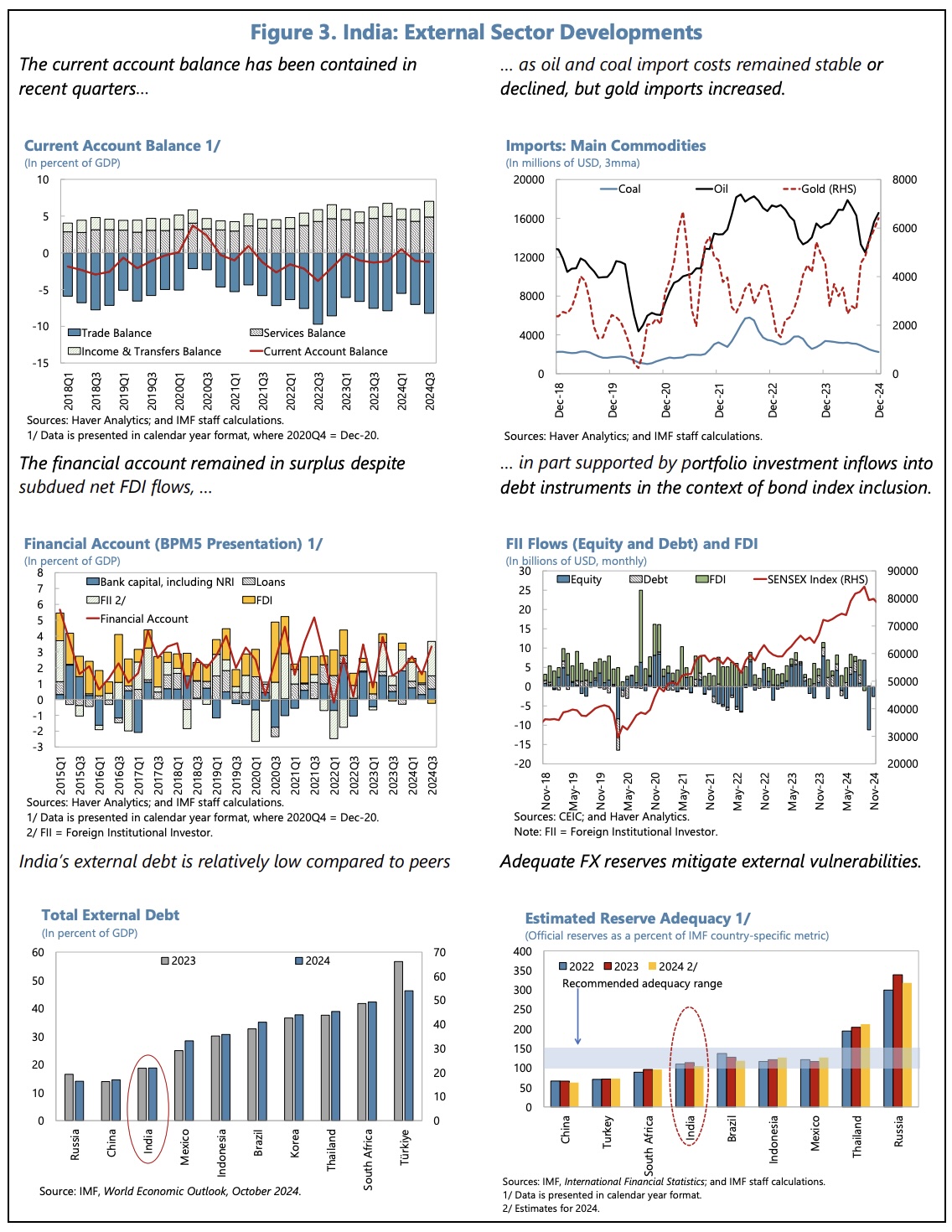

The current account deficit, projected at 0.9% GDP in 2024/25, is lower than its sustainable norm (2.2% GDP), but it is expected to rise gradually, as demand from India’s trading partners is likely to remain subdued, and domestic demand is expected to increase. The net FDI balance has been close to zero, as repatriations and outward investments have offset steady gross inflows. Official international reserves declined from a peak of $705bn in September 2025 to $640bn in December, but cover is deemed to be adequate, at around 8 months of imports.

Fiscal Policy

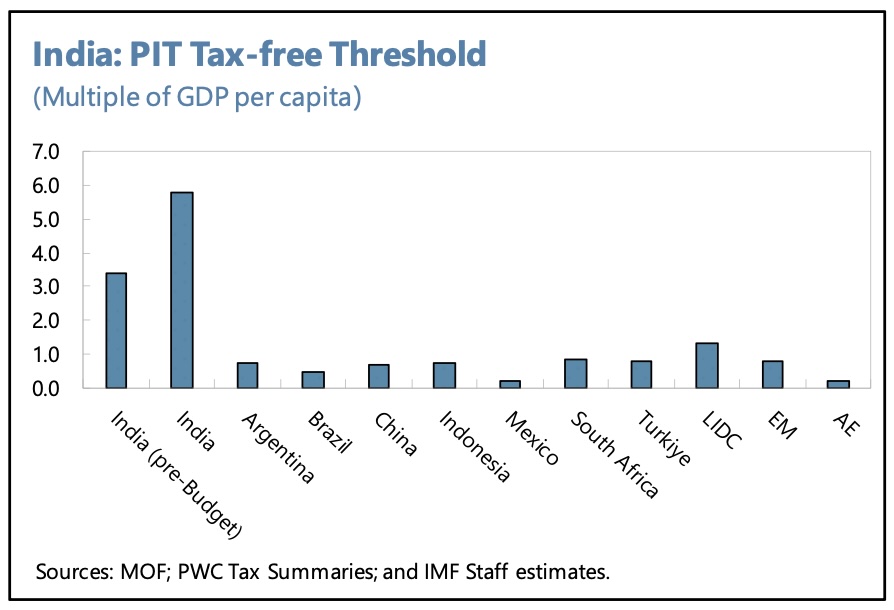

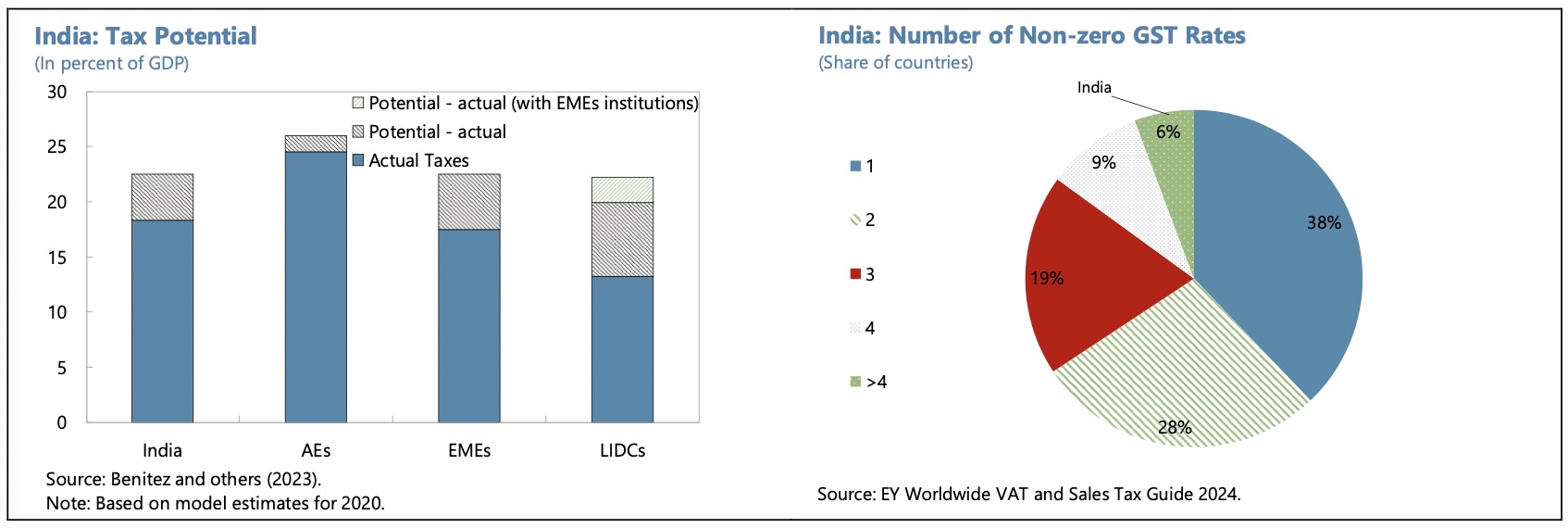

The IMF support a moderate contraction in the fiscal deficit, as the output gap has broadly closed and debt is elevated. They have cautioned against using high windfall gains from the central bank to finance permanently higher recurrent expenditure, and have encouraged the states to give greater weight to capital over recurrent spending. Although the increase in the personal income tax-free threshold announced in the budget has raised it significantly above peer country levels (from 3.5x to 6x per capita income), the IMF believe that improvements in tax administration and cuts in recurrent spending still hold out the prospect of a decline in the central government deficit to around 4.4% GDP in 2025/26. There is scope to raise revenue through GST simplification and reversing fuel excise cuts. Allowing domestic energy prices to reflect global prices would reduce support profitability in the power sector.

Under current policies, debt/GDP is expected to decline slightly to 77% GDP by 2030/31.

Fiscal risks include higher commodity prices/subsidies, contingent liabilities associated with loss-making SOEs (esp. the power sector), and unfunded civil service pensions. These can be countered with tighter subsidy targeting, regular revision of power tariffs and improved efficiency at the power distribution companies, and the better funding of pension fund benefits through improved actuarial assessment.

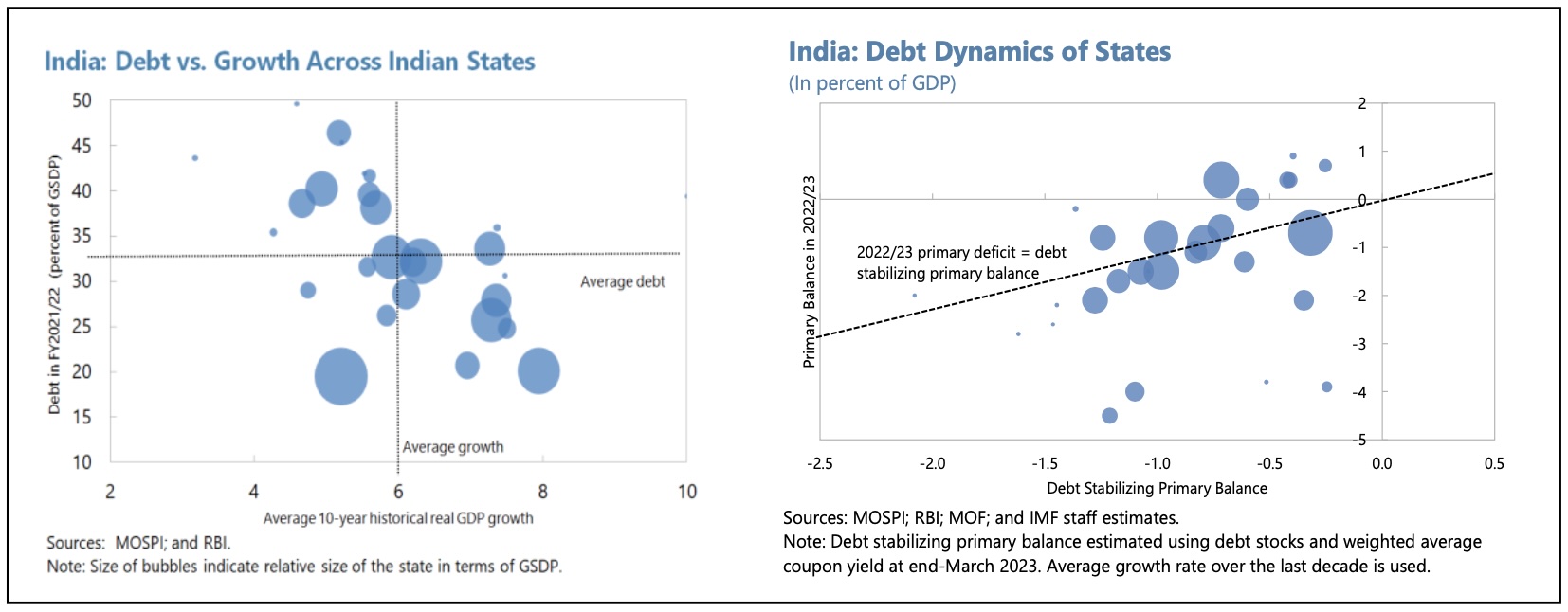

Risks of sovereign stress are seen as moderate, partly because a relatively high share of debt is denominated in rupees, with long duration, and the interest-growth differential is expected to remain favourable. (External debt was 18.7% GDP at the end of 2023/24.) Vulnerabilities are higher at the state level.

Monetary Policy

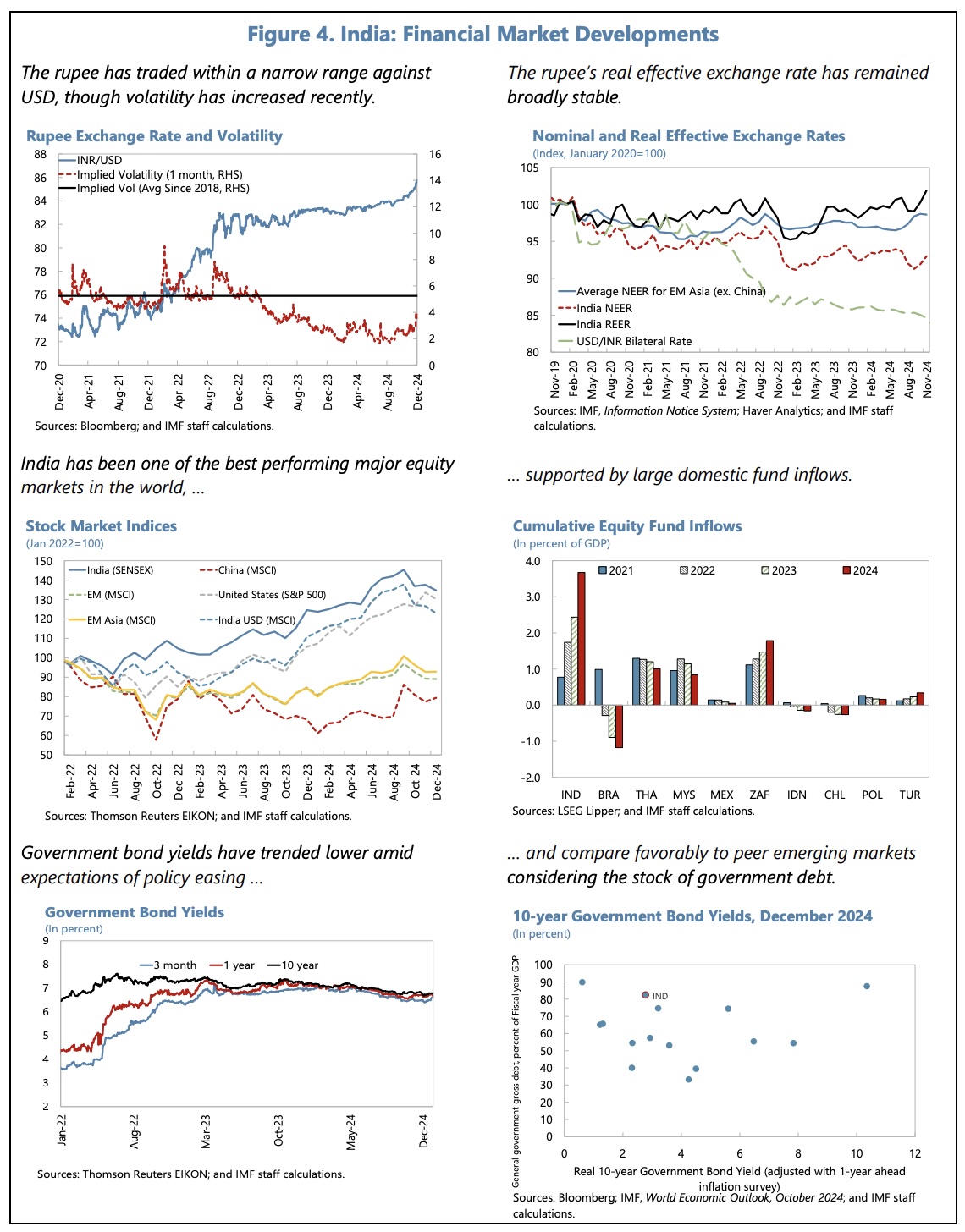

India’s flexible inflation targeting framework has been effective at anchoring inflation expectations. In the circumstances, the IMF think that greater exchange rate flexibility is warranted to help absorb external shocks, with intervention being used only to address disorderly market conditions. The advantages of using this approach would be a reduction in the need to hold costly precautionary FX reserves, the support it would give to the development of the FX market, and a reduction in the fluctuations of domestic financial system liquidity.

Financial Sector Policy

Sector risks are broadly contained, with banks’ gross NPLs at a multiyear low of 2.6% (September 2024), and capital buffers generally adequate. They are weaker at some public sector banks, select NBFCs and urban cooperative banks.

Household debt, at 43% GDP, remains manageable overall, and unsecured personal credit growth by banks has slowed from 24.5% in 2022-23 to 12.6% by November 2024. (NBFC unsecured lending growth has been higher, at over 30% in the period to September.).

Financial sector oversight has improved considerably. However, Non Banking Financial Institutions’s assets have risen from 34% of the total in 20i7 to 43%. The growing interconnectedness between financial institutions (bank funding accounted for 40% of NBFC borrowing in 2023/24) and mutual funds, suggests there is a need to strengthen data collection further, so that any emerging vulnerabilities are promptly identified.

Structural Reforms

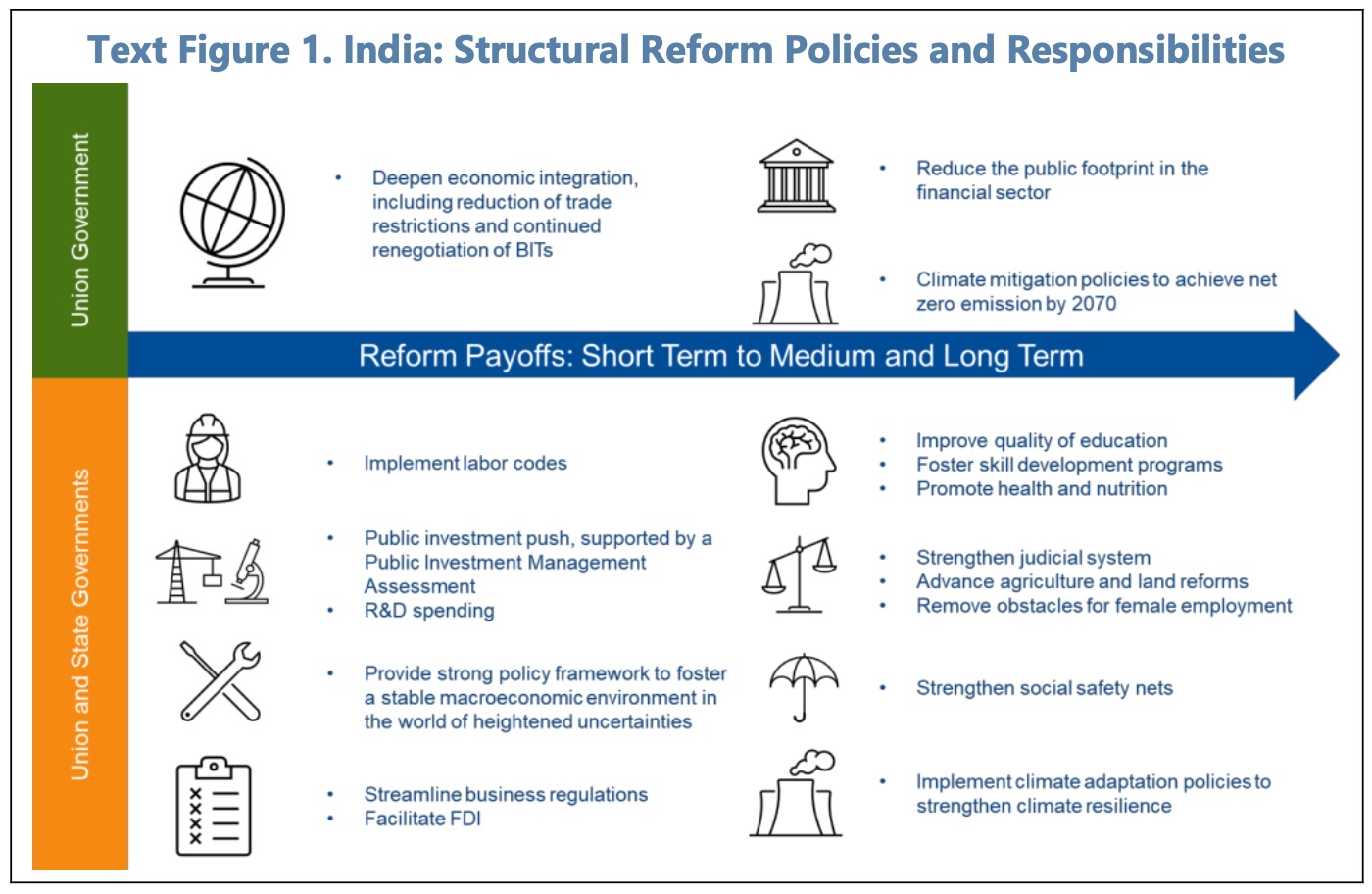

Labour market: The IMF believes job creation would be supported by the implementation of new labour market codes designed to enhance market flexibility and ease the constraints keeping firms inefficiently small. Suggestions include relaxing the hiring and firing regulations, more flexible and targeted social safety nets designed to facilitate the migration of workers from rural to urban areas and between states, and measures to encourage female employment.

There is a need to improve the quality of education and skills development, and health and nutrition.

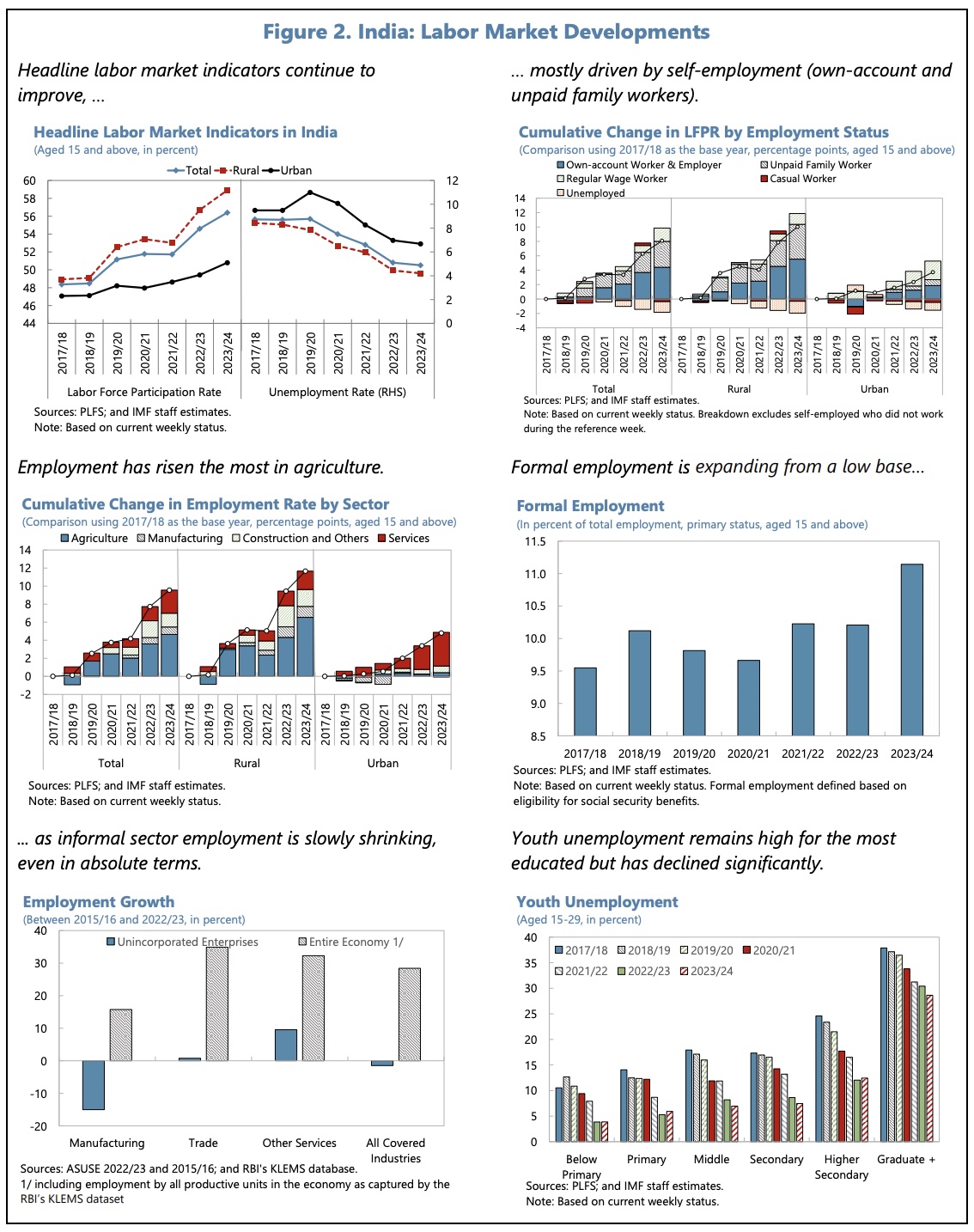

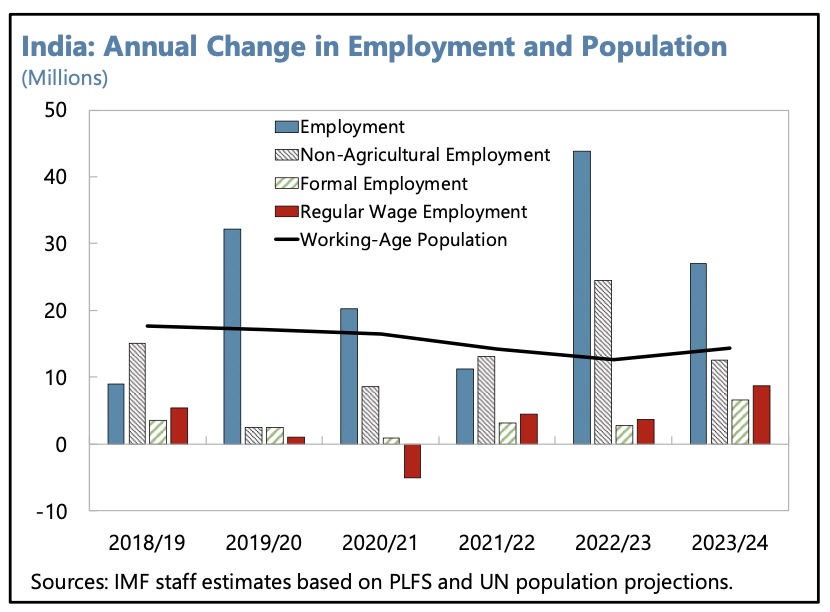

The IMF note that, whilst the labour force participation rate has been increasing (from 48.4% in 2017/18 to 56.4% in 2023/24), much of the increase has been driven by own-account and unpaid family workers and that, since the pandemic, there has been an increase in agricultural employment, which fits ill with traditional development paths.

Efforts are needed to improve the ease of doing business: (i) improving stability in taxation policy and regulation, (ii) reforming the insolvency and bankruptcy codes, (iii) reducing the public sector footprint in the credit markets, (iv) reducing bureaucracy, (v) tackling corruption. Success in these areas should encourage private sector investment and FDI, which is yet to take off as expected.

Reducing external trade restrictions and fostering bilateral, regional, and multilateral trade will strengthen India’s integration into global value chains, thereby attracting FDI, promoting technological transfer and boosting productivity. Whilst the IMF acknowledge that negotiations are underway with the UK and EU, they suggest India should consider participating in the Regional Comprehensive Economic Partnership (RCEP) between ASEAN and China, Japan, Korea, Australia and New Zealand.

To conclude, they caution that, whilst the government’s Product Linked Incentives (PLIs) targeting 14 selected industries have been successful within their limits, they cannot substitute for the above-mentioned horizontal reforms. Not only is spending equivalent to just 0.1% GDP between 2022/23 and 2024/25, but also the number of people entering the labour market each year is too great. In addition, the fiscal cost per job of the PLIs is too high.