The IMF have published their latest report on the Indian economy under the annual Article IV consultation process.

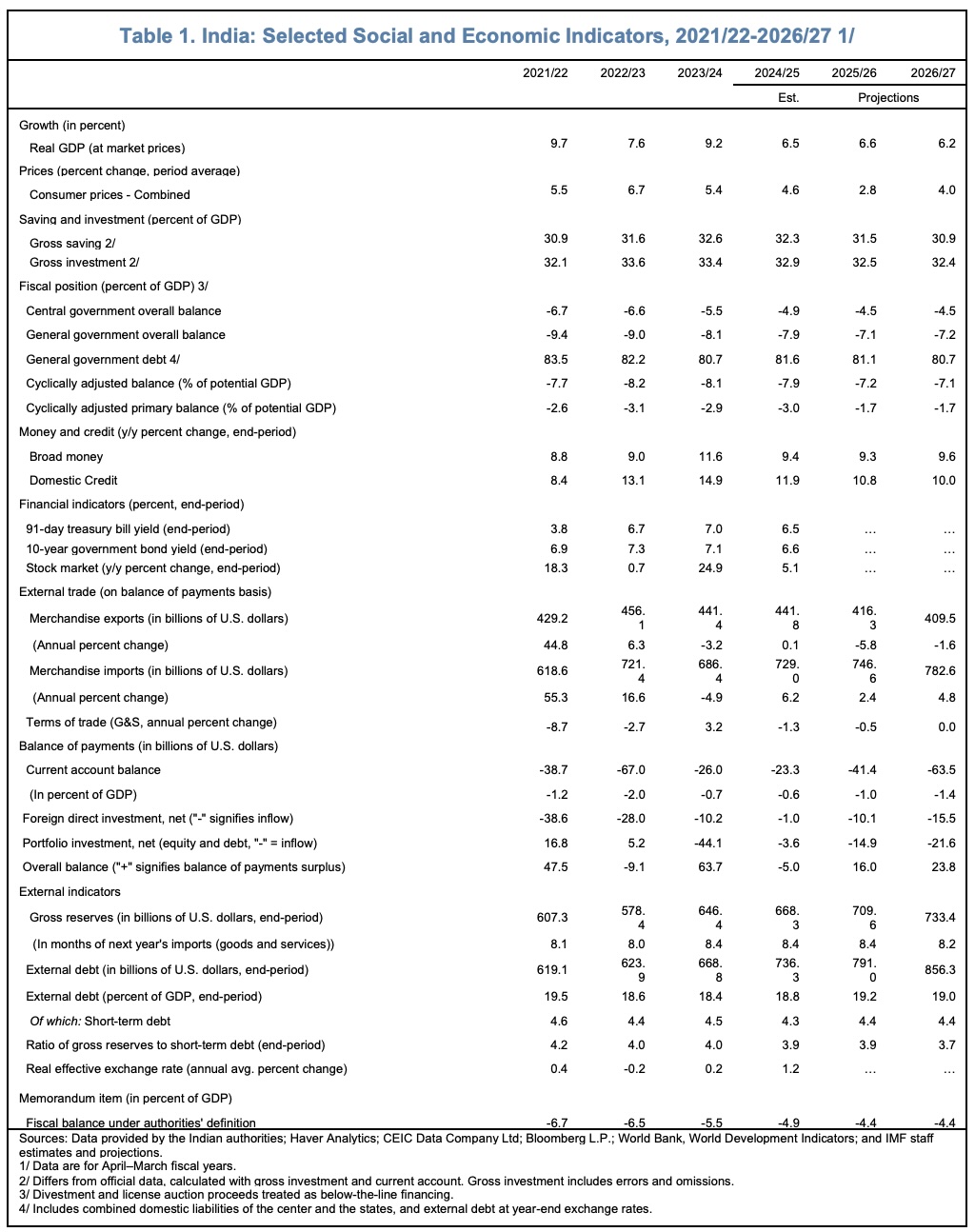

As expected, their verdict is generally favourable. Despite external headwinds from international trade tariffs, growth is expected to remain resilient (6.6% real GDP growth in 2025/26, 6.2% in 2026/27), whilst inflation is forecast to remain controlled (2.8% in 2025/26, 4% in 2026/27%).

India is reaping the rewards from past reforms in the areas of Goods and Services Tax (GST), flexible inflation targeting, and the expansion of digital public infrastructure. In addition, it has the advantage of being less exposed to international trade than other emerging Asian economies. Although merchandise exports to the US have been subject to c.50% tariffs since August 2025, around 30% of these have been exempted. Together, US merchandise exports represent just 2.2% GDP.

Recent Developments

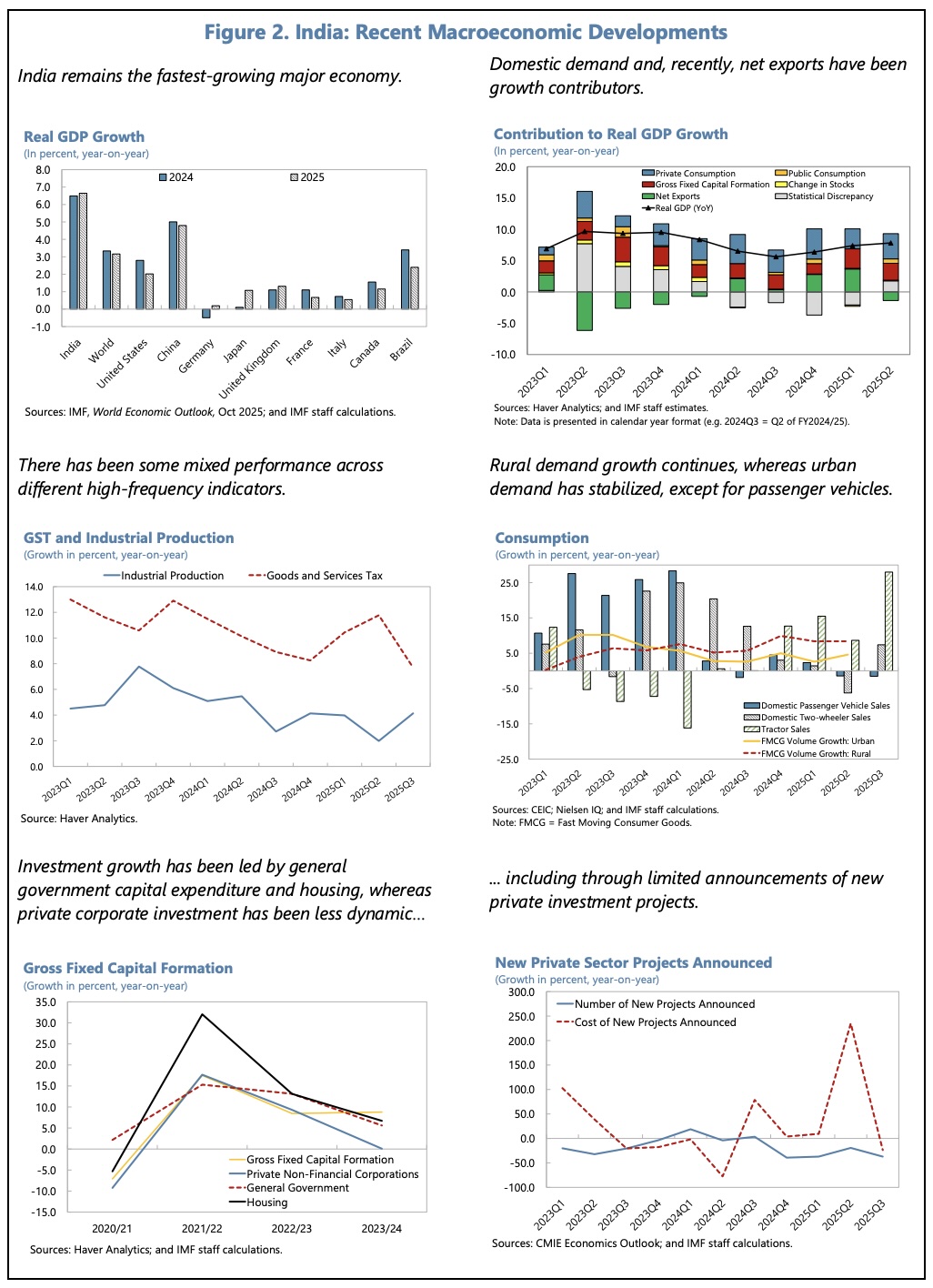

Real GDP grew by 6.5% YoY in 2024/25. Within this, private consumption (+7.2% YoY) and public investment have been resilient, whilst private investment has been somewhat less dynamic. Real GDP grew by 7.8% YoY in Q2 2025/26. In the IMF’s view, the output gap broadly closed in 2024/25.

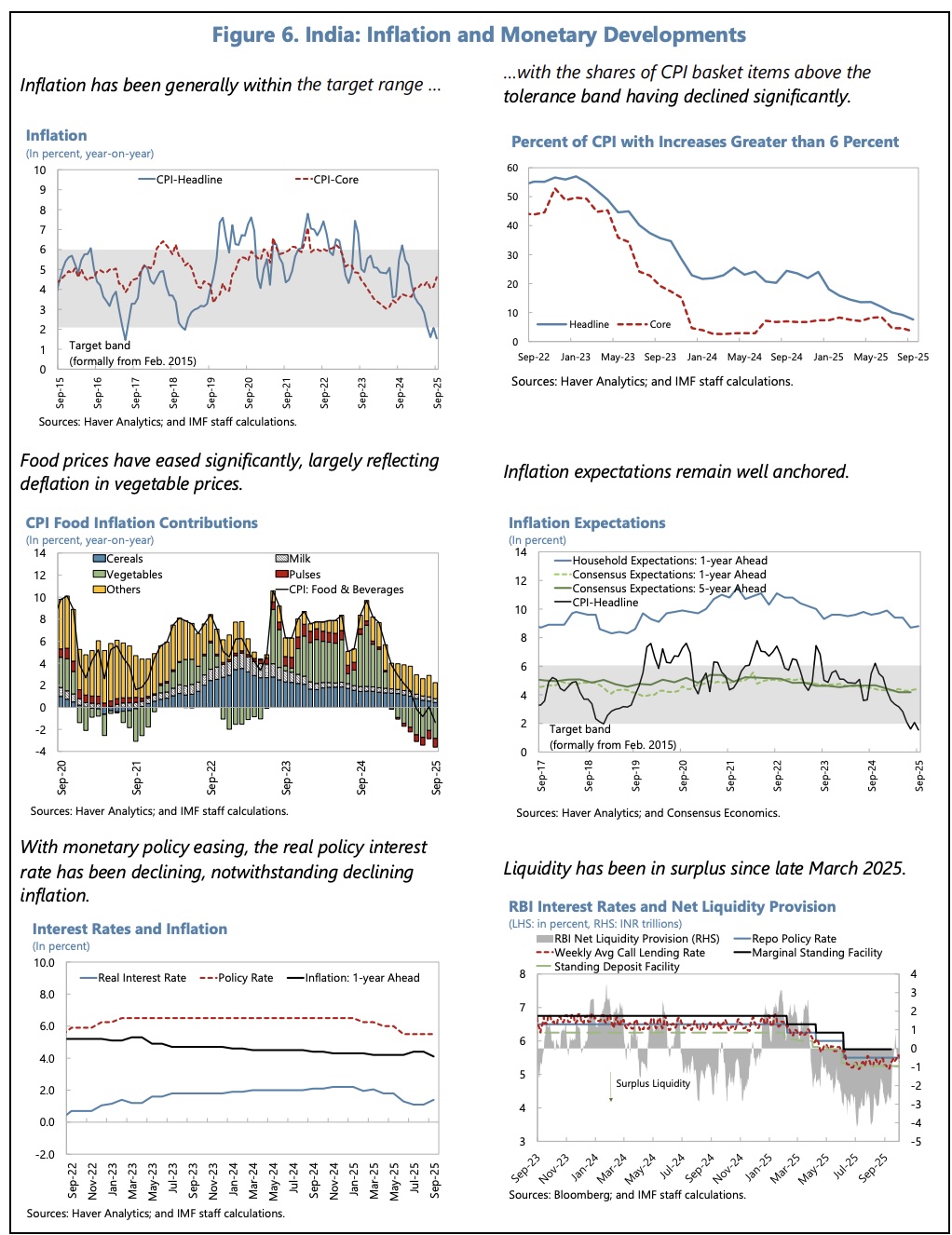

Headline inflation has fallen from an average of 4.5% in 2024/25 to 1.5% YoY in September 2025. A good harvest has helped domestic food prices. On the other hand, higher gold and silver prices meant that core inflation rose from a 2024/25 average of 3.5% YoY to 4.6% YoY in September.

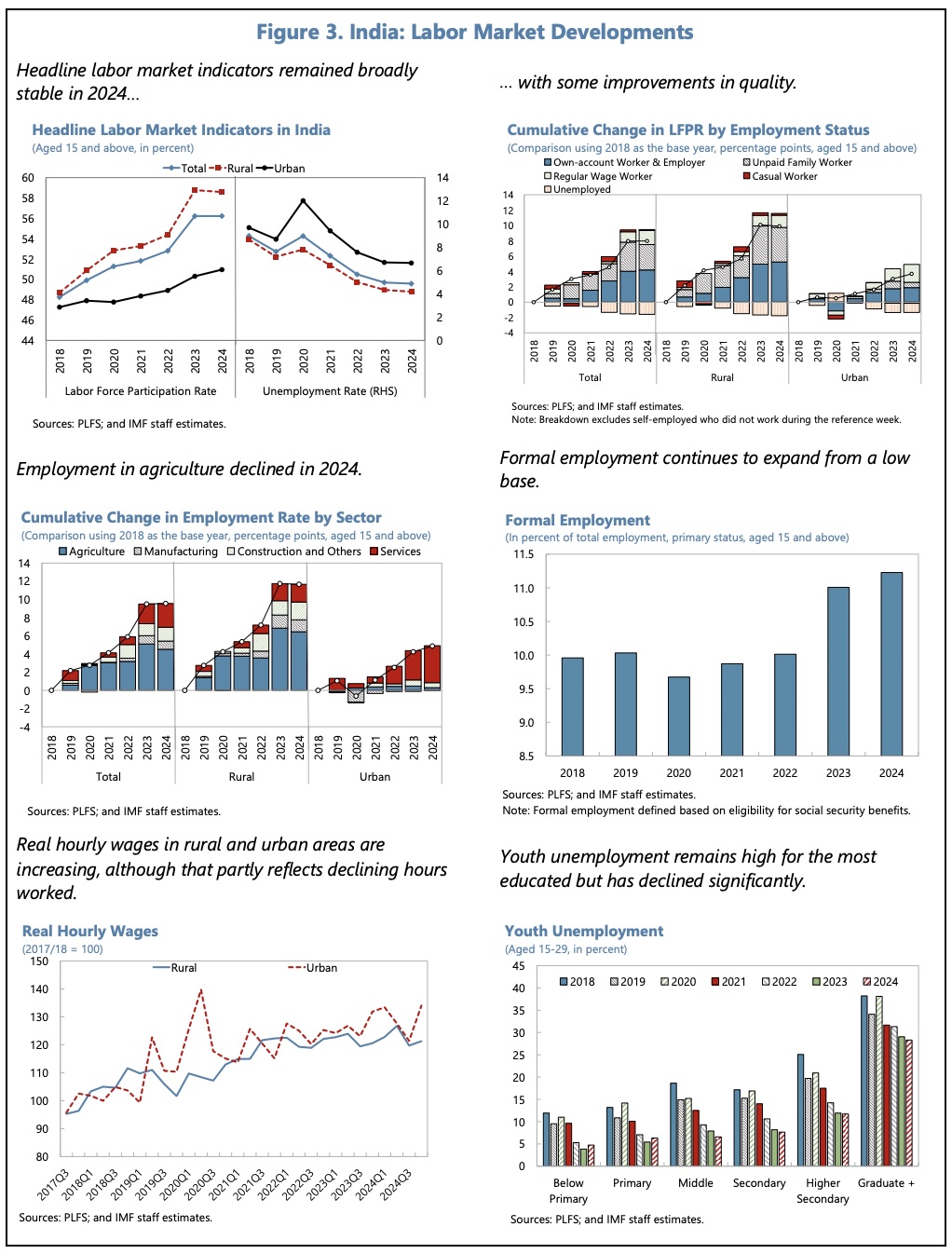

Labour market conditions have been broadly stable. Overall labour force participation is little changed (c.56%), but formal and regular employment have expanded to 11.2% and 12.7% respectively, indicating a mild improvement in employment quality. Real hourly wages have risen by 16% (rural areas) and by 26% (urban areas) since 2018. Unemployment in September 2025 was low, at 5.2%.

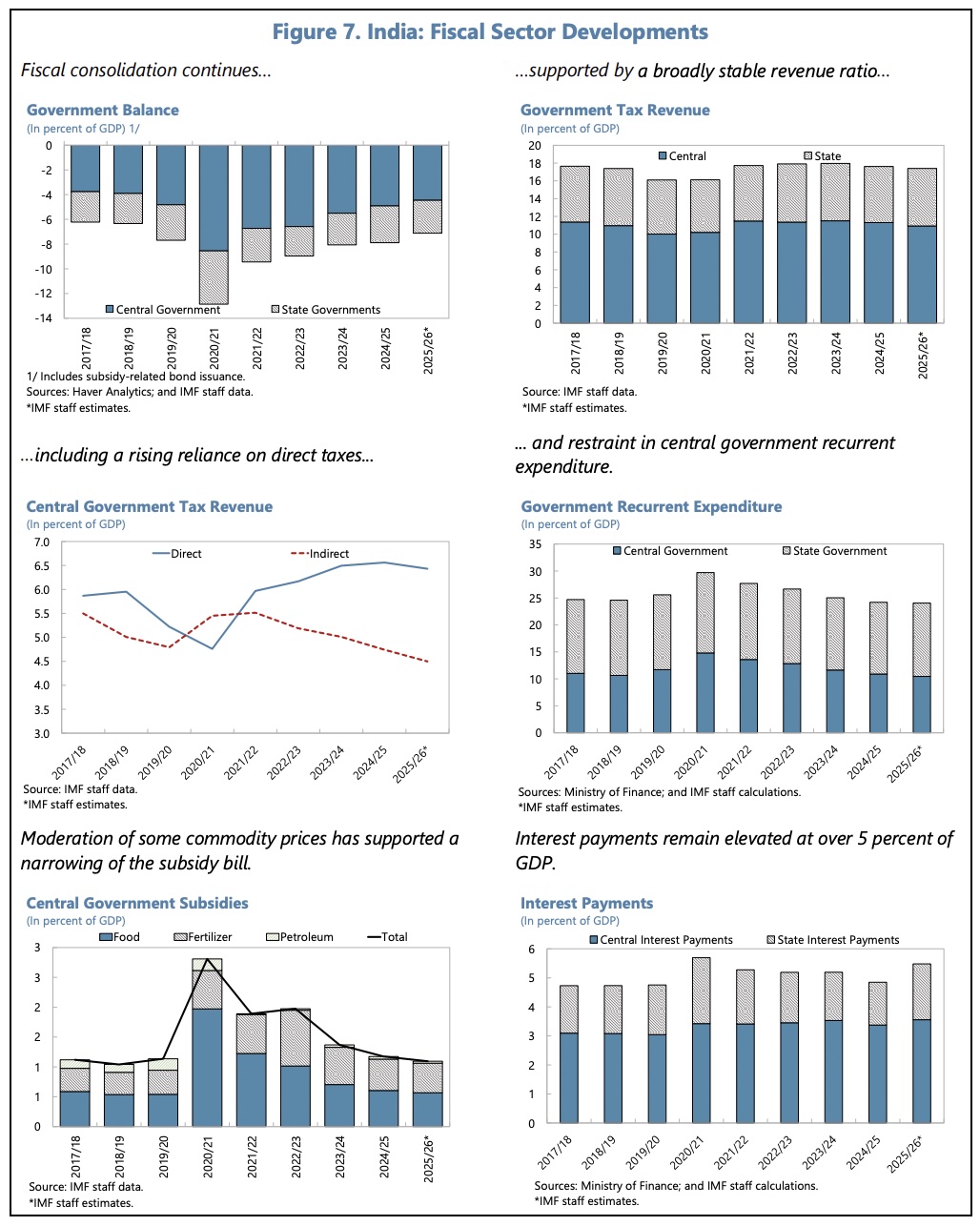

The general government deficit in 2024/25 is estimated at 7.9% GDP, down from 8.1% in the prior year. Within this, the central government deficit has declined to 4.9% GDP, whilst the states’ deficit has risen from 2.9% GDP to 3.3% GDP.

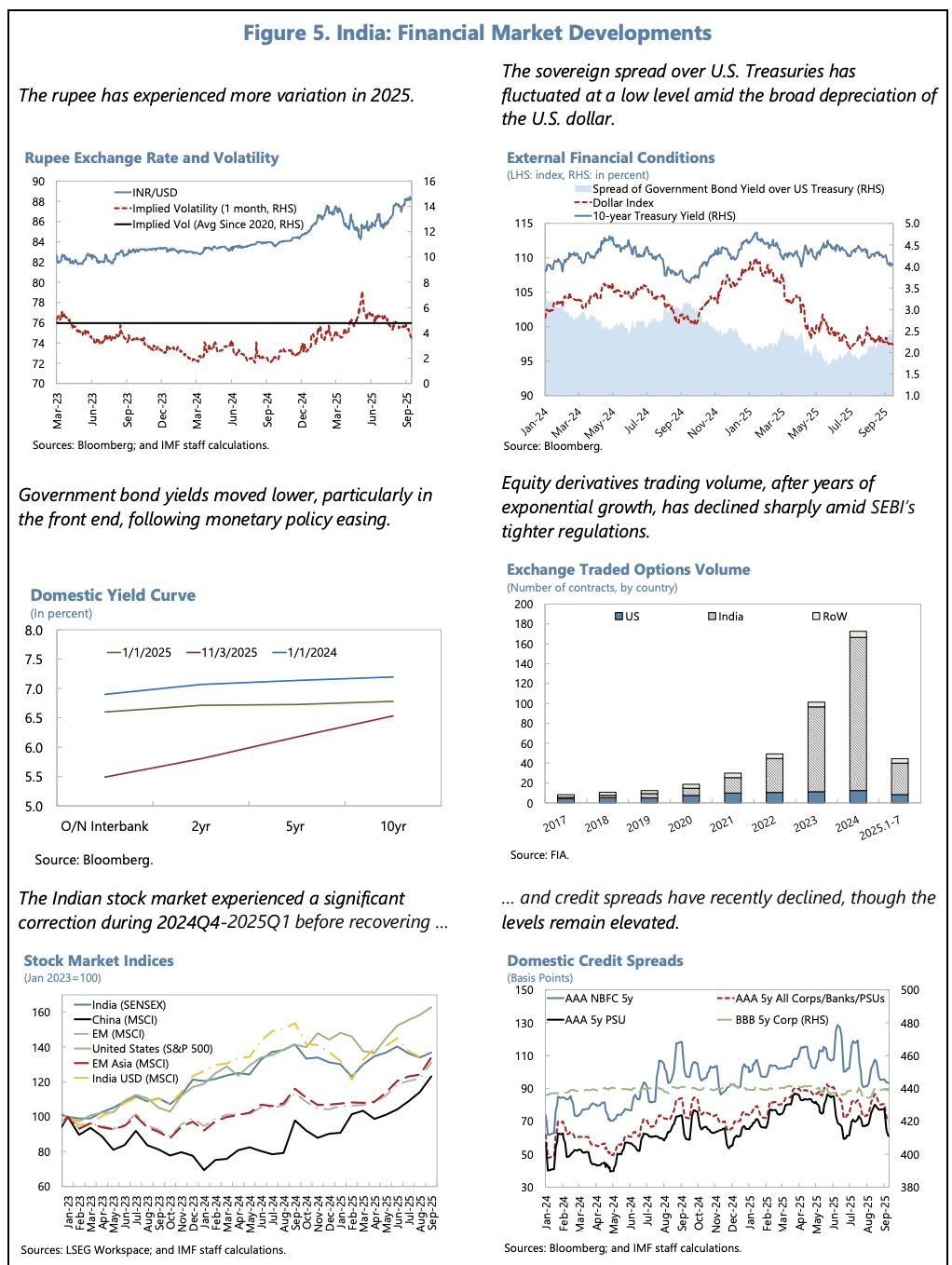

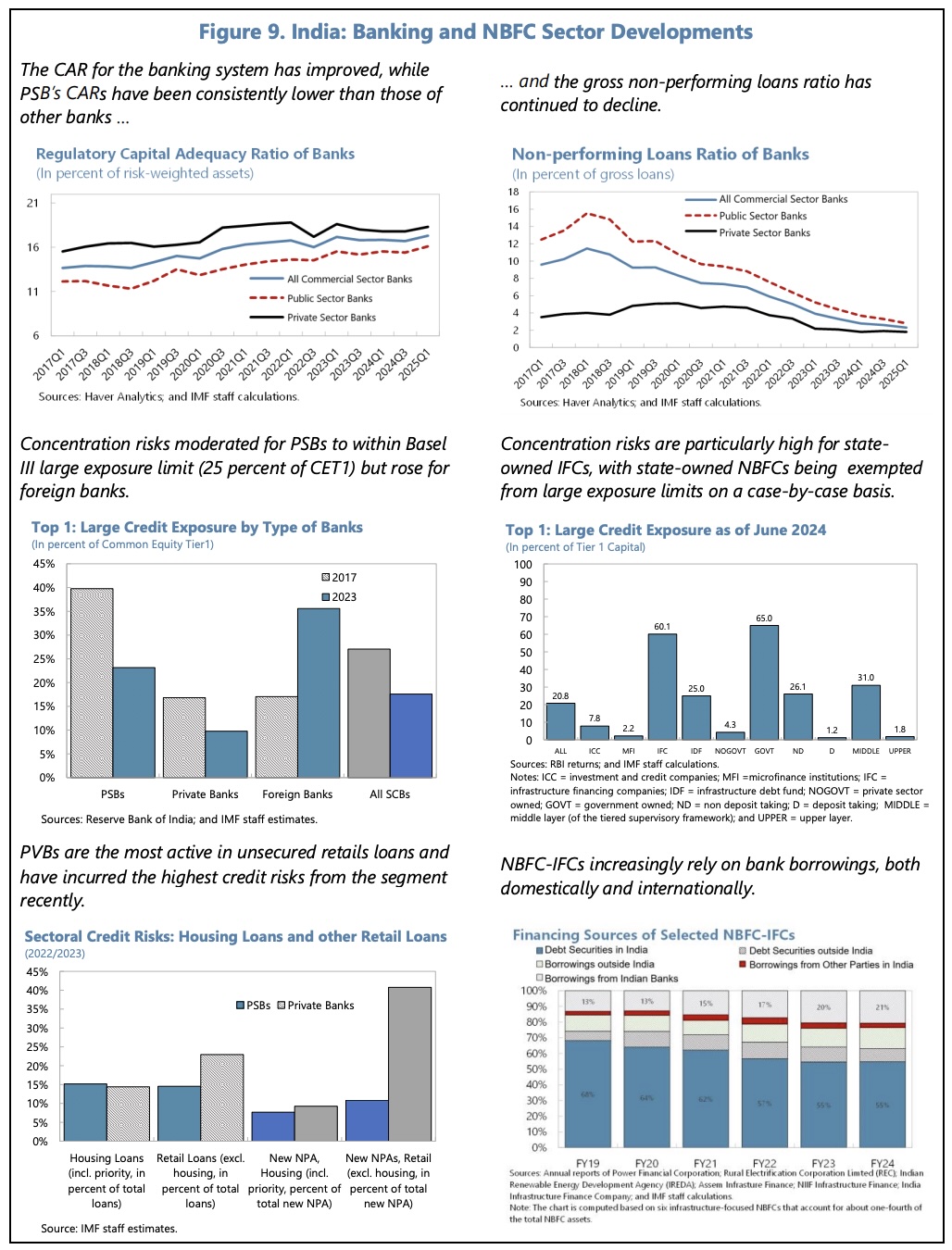

Financial conditions have eased in the past year, with government bond yields and policy rates declining. India’s S&P credit rating has risen to BBB. Credit spreads have eased, although they remain elevated. Reserve Bank policies have been supportive. Nonetheless, credit growth has moderated from 13% YoY, in September 2024, to 10.4% YoY, in September 2025. Growth overall has mirrored nominal GDP growth, and the credit gap is estimated to be broadly closed or slightly negative. Housing prices have risen modestly.

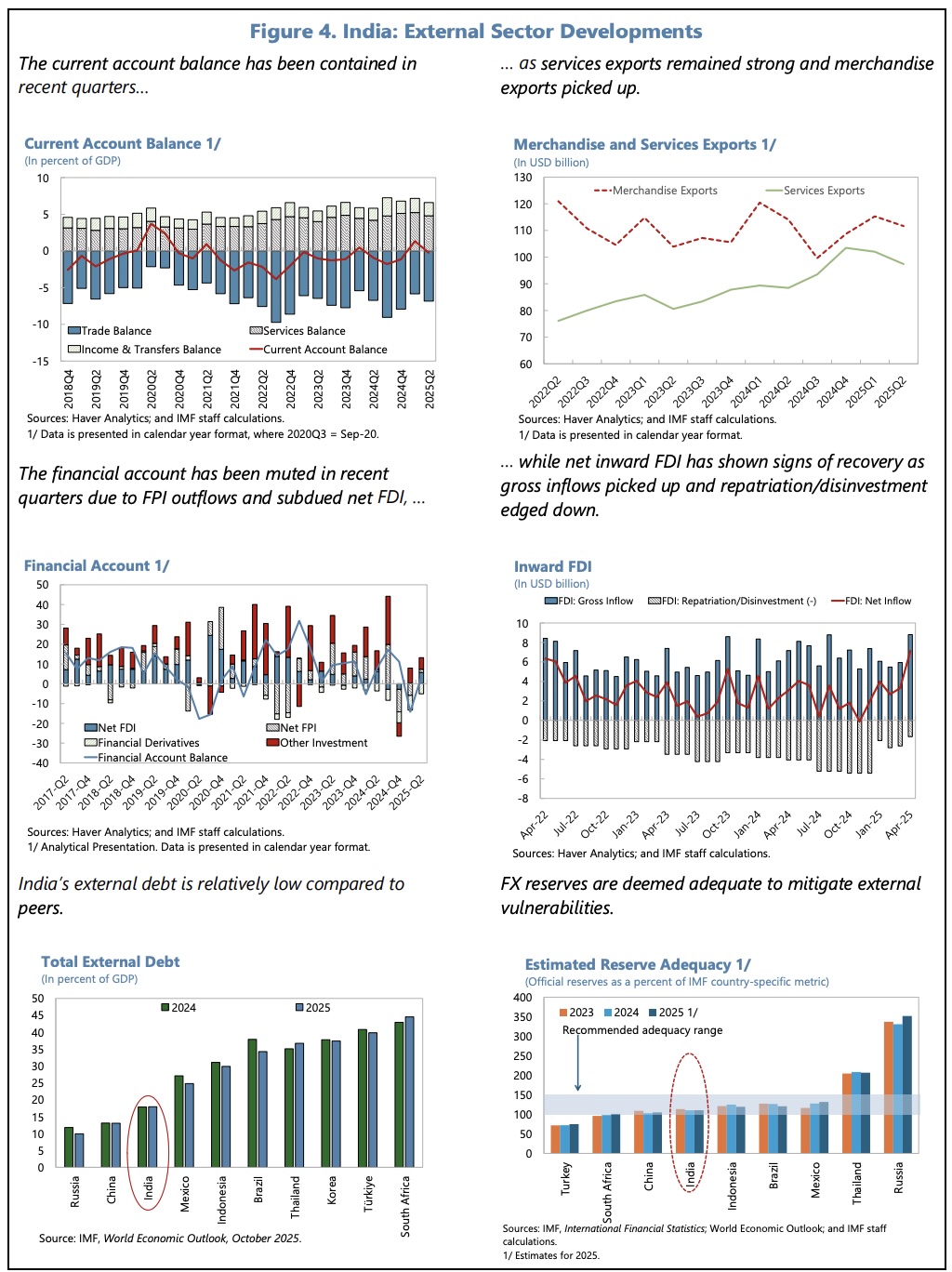

The current account deficit (0.6% GDP in 2024/25) has been slightly smaller than is warranted by India’s development fundamentals, as net FDI has fallen to about zero, reflecting trade tensions, weaker net portfolio flows and increased outward FDI. Services exports and inward remittances have remained robust. FX reserves stood at $695bn in October 2025, covering eight months of prospective imports (109% of the IMF’s adequacy metric).

Export restrictions have been reduced on some agricultural products, as domestic prices have eased. In addition, India has reduced the simple average tariff on industrial products from 13.5% in 2023 to 10.7%. A free trade agreement has been signed with the UK, according to which most bilateral tariffs will be eliminated over ten years. Free trade negotiations are underway with Australia, New Zealand, the EU and the USA.

Outlook and Risks

Growth in 2026/27 is forecast to decrease from 6.6% YoY to 6.2%, as US tariffs (assumed to decline to 19% on non-exempted goods from December 2025) feed into external demand and investment. The longer-term expectation for growth remains unchanged at c.6.5%.

Core inflation is forecast to rise to 3.5% YoY in 2026/27, as domestic food prices increase. Monetary and exchange rate policies are deemed to be ‘broadly adequate’. Given benign inflation dynamics and the baseline assumption of lower tariffs with time, the IMF advocate policies remaining ‘nimble, with an easing bias.’ They see scope to improve monetary policy effectiveness further, by enhancing pass-through mechanisms within the NBFC sector. As inflation expectations have become anchored, they see scope for greater exchange rate flexibility – with intervention only being used in the event of large shocks.

Despite reductions in personal income tax and GST effective rates/complexity, this year’s fiscal consolidation target is thought still to be achievable. If it proves necessary, the IMF advocate current spending should be the focus of rationalisation, not capital spending. Reforms in tax administration are expected to reduce the tax compliance burden and increase tax buoyancy in the medium term.

Longer term, the risk of sovereign debt stress is assessed as moderate. There is scope for the medium-term government debt target (c.50% GDP by 2030/31) to be made more ambitious, with the emphasis being put on increasing revenue mobilisation, which is slightly below the average of non-fuel exporting peers (c.18% GDP). Meantime, further reforms – spending efficiencies, better targeting of social spending, improved revenue mobilisation – are required to bring the states’ debts (28% of their GDP in 2022/23) to sustainable levels.

The current account deficit is forecast to increase towards its norm of 2% GDP, as exports weaken and international tariffs feed into the Real Effective Exchange Rate. The recent removal of caps on foreign portfolio investment in corporate debt, coupled with India’s long-term investment attractions, should help to ensure that a deficit of this scale may be financed.

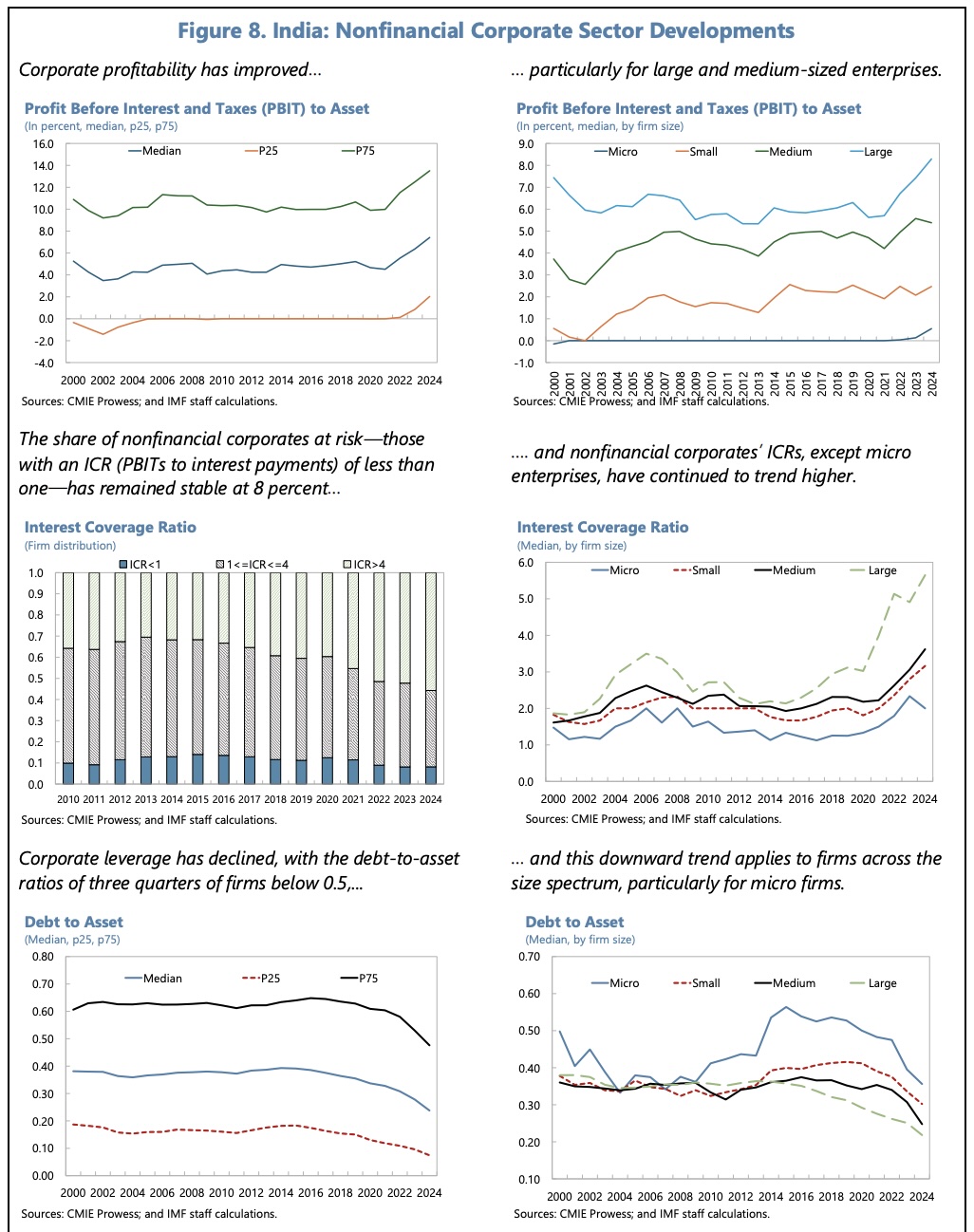

Systemic financial sector risks appear to be contained, with banks’ capital adequacy ‘well above required levels,’ and gross and net NPLs declining, except in the area of unsecured personal loans among private sector banks (which merits monitoring). Further strengthening of the risk management framework is in train and welcomed. However, there is scope for further strengthening of public sector banks’ capital adequacy, and the IMF have urged the authorities to be alert to vulnerabilities in the NBFC sector, which is playing an increasing role in the economy. Risks are particularly high for state-owned Infrastructure Lending Companies (IFCs), which are heavily exposed to the power sector, and enjoy certain exemptions from prudential standards. In addition to reducing these, the IMF have suggested the RBI should conduct detailed assessments of systemic risks in this area and possibly tighten limits on bank lending to these NBFCs, to reduce possible spillover effects.

Structural Reforms

Under the headline ‘Activating All Growth Engines’, the IMF continue to advocate reforms in the following areas:

- lifting trade restrictions & deepening trade integration with bilateral partners and trade blocs

- investments in physical public infrastructure

- reductions in red tape for firms and households

- increasing labour market flexibility

- a more targeted and resilient safety net

- enhancing education and skills development, and infant nutrition

- easing investment in agricultural land for more productive uses

- improving the insolvency resolution process

- raising university and private sector spending on R&D (below peer average)

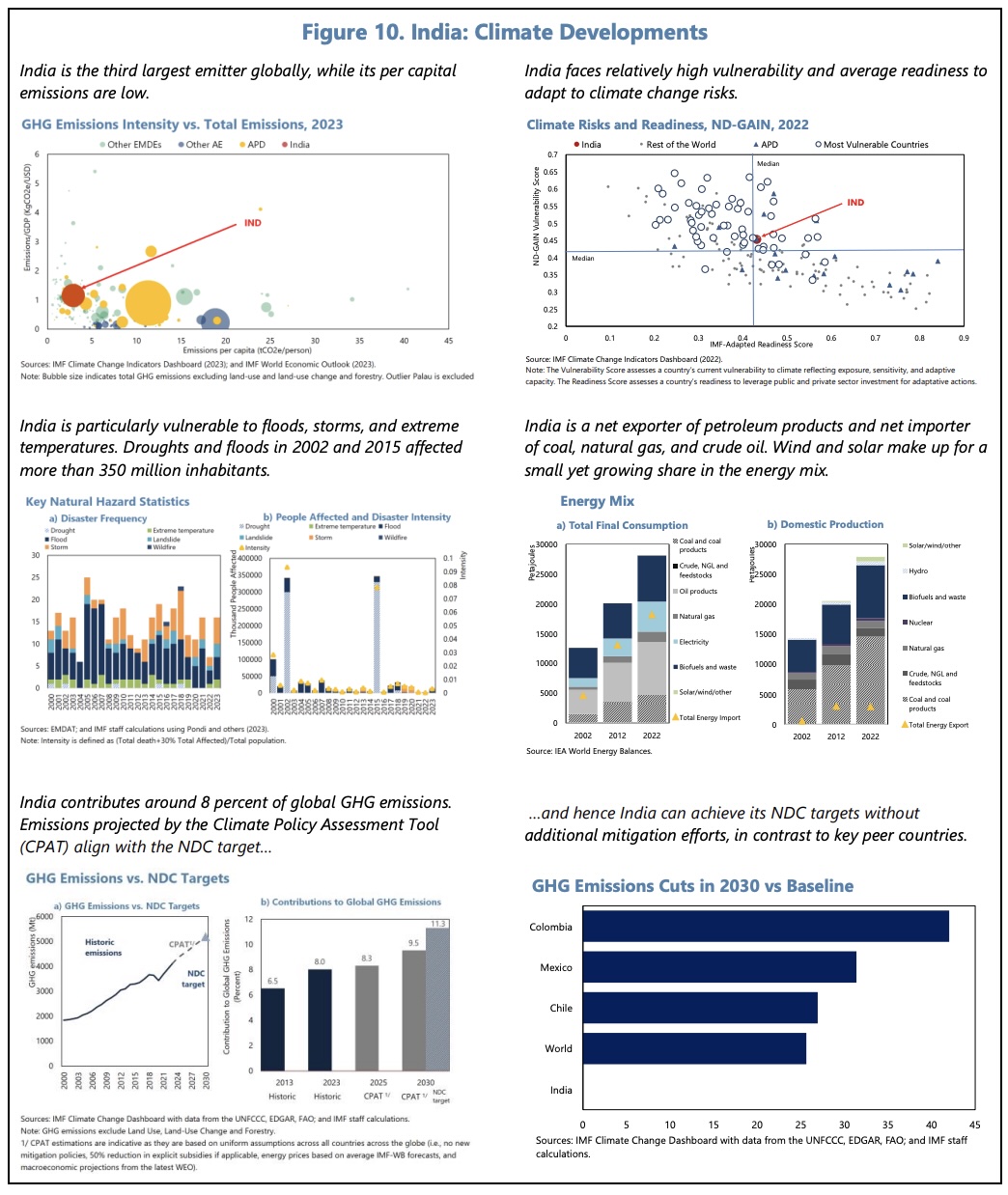

- reducing vulnerabilities to climate change. (Agriculture employs c.42% of workers.)

- improving the quality of macroeconomic and financial statistics.

The IMF’s full Article IV report may be read using this link to the IMF’s website: