In its latest survey, titled ‘Surviving not Thriving’, the World Bank reports that Myanmar’s economy is continuing to feel the effects of the March 2025 earthquake, persistent conflict, subdued domestic demand, labour shortages and power outages.

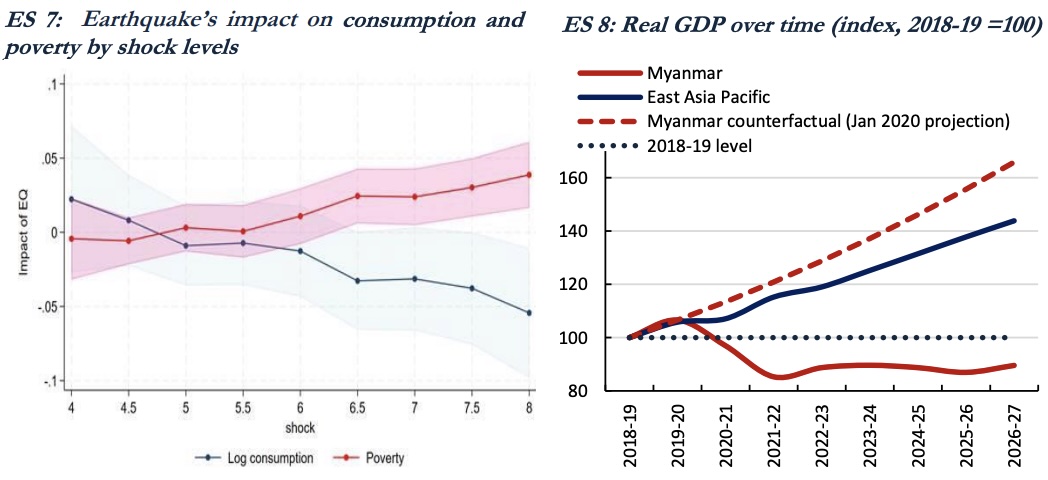

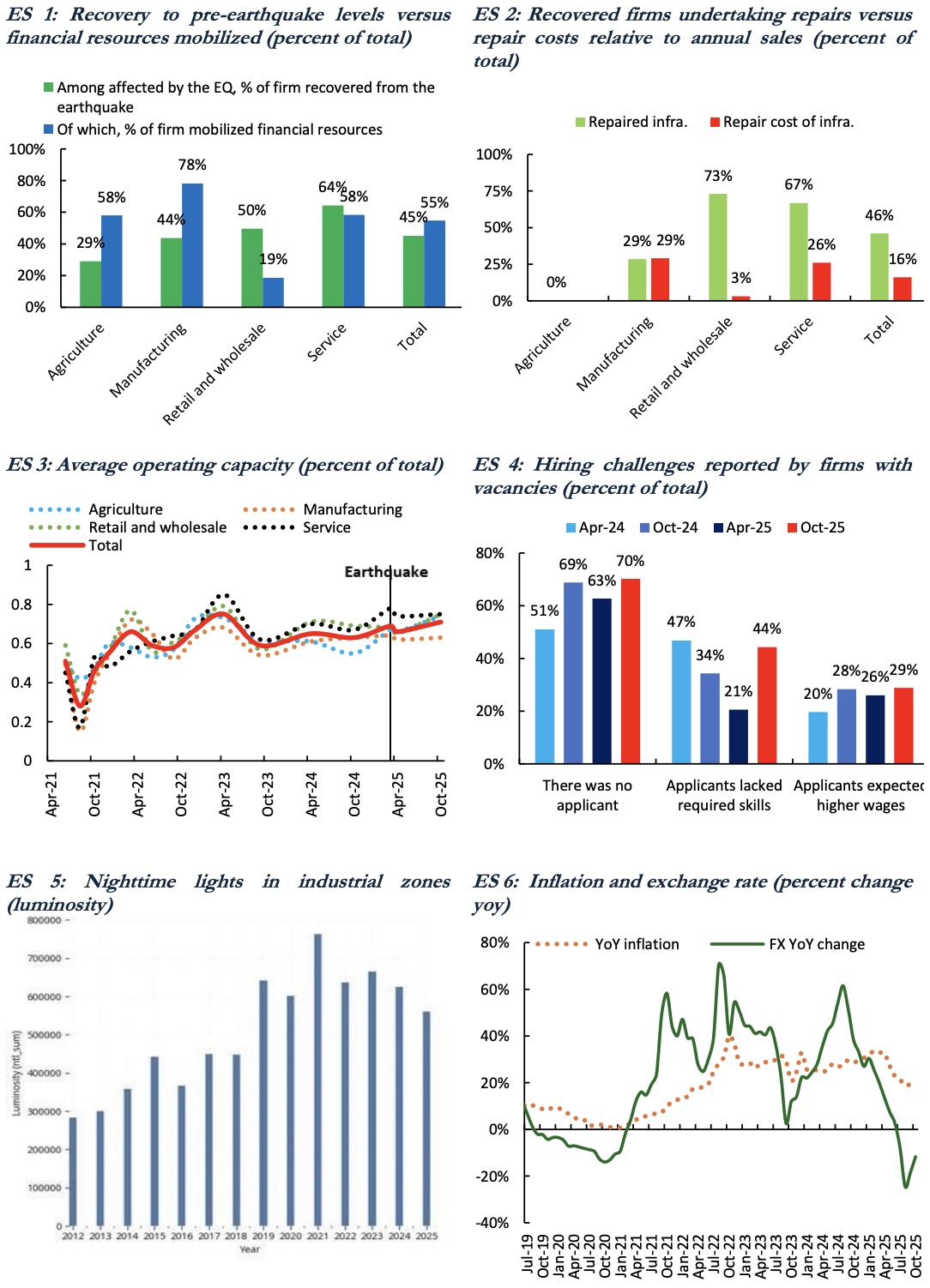

Only 45% of the firms they have surveyed are enjoying pre-earthquake levels of activity, with capital-intensive firms suffering more than most. Household vulnerability and poverty have worsened, especially in areas most affected by the earthquake (Mandalay, Sagaing, Naypyitaw), whilst 3.6 million people have now been displaced by conflict.

In business, power shortages present a critical bottleneck, with night-time light data from industrial zones indicating a broad-based decline in real activity. The labour market has experienced further deterioration, with the earthquake, conflict and conscription all contributing to outward migration and mismatches between the demand for skills and supply. Average firm operating capacity has risen, but only to 71%, a level well below pre-earthquake levels. Agricultural output has shown some resilience, manufacturing less so. In aggregate, the economy is expected to be 13% smaller than it was before the pandemic.

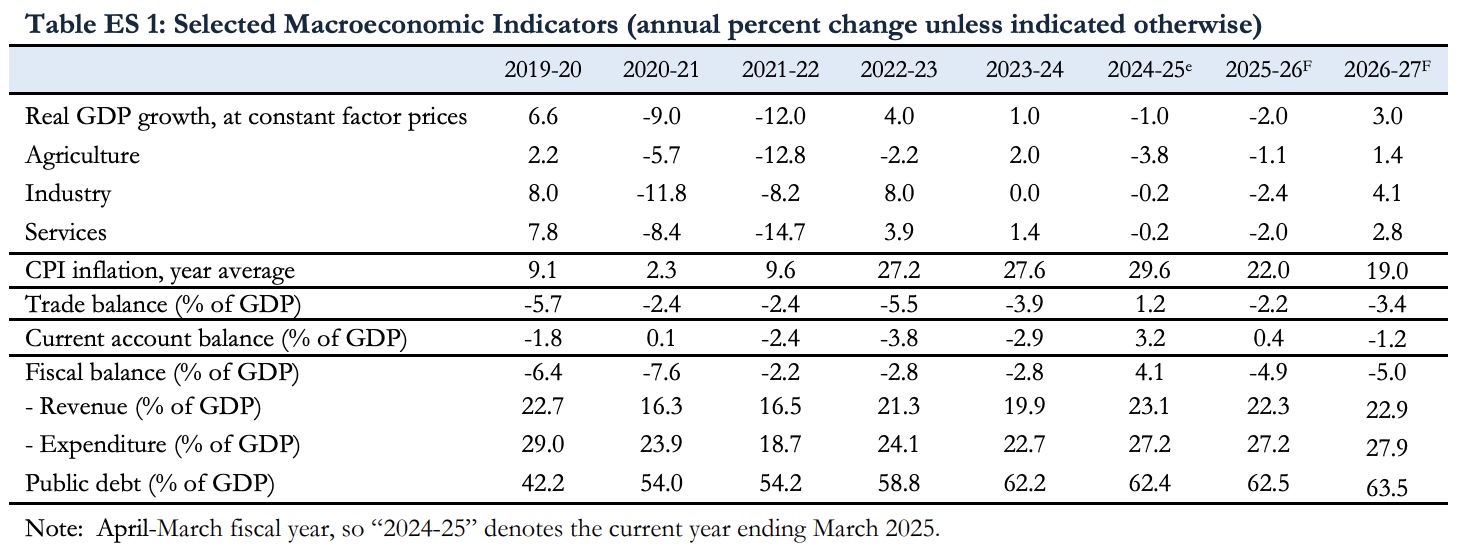

Meanwhile, the level of inflation remains high (19.8% YoY, headline in October) and unanchored. To this, import restrictions, energy tariffs, supply-side constraints, and robust monetary expansion, fuelled by central bank funding of the fiscal deficit, are all contributing. Looking forward, the fiscal deficit is expected to widen, raising concerns about the inflation risks and macroeconomic stability.

Despite these negatives, confidence in the banks has improved, with deposits and credit both growing steadily, and liquidity remaining strong. NPL ratios have declined for a sample of banks representing 15% of system assets, as a result of restructuring efforts and improved collateral values. However, the World Bank has cautioned that a comprehensive assessment of system assets is not available, and that the number of microfinance clients fell by 27% to 2.8 million in FY 2024/2025.

The external sector has been supported by robust trade performance, assisted by garment exports, and inward remittances, though the surplus has narrowed in H1 FY 2025/26, as imports have risen with reconstruction.

Overall, real GDP is expected to decline by 2% YoY in FY 2025/26, and to recover by 3% YoY in FY 2026/27, as earthquake reconstruction and increased investment in public infrastructure take hold. On the other hand, inflation and the fiscal deficit are projected to remain high, even as the current account surplus narrows.

A summary table of forecasts appears below, together with a few charts taken from the introduction to the World Bank’s report.

For further details, including a detailed survey of Myanmar’s agrifood industry, please refer to the full report using this link to the World Bank’s website: