In July 2025, the IMF completed their fourth review of the Sri Lankan economy under the $3bn Extended Fund Facility programme, launched in March 2023. Sri Lanka has been granted immediate access to $350mn in Special Drawing Rights under that programme.

The IMF have reported that ‘performance under the programme has been generally strong.’ All quantitative targets for end-March 2025 were met, except the indicative target on the stock of expenditure arrears, which is being addressed. All structural benchmarks due by the end of May were either met or implemented with delay. Q2 2025 inflation fell below the outer band of the Monetary Policy Consultation Clause, largely due to energy prices. Debt restructuring is nearly complete.

Sri Lanka’s government. which holds a two-thirds majority in parliament, has confirmed that ‘it is now looking to pursue a more ambitious agenda of policies, in line with the IMF program objectives.’ Future reforms include measures to reduce corruption and upgrade governance standards, to boost investment through changes to tax exemptions, and to retool and improve fiscal revenue administration. Plans also include measures to help the vulnerable.

The IMF caution that global trade uncertainty poses a significant risk to Sri Lanka’s economic stability, as the USA accounts for 23% of goods exports (equivalent to 3% GDP). Negotiations are continuing: the IMF’s estimates assume continuing baseline tariffs of 10%. With this caveat, however, the IMF report that Sri Lanka’s reform efforts are bearing fruit, and that there is ‘significant progress on all fronts.’

Recent Developments

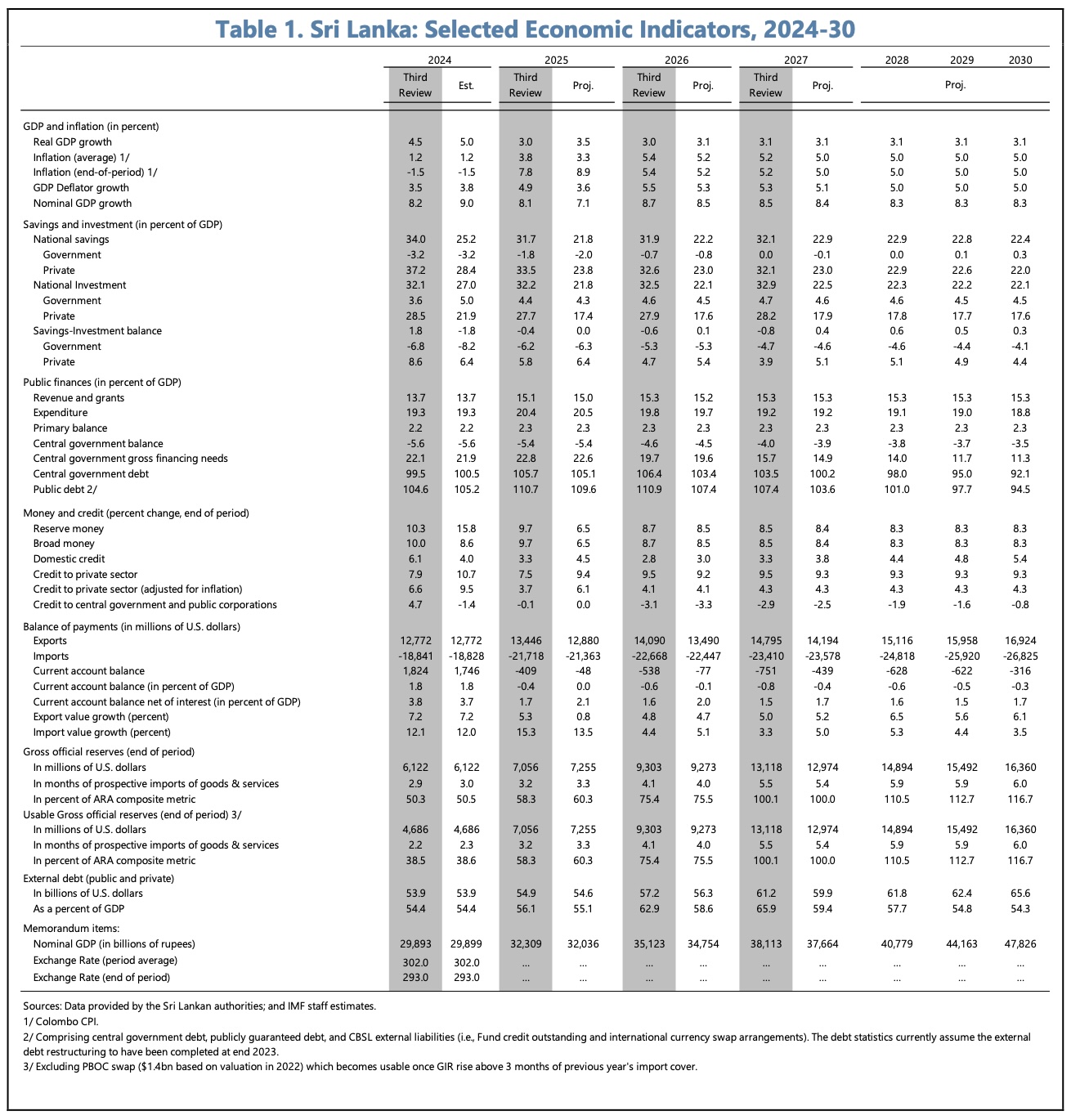

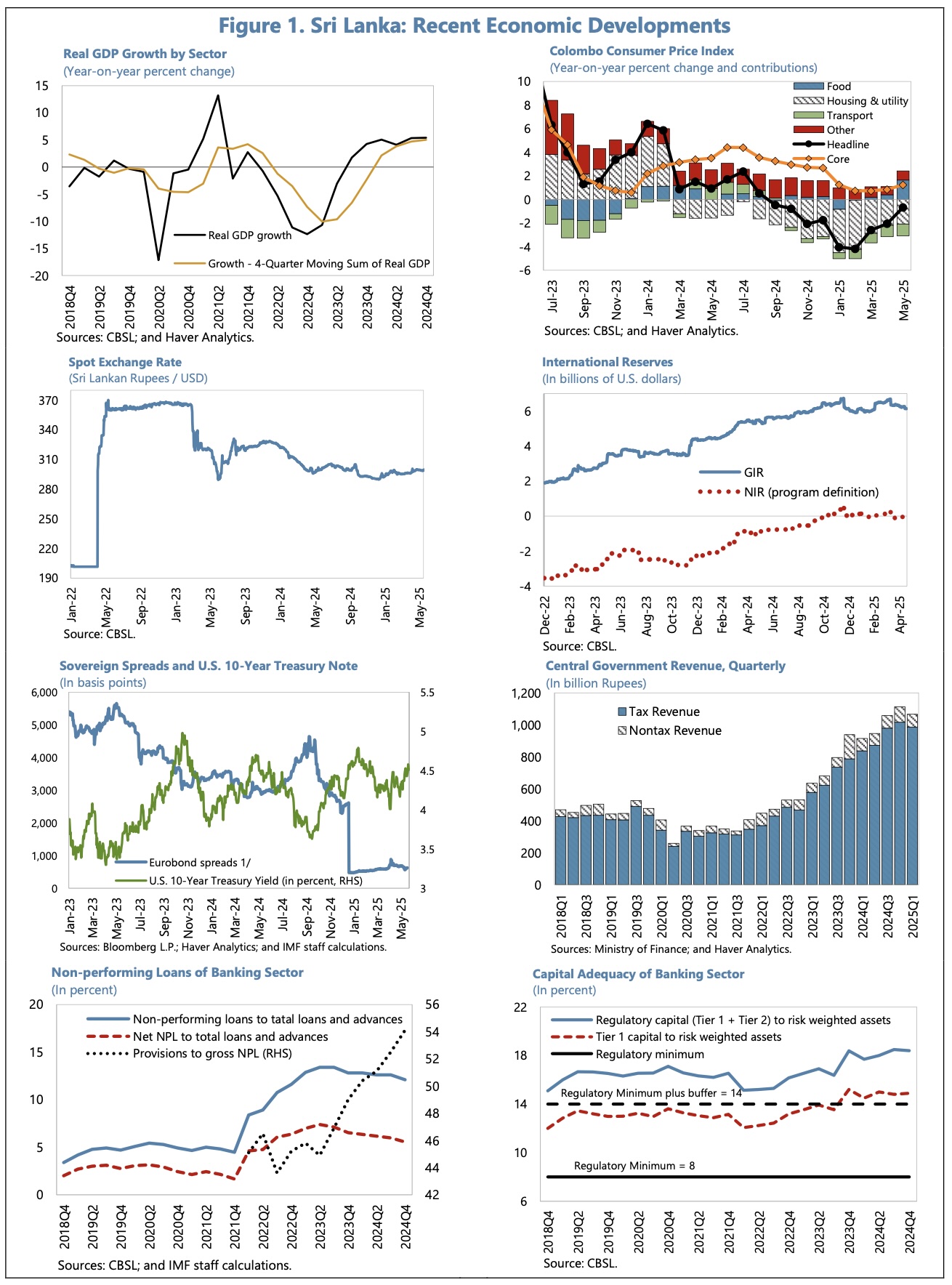

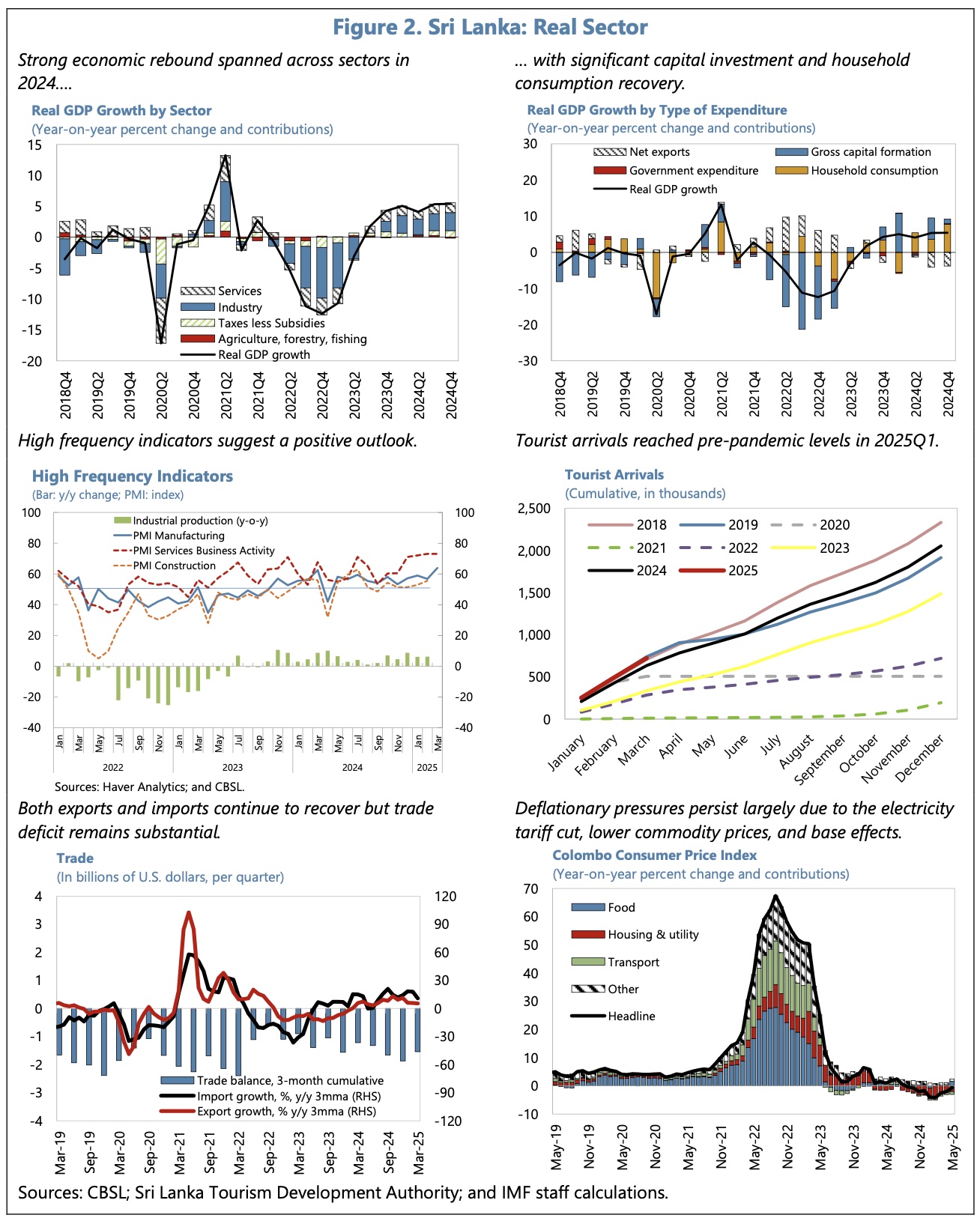

Real GDP rose by 5% YoY in 2024, led by manufacturing, construction and tourism. With the PMIs for manufacturing and services firmly positive, there are signs that this will continue.

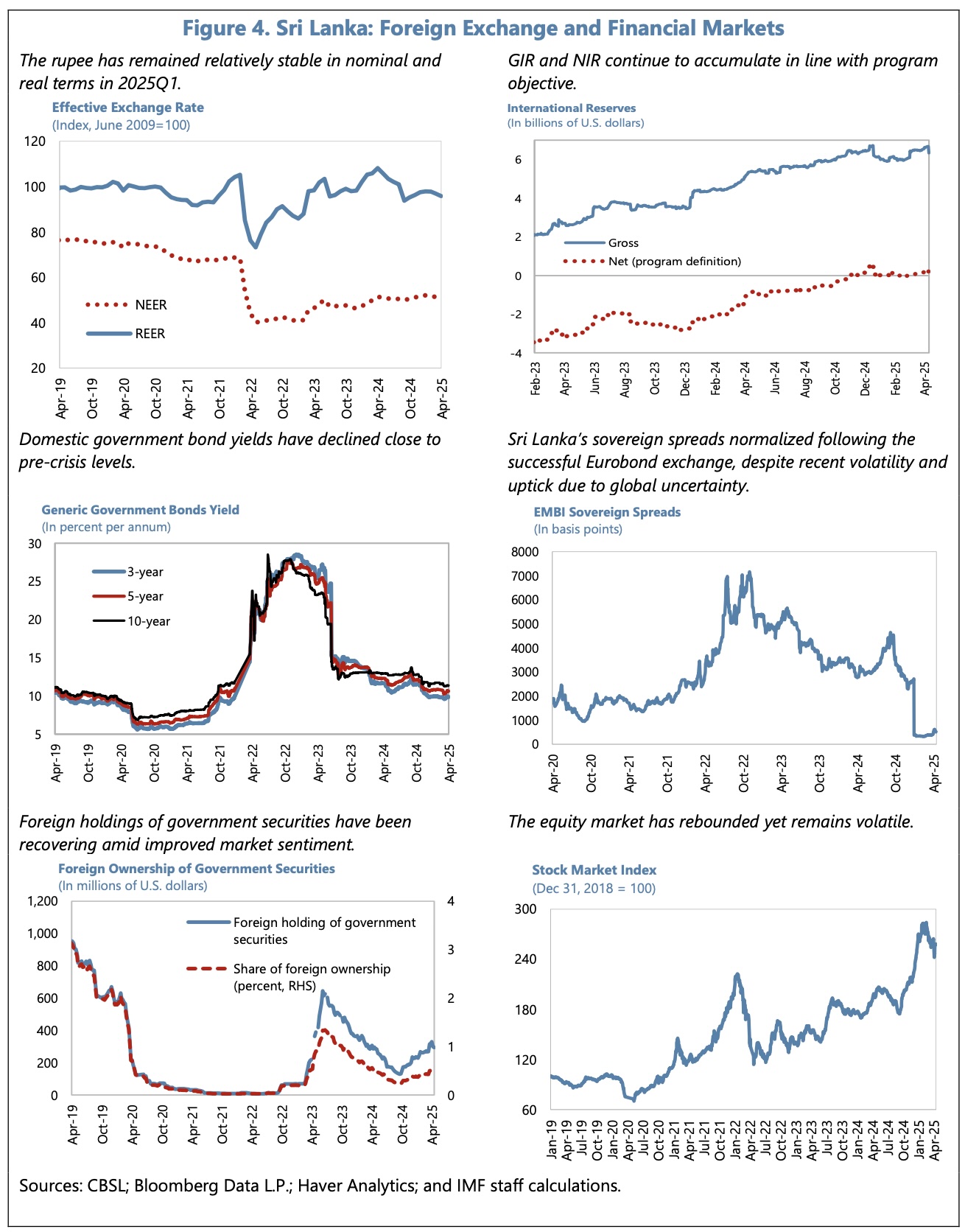

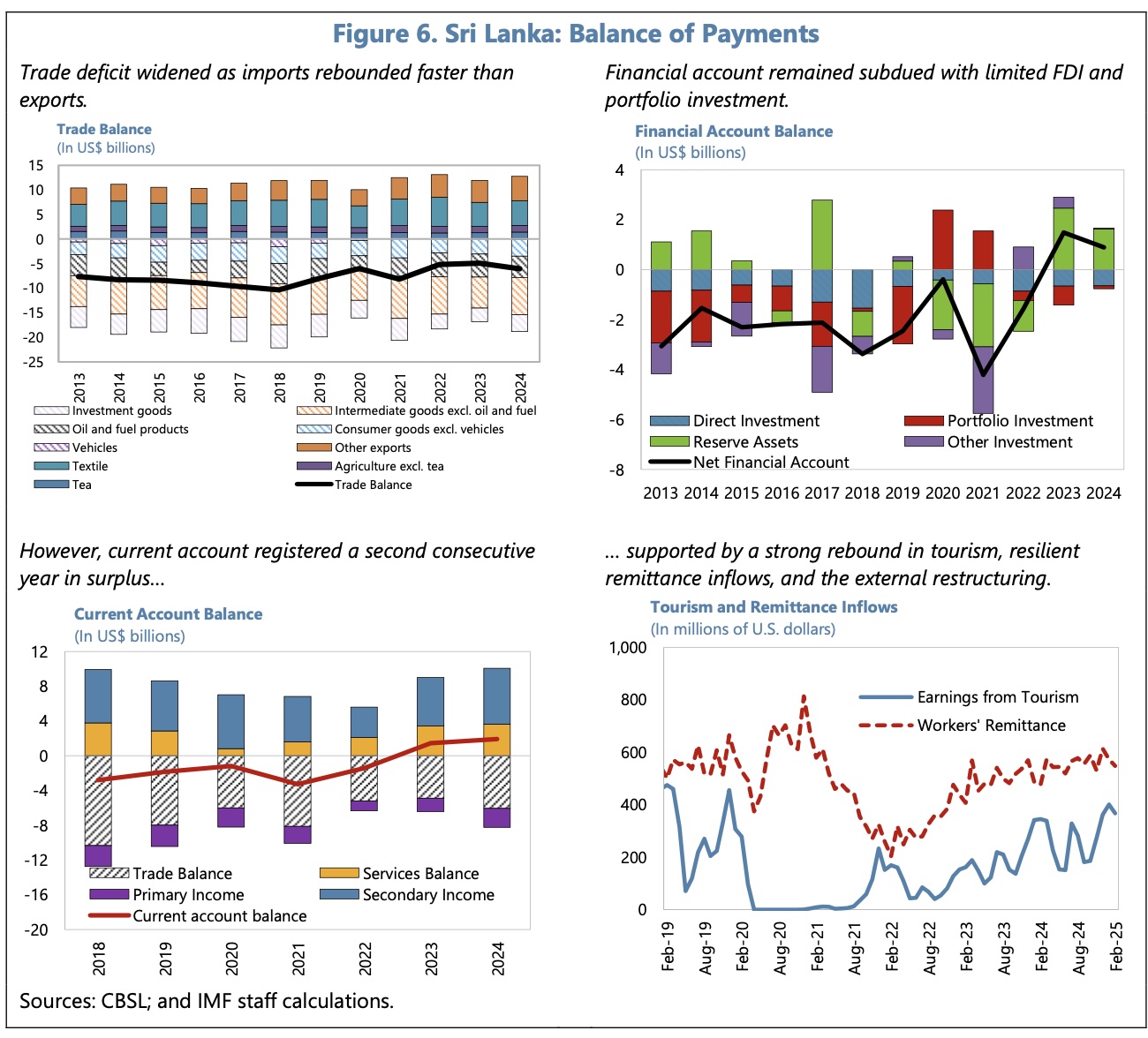

Inflation remains subdued (May headline CPI -0.7% YoY, core CPI +1.2% YoY). Reserve accumulation has outperformed, with the current account in surplus as a result of buoyant tourism and strong remittances. Gross official reserves reached $62.2mn (52% of target) at the end of April. The real effective exchange rate depreciated by 4.6% YoY, as of April.

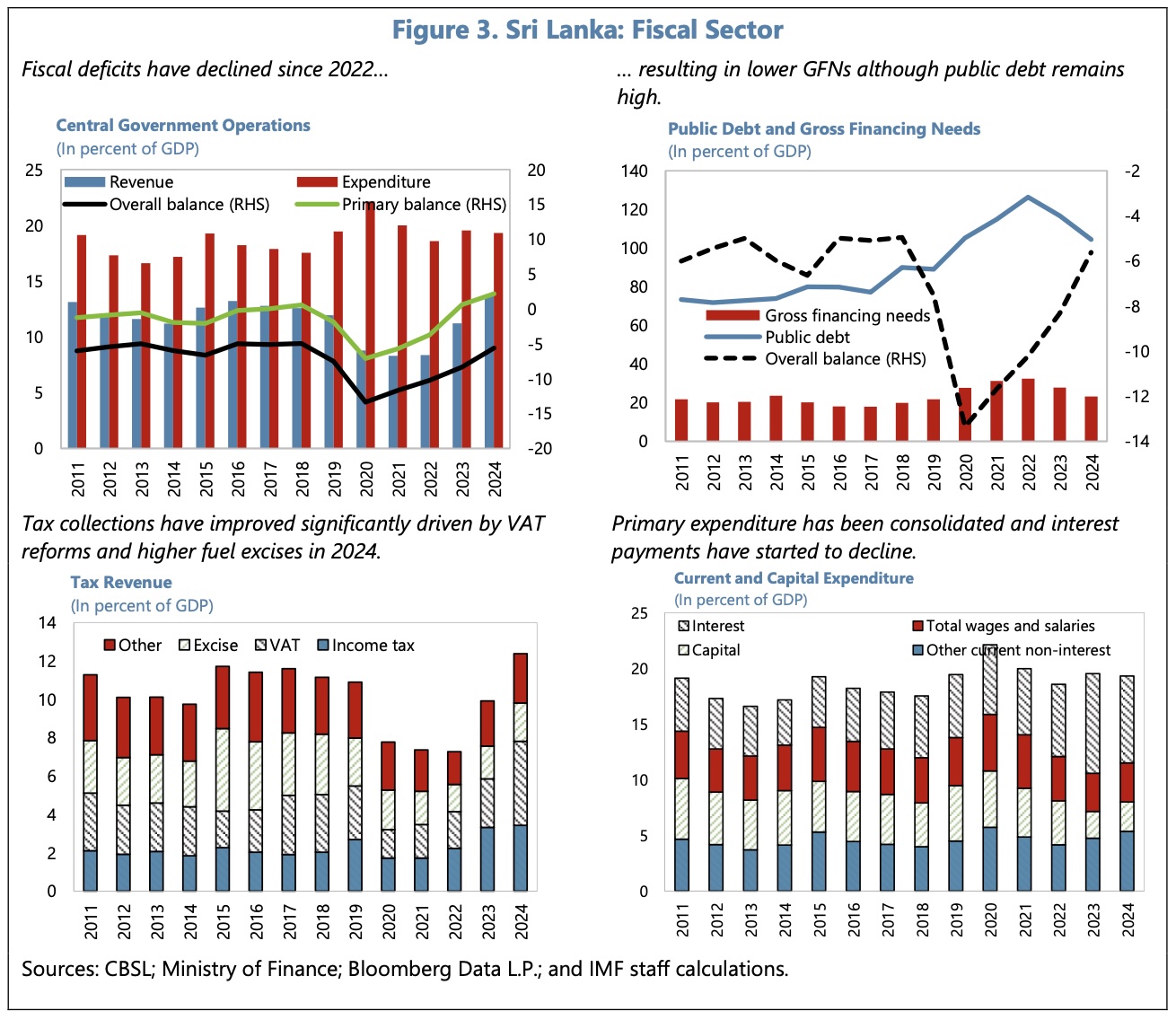

Revenue-based fiscal consolidation is on track, with tax revenues rising by 21% YoY in January-April. The primary balance recorded a surplus of 1.6% GDP, reflecting limited provision for government capex under the plan.

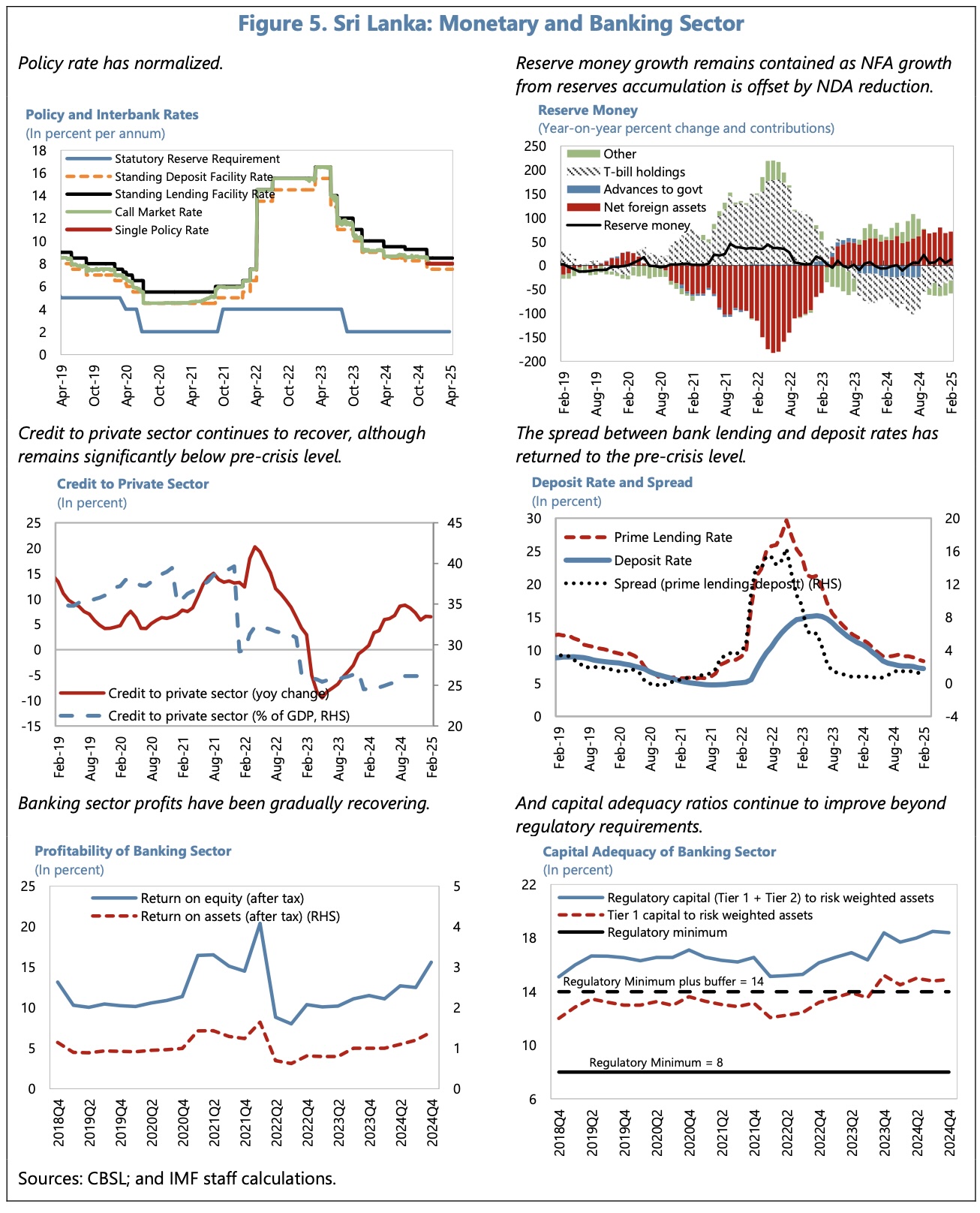

Credit to the private sector has been accelerating (+12.8% YoY in February). The banking sector is well-capitalised, with aggregate regulatory capital standing above 18% in the last three quarters of 2024. The net level of NPLs, though high, has nevertheless declined from 7.4% in Q2 2024 to 5.6% in Q4.

Outlook and Risks

Real GDP growth is now forecast to rise by 3.5% YoY in 2025 (up from an earlier forecast of 3%). This reflects stronger tourism, buoyant manufacturing and construction, and recovering consumption.

Lower energy prices and a stronger than expected exchange rate have contributed to a reduction in the average inflation forecast, to 3.3% YoY. The current account is projected to deteriorate only marginally, and is forecast to be close to balance in 2025.

In terms of risk, a return to the 44% reciprocal tariff announced by President Trump in April 2025 would be a significant shock to Sri Lanka’s competitiveness. The IMF think exports could decline by as much as 3% of GDP. They caution that margins, especially in the garment sector, are thin, and that exporters might relocate their existing foreign operations. Allowing for a need for fewer export-related inputs, lower commodity prices and FX depreciation, they estimate the hit to real GDP might be between 1/4% and 1 1/2% relative to the baseline. The impact on unemployment is potentially very significant, as the garment and rubber industries employ over 1 million, directly and indirectly. Clearly, such a shock would also pose significant risks to the recovery programme.

The following table and charts summarise some of the IMF’s key perspectives on the performance of Sri Lanka’s economy. Full details are contained in the IMF’s report, which may be read using the following link to the IMF’s website: IMF Report