In early October, the IMF posted their latest update on the Vietnamese economy, under the Article IV process.

Recent Developments

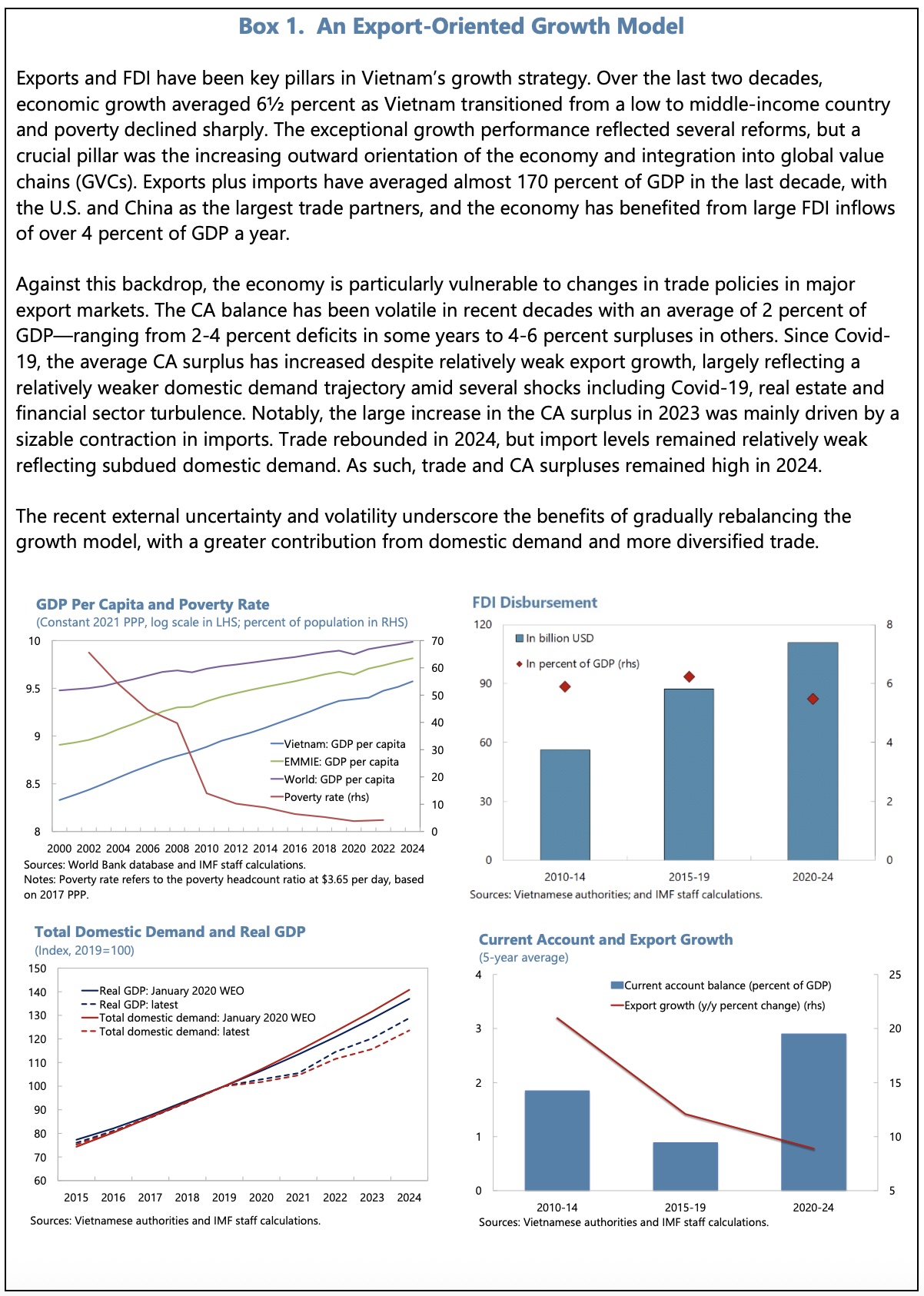

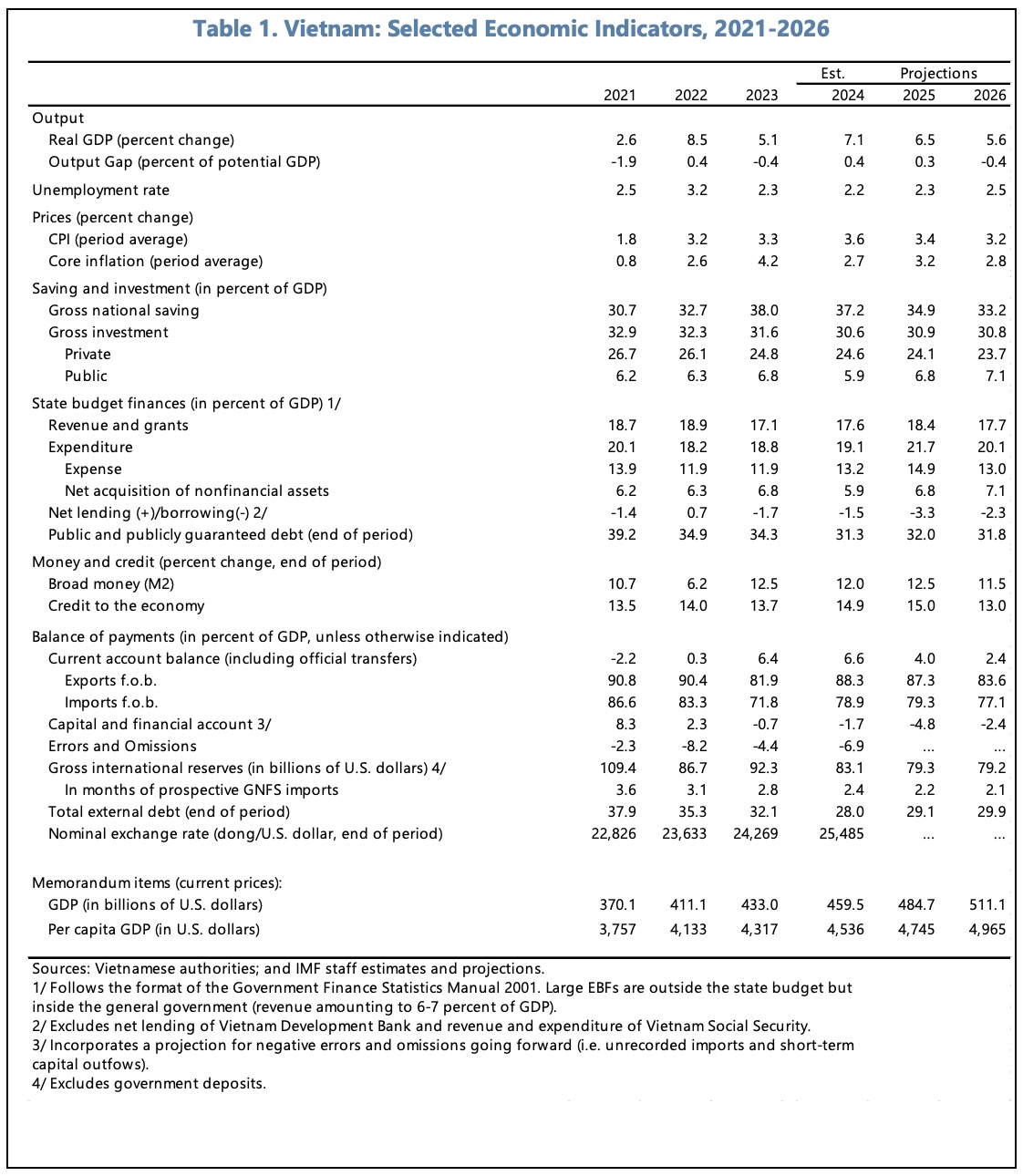

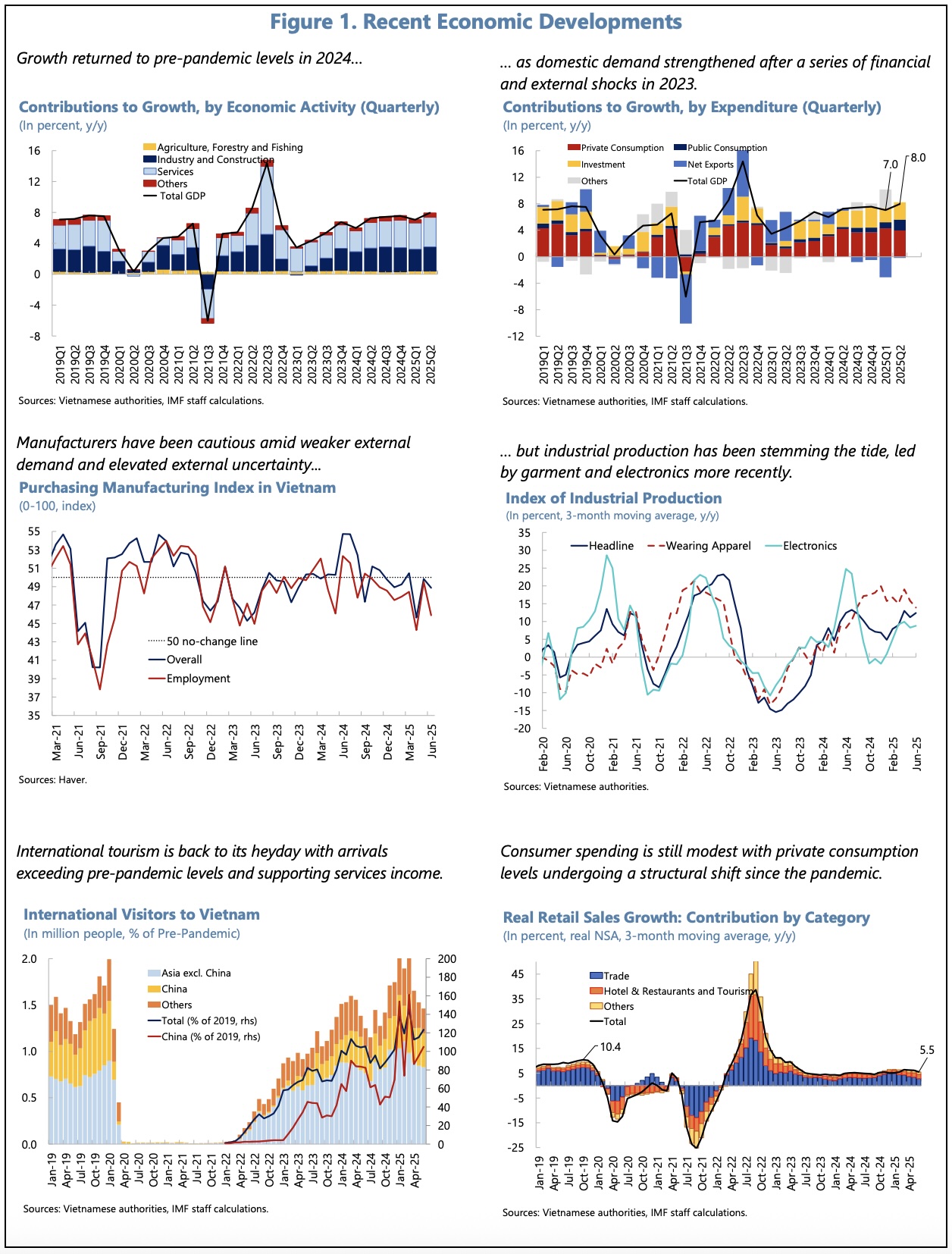

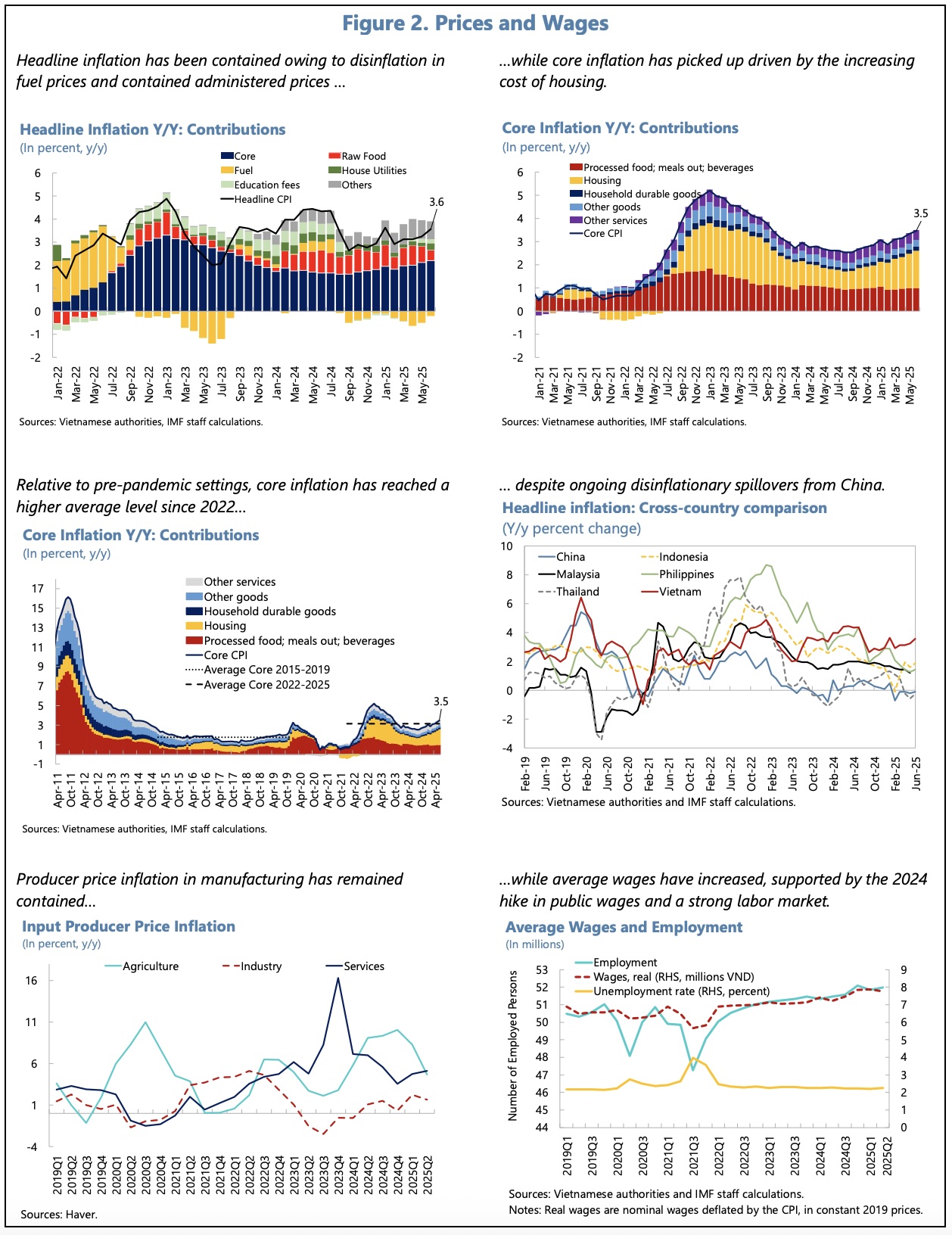

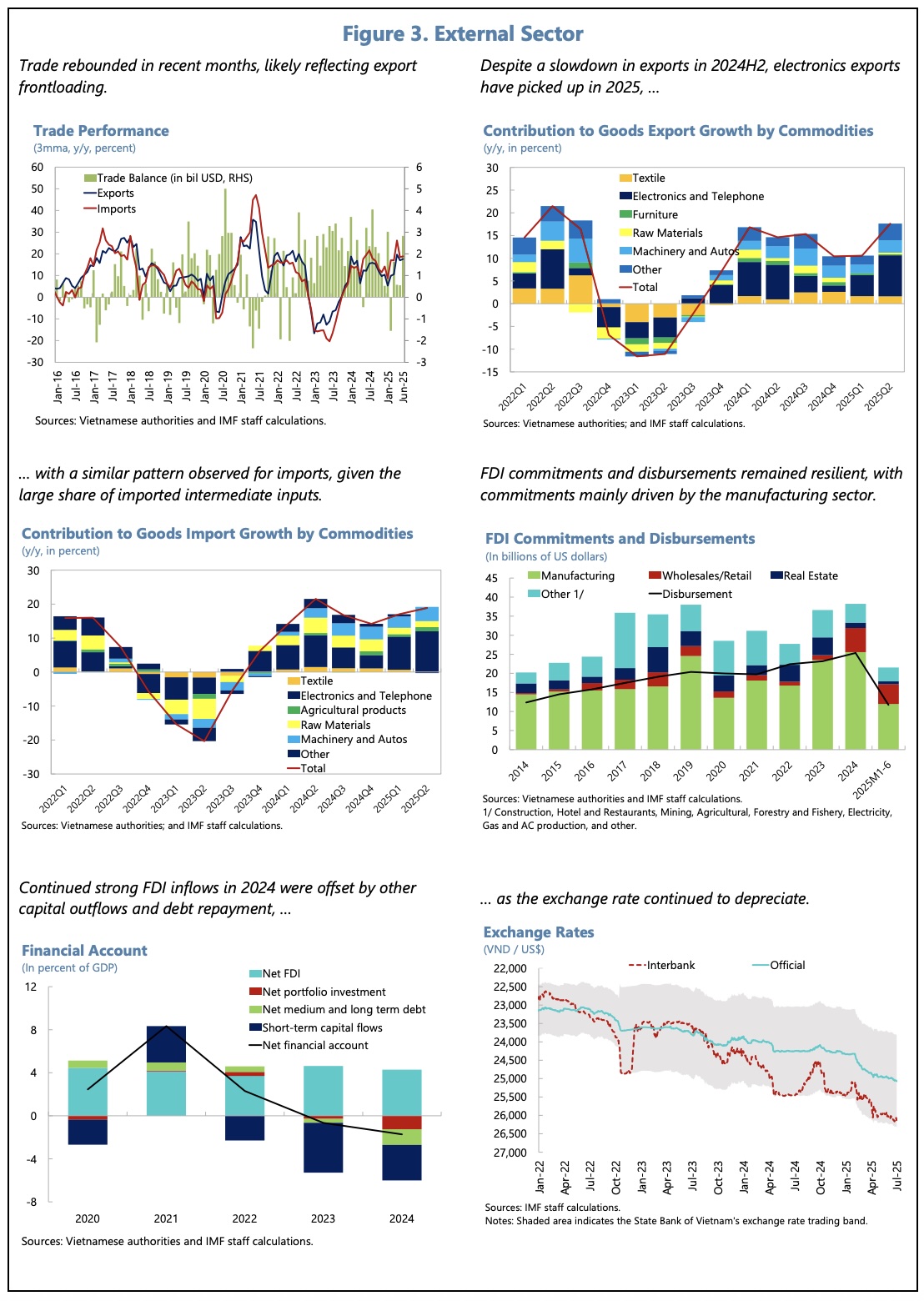

The momentum of growth in 2024 (real GDP +7.1% YoY) has continued into H1 2025 (+7.5% YoY). Inflation has been on an upward trend (+3.6% YoY in June), although it remains below the 4.5%-5% target. The current account surplus reached an historical high of 6.6% GDP, in 2024.

Outlook / Risks

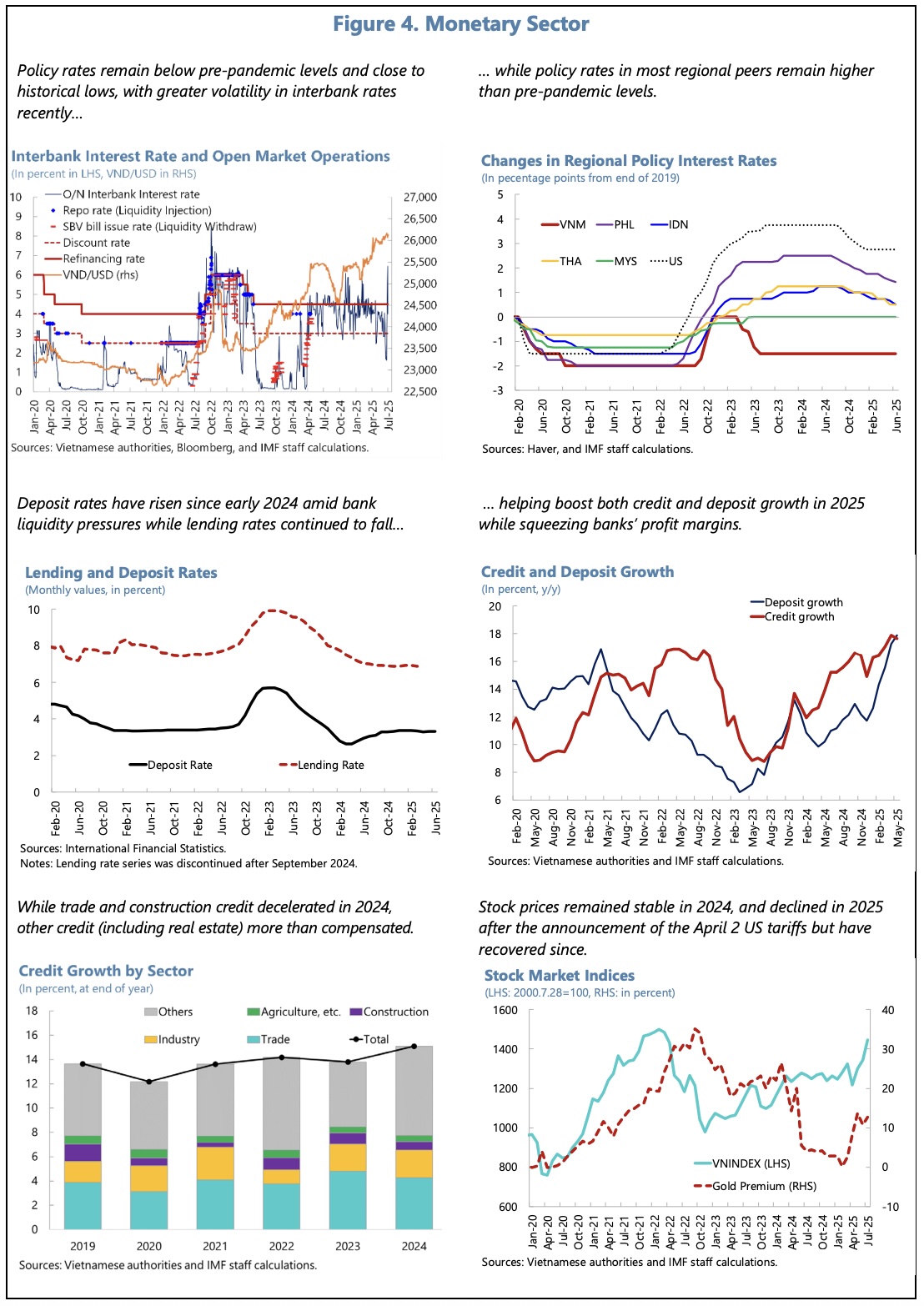

The IMF have indicated that growth has been supported by ‘export front-loading, faster credit growth and large one-off government spending.’ They have cautioned that the outlook is heavily dependent on ongoing trade negotiations and, more generally, on developments in the global trade environment and global financial conditions. They have warned that there is a risk of increased financial stress emerging, given Vietnam’s high indebtedness (credit at 136% GDP) and the possibility of tighter financial conditions.

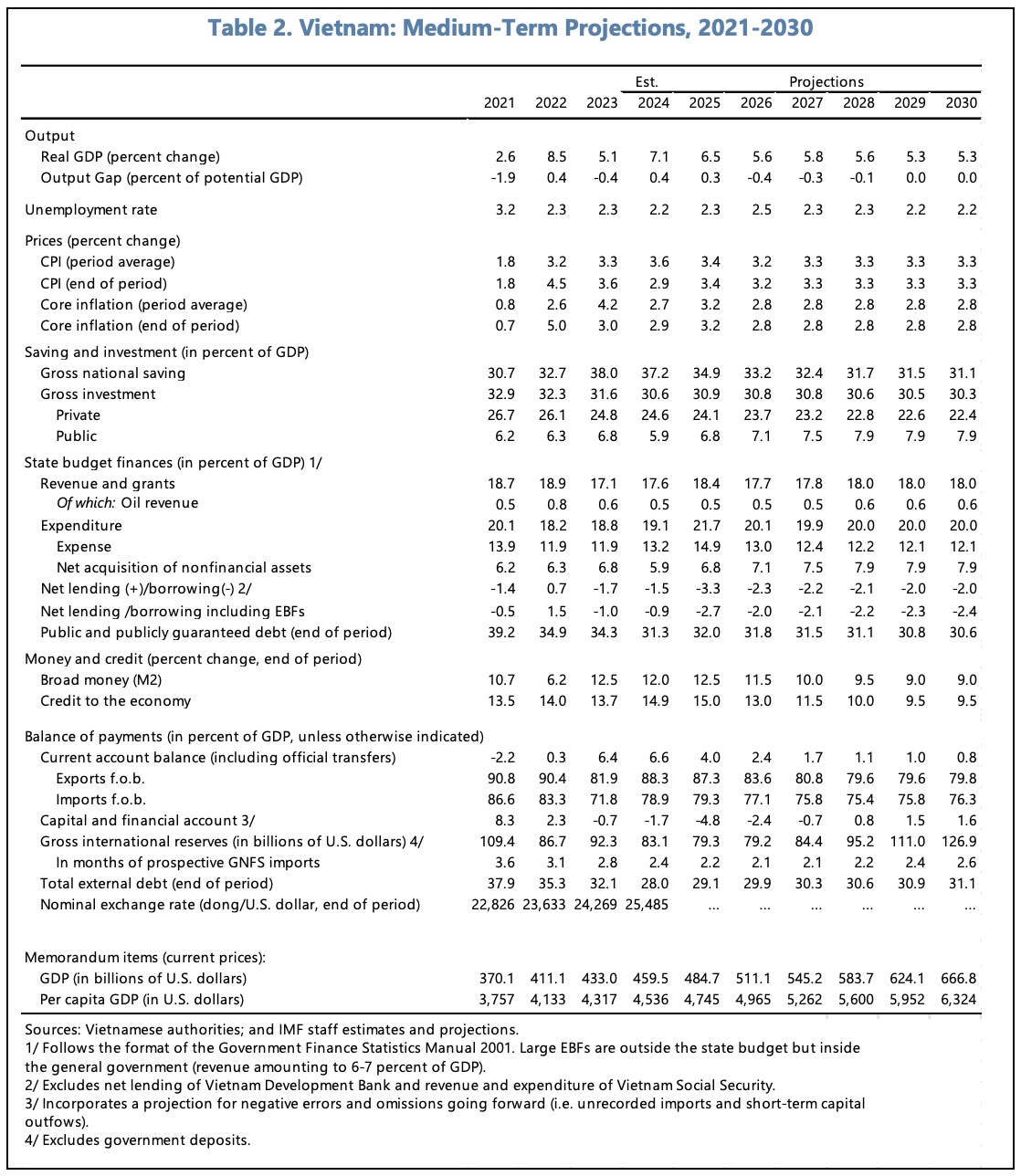

Looking forward, the IMF expect real GDP growth to slow to 6.5% YoY, in the full year 2025, and 5.6%, in 2026, as the effect of higher US tariffs bites and the government’s one-off stimulus unwinds. Inflation is projected to remain broadly stable, as a result of an opening of the negative output gap (as higher export tariffs take effect) and low inflation in China. Nonetheless, the IMF consider that the downside risks to their forecast are ‘high’.

Reform Priorities

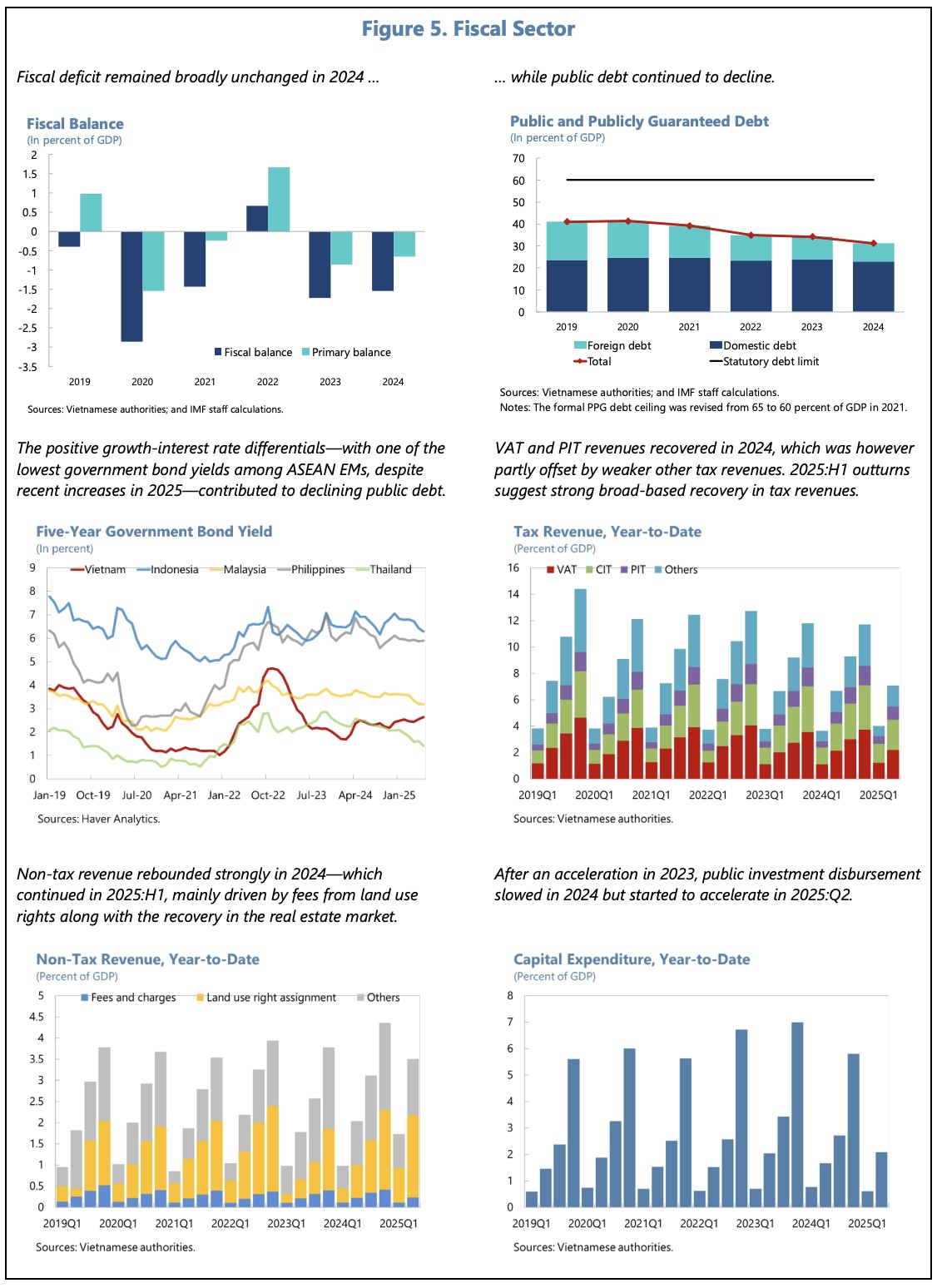

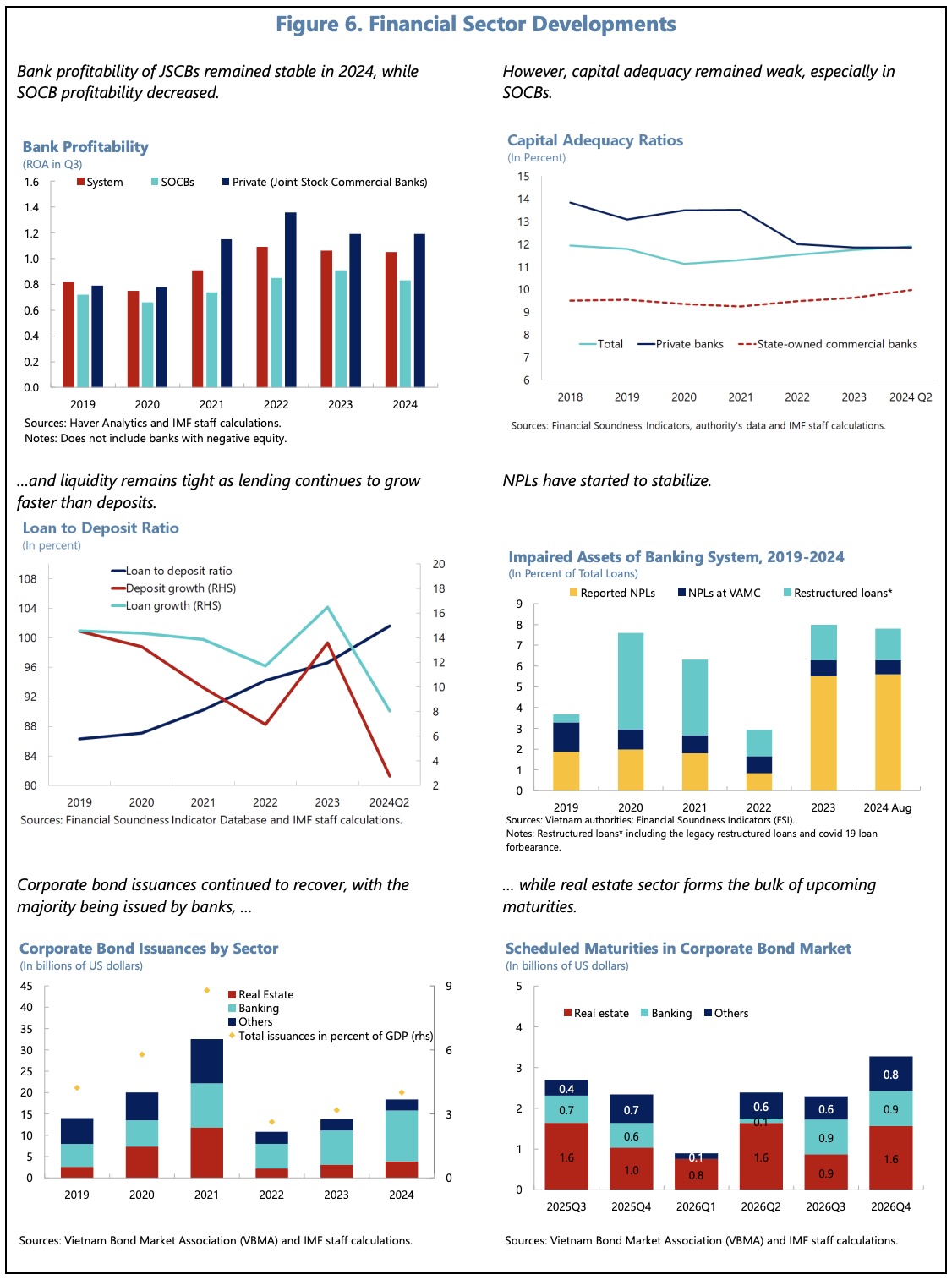

Naturally, an easing of global trade tensions would improve the outlook (the forecast assumes additional US tariffs average 20% from August 2025). Meantime, the IMF continue to advocate reforms in areas such as the development of a medium-term fiscal framework and the strengthening of financial sector resilience.

In terms of structural reform, the IMF consider it is important to prioritize actions to improve skills and productivity (which has been on a declining trend and lags regional peers, especially for non-FDI firms), to upgrade key infrastructure (transport, energy, digital), and to boost domestic demand (inter alia through higher public investment, an improved business environment, and enhanced social safety nets). Credit and resource misallocations (for instance, in favour of real estate and construction) are seen as sizeable, and economic statistics need improvement, to make policymaking more effective.

Population ageing and climate change have been identified as long-term challenges.

Shorter-Term Policies

In the shorter term, the IMF believe the policy mix should remain flexible, but with the onus of measures taken to support the economy, if needed, being borne on the fiscal side (through public investment implementation and strengthened social safety nets). They consider that, with policy rates near record lows, the scope to ease monetary policies is ‘very limited’ and that, already, inflation and FX risks need to be carefully monitored. Further lowering domestic rates could exacerbate capital outflows and pressure the exchange rate.

Instead, the current environment underscores the importance of modernizing the monetary policy framework, by accelerating the transition to an inflation targeting regime, and strengthening the state bank’s operational independence, in order to anchor inflation expectations, &c.

For full details of the Article IV report, including appendices, please use the following link to the IMF’s website.